Is the Stock Market Overvalued?

Key Points – Is the Stock Market Overvalued?

- Is the Stock Market Overvalued Is a Question That’s Been Asked A Lot in Recent Years

- Understanding Types of P/E Ratios

- Looking at Long-Term Data to Determine If the Stock Market Is Overvalued

- Assessing Research from Robert Shiller, Ed Easterling, and James Tobin

- 14 Minutes to Read

Do You Remember the Market Madness of 2020?

Four years ago, we witnessed some historic swings in the stock market that led me to do some extensive research on stock valuations. My goal was to provide a thorough (and hopefully informative) answer to whether the stock market was overvalued while we were experiencing some wild market volatility.

Fast forward four years, and the question of whether the stock market is overvalued is one that we still field on an almost daily basis. The problem is, there are no easy answers. That’s because there are so many methods used to measure valuations. Unless you understand them all, it’s hard to form an opinion on which one is correct at any given point in time. Add in a personal bias toward a particular method and you’ve really complicated the discussion.

The goal of this article will be to help you understand all the different methods—at least in a cursory fashion—and the pros and cons of each. That way you can begin to form your own opinion on if the stock market is overvalued. Some of you will change your minds. Some of you will have your opinions validated. And hopefully, all of you can take away some knowledge that you didn’t have before.

Before we really dive into whether the stock market might be overvalued, I want to start with some basics about valuations. The stock market can remain overvalued or undervalued for FAR longer than anyone can anticipate. Therefore, valuations are not good short-term indicators. They’re just not. And anyone that tells you they are is probably selling something you don’t want to buy. With that out of the way, let’s get to it.

Valuation Methods

Most valuation methods for calculating the relative value of the stock market as a whole use some form of price-to-earnings ratio (P/E ratio) in their determination. So, let’s first understand what that means. We’ll discuss it in terms of an individual company to simplify the concept.

Price-to-Earnings Ratio

The P/E of a company is the ratio of a company’s current share price to its earnings per share (EPS). This is also known as the price multiple or the earnings multiple. Investors use that ratio to determine the relative value of a company’s stock and compare it to other similar companies or to the overall market.

In practice, the P/E tells us what dollar amount investors are willing to pay per share to receive $1 of the company’s earnings. Thus, the term price multiple. So, for example, a company that has a P/E of 20. You will pay $20 for every $1 in earnings you expect to receive from that company because that’s what the market is currently willing to pay.

A high P/E might mean that the stock price is high relative to the company’s earnings and is therefore overvalued. On the other hand, a low P/E may mean that the stock price is low relative to the company’s earnings and is possibly undervalued. We can apply the same principles to the overall market. It’s just a more complicated exercise.

The calculation is the same: Current Share Price divided by Earnings Per Share. It’s just that you need to figure that for all 500 companies in the index if you’re looking to find the P/E for the S&P 500.

Types of P/E Ratios

Now that you understand the basics of the P/E ratio, you need to understand the different types that are out there. Here’s a brief list of the ones I can think of off the top of my head:

Forward P/E

Each of these use the same basic calculations, but they use different timeframes. For example, forward P/E measures the current price versus the expected earnings over the next 12 months. Obviously, if you project the earnings to be higher over the next 12 months and use that as the divisor for the stock price, your P/E is going to be lower. This is the method that most in the financial media use when they talk about whether the market is overvalued or undervalued.

Trailing P/E

Trailing P/E simply uses the last 12-month average of share price and earnings which, doesn’t really skew your numbers like forward P/E does, it just smooths out quarterly and annual fluctuations that may affect certain companies in certain industries.

CAPE

Cyclically Adjusted P/E (CAPE) does the same thing as trailing P/E, but over a longer historical timeframe of the trailing 10 years. It does a great job of smoothing out peaks and valleys in the data and gives what some believe is a more realistic look at overall market valuation. This is the method developed by Dr. Robert Shiller, and one we’ll be discussing later in the article in more detail. There are also some contemporaries of his we’ll talk about as well. One is Nobel laureate James Tobin, who developed the Q ratio. The other is Crestmont Research Founder Ed Easterling, who developed the Crestmont P/E.

Absolute P/E

Absolute P/E is simply the P/E for the current timeframe being measured, whether using trailing or forward EPS as the denominator or a combination of both.

Relative P/E

Relative P/E is the current P/E versus the historical P/Es from a select timeframe, say five or 10 years, to understand where today’s P/E is relative to past P/Es highs and lows. This can help determine whether the P/E currently is near the high or low end of the historical spectrum and therefore whether a stock is relatively expensive, or a relative bargain.

