Staying Calm Amid Economic Uncertainty

Key Points – Staying Calm Amid Economic Uncertainty

- Keeping Your Emotions Separate from Your Investments

- Taking Risk Off the Table

- Don’t Completely Count Out Bonds from the Equations

- How Will the Markets React to the Fed’s Upcoming Decisions and the Russia and Ukraine Conflict?

- 7 minutes to read | 10 minutes to listen

Everyone has their opinions about the Federal Reserve’s plan of action with interest rates and the developing situation between Russia and Ukraine. Regardless of your opinions, Dean Barber and Logan DeGraeve explain why it’s critical to keep your emotions in check and make sound financial decisions during these times of economic uncertainty.

Get a Complimentary Consultation Subscribe on YouTube

Staying Calm Amid Economic Uncertainty

Dean Barber: Hello, everybody! I’m Dean Barber, founder and CEO of Modern Wealth Management. Welcome to the Monthly Economic Update. Today, Logan DeGraeve joins me to discuss what is happening in the market and all the economic uncertainty.

We’ll break down how many of the S&P 500 stocks are in bearish, bullish, and neutral territory. We’ll also explore that for the Dow Jones Industrial Average and the NASDAQ. And, of course, there’s a lot happening with Russia and Ukraine and inflation and interest rates that’s causing economic uncertainty.

Diving into Recent Market Data

Dean Barber: Before we get to the discussion with Logan and I about how to deal with this in your plan, let’s go over some of the most recent data. The date that we’re producing this is February 23, so who knows what is going to happen over the next several days. There is a lot of economic uncertainty going on.