Are you thoroughly confused yet? If not, hang in there. There’s more.

Looking at Long-Term Data to Determine If the Stock Market Is Overvalued

When determining whether the stock market is overvalued, I prefer to have more data than less. It just makes sense to me because you can’t know with any certainty if what’s happening today is unprecedented if you’re only looking back 10, 20, even 50 years. The timeline isn’t long enough to gain a proper historical perspective. Unfortunately, that’s what far too many people do. They make decisions based on too short of a time horizon and don’t understand where the market, or even an individual stock is, from a longer-term perspective.

Advisor Perspectives (formerly dshort) has been a resource that I frequently use to gain historical perspective. They produce very informative charts and graphs each month. Take for instance Figure 1, below, which is a multi-decade regression to trend of the S&P Composite.

FIGURE 1 – S&P Composite Index: Regression to Trend – Advisor Perspectives1

Figure 1 goes all the way back to the late 1800s and comes forward through today. It shows the value of the market versus the trend line over that timeframe and gives a brilliant insight into what is happening today versus the past.

Stock Valuations in July 2020 vs. March 2024

Let’s flash back to July 2020. The S&P Composite was 119% above the trend line. That mark was much higher than it was after the roaring 20s, much higher than it was before the Financial Crisis in 2007, and higher than it was before the Dot-Com Bubble burst in 2000.

Today, the S&P Composite sits at 154% above the trend line! The stock market is definitely overvalued from a historical perspective. However, it’s been overvalued for the last 20 years except for a brief dip below trend by early 2009 that quickly reversed.

Remember what I said at the outset that markets can remain over or undervalued for FAR longer than anyone thinks. You certainly wouldn’t want to use this information to make short-term trading decisions because you would have been wrong for the last 20 years. Let’s look at Figure 2, which is the same as Figure 1 except that the trend line set to zero.

Standard Deviations

Notice the standard deviation marks above and below the trend line. In this case, one standard deviation is 45%. The peak of the market just before the Great Depression was two standard deviations above trend, and it subsequently fell to roughly one-and-a-half standard deviations below trend (-67%) before it bottomed. The year 2000 saw a peak at almost three standard deviations. If you remember the bell curve,3 three standard deviations is where 99.7% of all occurrences will be found.

Today, even after the wild swings in the market caused by rising interest rates in 2022, we’re well over three standard deviations above trend. Some would call that Black Swan territory. Can we go higher? Absolutely. The question is how much, and for how long? Or is it? Maybe we need to talk about how market overvaluations come back to trend or fair value, which is what we’ll refer to trend as in the next segment, before we move on.

How Does an Overvalued Market Get Back to “Fair Value?”

Remember the formula to figure out the P/E ratio is share price divided by earnings per share. So, the higher the share price is versus the denominator of earnings, the higher the P/E will be. What could change that?

Well, first of all, the price could come down. The lower price to the steady earnings would lower the P/E ratio. But what if the price stayed flat at their elevated levels, and earnings came up to meet or exceed expectations? If my earnings per share are higher compared to the price per share, my P/E goes down without the price having to come down. Are you following me here?

Let’s take our stock with a P/E of 20 from earlier and assume that the share price is $20 and the earnings per share is $1. That’s our P/E of 20. Now, let’s assume that the earnings per share doubled to $2. Under that scenario, my new P/E is 10!

Suddenly, an overvalued stock is undervalued, and the price didn’t change. Conversely, but much more painfully for the shareholders, if the price drops by 50% to $10 and the earnings per share remain the same at $1, my new P/E is also 10. It may be a bargain, but someone suffered for someone else to get a bargain. As we continue, these are the two ways that a market that appears to be overvalued today can come back to fair value. Let’s move on now.

Shiller, Crestmont, and Tobin in Detail

Shiller, Easterling, and Tobin are all exceptionally intelligent men. I’m so thankful for their work in this area because they’ve given me the ability to get the detailed, long-range historical look back I need in doing my job. So, let’s break down each of their valuation measurements and I’ll give you examples of each. Then, we’ll tie it all together via the work of Advisor Perspectives in blending the valuations from each into one composite valuation indicator.

Valuations Using Trailing 12-Month Earnings

We’ll start with Shiller because he’s probably the most recognizable name. Let’s first look at the anomalies that can happen with valuations using trailing 12-month earnings to calculate P/E. Notice the spike in Figure 3, below, in the middle of the financial crisis.