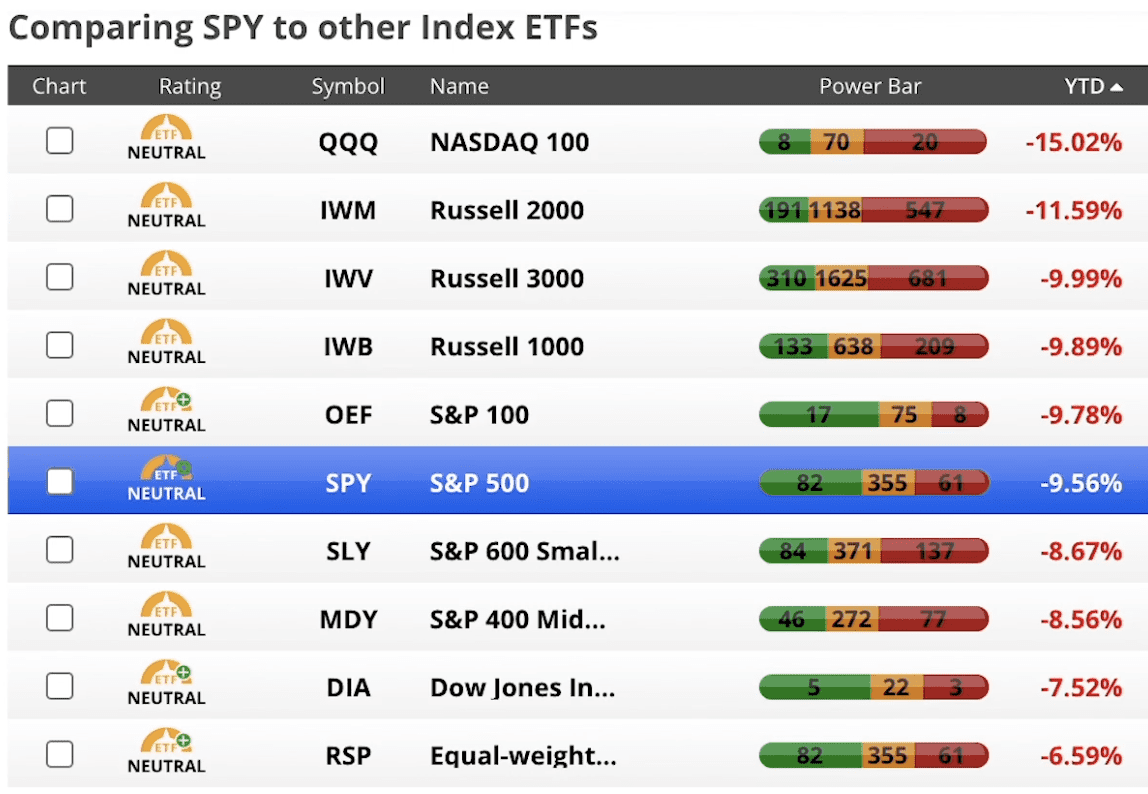

Let’s go over some statistics of the major indexes year-to-date. As you know, we use a platform that shows us whether stocks are at a bearish, bullish, or neutral mode. We won’t get too deep into the weeds, but here are a few statistics below in FIGURE 1. Connect with your advisor to review these in more detail.

FIGURE 1 | Comparing SPY to Other Index ETFs | Chaikin Analytics

What you’re seeing above is that virtually every major index is either neutral or neutral plus. We don’t have anything in bearish territory yet. Let’s look at the NASDAQ 100 composite. It’s the worst performing composite year to date at -15.02%. Out of the 100 stocks in the NASDAQ, 20 of those are bearish, 70 are neutral, and eight are positive. That gives us a neutral rating for the NASDAQ.

Now, compare that to the Dow Jones Industrial Average. Of the 30 stocks, three are bearish, 22 are neutral, and five are positive. That gives the Dow Jones Industrial Average a neutral plus rating.

The S&P 500 Equal Weight has 61 negative stocks, 35 that are neutral, and 82 that are bullish.

We don’t need to go into a lot of detail but suffice it to say that we are watching this very closely. If more and more stocks turn bearish and the indices turn bearish, that’s going to be our catalyst to take some risk off the table.

Trials and Tribulations of Economic Uncertainty So Far in 2022

Logan, we finished 2021 with a bang. It was an amazing year. That was coming off an amazing bull run following the onset of COVID-19. People were euphoric and felt great. Suddenly, we’ve had nothing but huge swings in the market and a lot of economic uncertainty. Emotions are running high.

Logan DeGraeve: Absolutely. I think that people forgot that the market can go down, too. We had a lot of conversations with clients in the fourth quarter of last year about taking some gain off the table. But they say that they don’t want to be in bonds and that bonds aren’t any good. Well, that’s not true.

Reviewing Your Portfolio Allocation

No one should be surprised by this. The Fed is going to raise rates and inflation is up. Those are not the surprising things. The Russia and Ukraine thing is a wrinkle in all this. At the end of the day, the most important thing you can do is talk with your advisor and look at your portfolio allocation. How does it complement your overall financial plan? How much risk should you be taking on your money?

It may have changed over the last couple of years we had good returns. Maybe you don’t need to be in that 60/40 portfolio. Maybe you could be in a 40/60 portfolio now.

Dean Barber: One of the things that tends to happen is that when you get into a period when everything is great, the story is that the rising tide lifts all boats. It does feel good and it’s hard to step back from that. Let’s use that example of having a 60/40 portfolio. When we examine a financial plan, we may see that their probability of success is just as strong if we reserve it and have 40% in equities and 60% in fixed income. Or maybe it’s even 30/70?

That’s the beautiful thing about having that financial plan done. In a period like this with economic uncertainty and volatility, what is the least amount of risk you can take on your portfolio and still accomplish your objectives?

A Financial Plan Can Help Remove Emotions from Decisions

Logan DeGraeve: Absolutely. I had a discussion with a client the other day about this. They called and were nervous about everything going on. I pulled up their plan and told them to just take the emotion out of it. Let the plan do the talking. Also, the money in your portfolio shouldn’t be behaving the same way. The money you’re spending today, tomorrow, and next year should be a lot different than the money you’re going to spend 15 to 20 years from now.

With that longer-term money, we know that the market will be back and things will be OK. But with the money you’re spending today and tomorrow and the economic uncertainty we’re seeing right now, you don’t want that risk.

Not All Bonds Are Created Equal

Dean Barber: It’s interesting because I also had a conversation with someone who was asking why they would want to be in bonds. They’re thinking that a rising interest rate environment is not going to be positive for bonds. Well, first, not all bonds are created equal. There are some bonds and types of investments in fixed income that are doing well this year compared to the bond aggregate.

The bottom line is that you have that fixed income or safe position within your portfolio for times like this. If the equity piece is down a little bit, you don’t want to sell out on it when it’s down. What you’d rather do is take some of the fixed income and spend it if you needed an extra lump sum or something like that. Make sure that you have enough money in that position that’s not going to be tied to the economic uncertainty of the stock market so that you can continue doing the things that you want to do and spend the money the way you want to spend it.

Logan DeGraeve: I don’t think I can emphasize it enough to make sure that all the money in your portfolio is not behaving the same way.

Cost of Oil’s Impact on the Markets

Dean Barber: Let’s discuss what is going on in the market and why it’s behaving the way that it is. Logan mentioned Russia and Ukraine. I think the Russia and Ukraine thing is an additional catalyst that is scaring the market because we could see oil costs around $130, $140, $150 a barrel. We’ve seen that before. But what does that do automatically? It creates more inflation on top of an already high inflationary environment. That, in turn, could cause Federal Reserve Chairman Jerome Powell to act even faster. He could raise rates even faster than what he’s been planning on.

Then, the Russia/Ukraine thing dissipates, inflation starts to fall, and the Fed overdid it. And he sends us into a recession. In my mind, that’s where the fear in the markets is coming from. It’s all that economic uncertainty that’s out there. But, otherwise, from an earnings standpoint, things look great.

This is one of those things where if we were just going to look at fundamentals, we could say things are looking positive. But there are all these things are out of the market’s control that could have a big-time impact in the short-term.

What Is Jerome Powell Going to Do?

Logan DeGraeve: Absolutely. Bud Kasper and I talked last week on America’s Wealth Management Show about the Fed, raising interest rates, and inflation. None of this should be a surprise to anyone with what we’re seeing. But to Dean’s great point, the Russia and Ukraine thing does put a wrench in it. I wouldn’t want to be Jerome Powell right now, would you?

Dean Barber: No. A few weeks ago, Bud and I were talking about interest rates that Jerome Powell is walking a tightrope. One little mistake could be all it takes to send the markets into a tailspin. I think the big takeaway during the economic uncertainty is to go back to the asset allocation in your plan and asking, what’s the least amount of risk I could be taking right now and still accomplish my objectives? Because the sun is going to come out again. We’re going to have another bull market and it’s going to feel good. That’s when we can ratchet back the equity exposure.

Don’t Make Knee-Jerk Reactions During Times of Economic Uncertainty

Logan DeGraeve: The way I think about this and what I’ve been talking to clients about is there is always going to be something going on. Think about the last two to three years with COVID and everything else. There is always something going on. I think the bigger takeaway is to not make knee-jerk reactions when there is economic uncertainty. Make sure you have a conversation with your advisor and complementing the financial plan. Make sure that everything is in sync.

What you don’t want to do is watch the news. You can watch the news on any given day and think, ‘Oh my goodness. I have to get out of the market.’ Have some discipline around the decisions being made.

Helping People Live Their One Best Financial Lives

Dean Barber: As a CFP® professional, that’s exactly what Logan brings to the table. Let’s look at this from a logical standpoint and remove the emotion. The idea is for people to live their one best financial life and do the things that they want to do.

Logan DeGraeve: I say all the time that I don’t know what the market is going to do. But I do know that Mr. and Mrs. Smith are going to need X-dollars per month in retirement. How do we make sure that happens?

Dean Barber: That’s the key. Logan, thanks for taking the time to join me for the Monthly Economic Update. Ladies and gentlemen, thanks for joining us. If you have any questions, reach out to schedule a 20-minute ask anything session or a complimentary consultation with one of our financial advisors. We can do a quick phone conversation, virtual meeting, or meet with you in our office. We wish you the best and come on spring! Let’s get here quick.

Schedule a Conversation

Click below to select the office you would like to meet with and check the calendar. We can meet in person, by virtual meeting, or by phone. Then it’s just two simple steps to schedule a time for your conversation.

Get a Complimentary Consultation

Investment advisory services offered through Modern Wealth Management, Inc., an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Advisor. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.