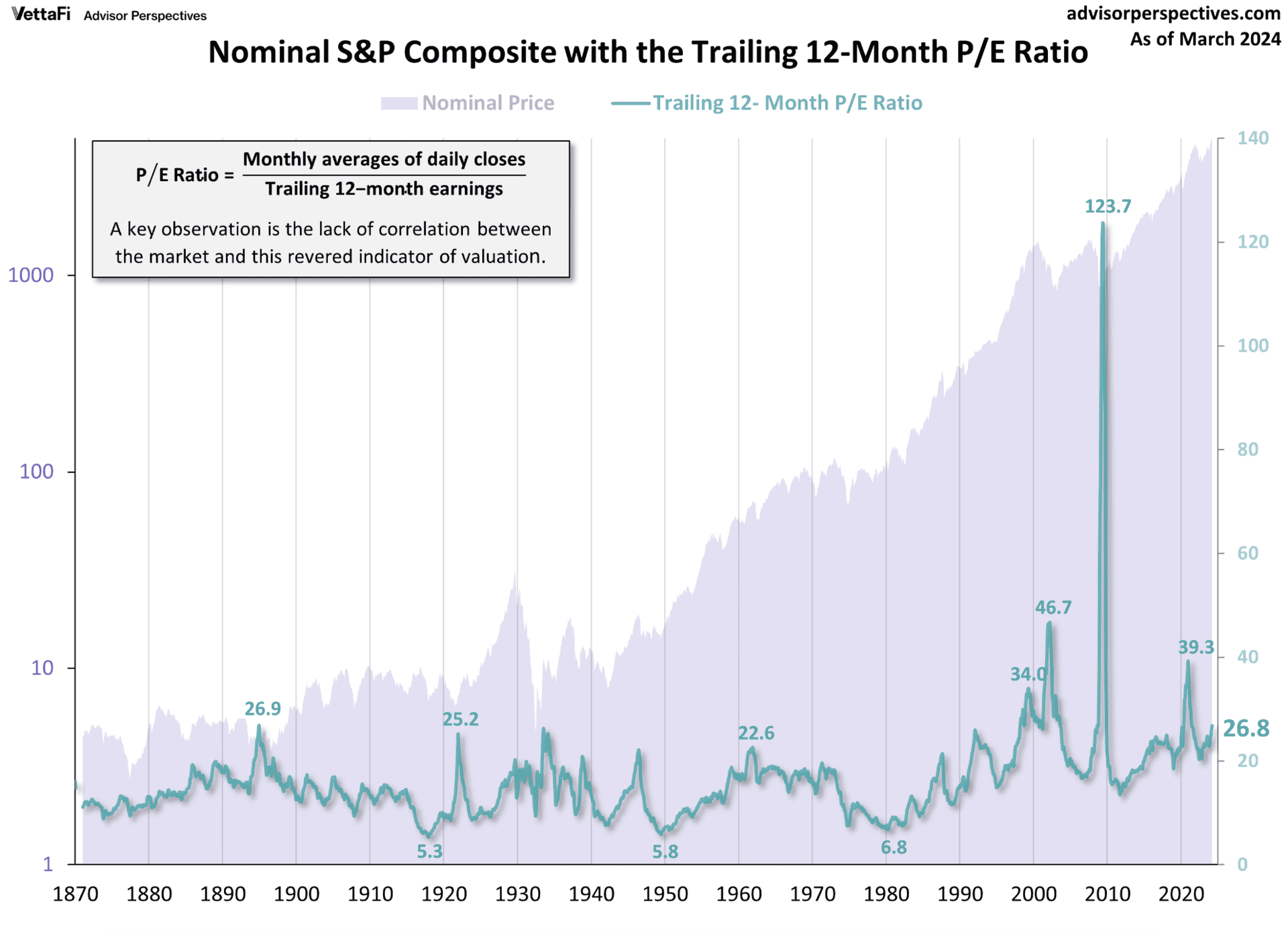

FIGURE 3 – Nominal S&P Composite with the Trailing 12-Month P/E Ratio – Advisor Perspectives4

The P/E of the S&P Composite spiked to 123.7 in 2009, as prices were cratering. Based on our discussion about how markets get back to fair value, this should never have happened. But it did. The problem was that earnings fell faster than prices in that timeframe and actually went negative. That had never happened in the history of the S&P. Thus, you get P/E readings that are absolutely meaningless and downright misleading.

In a book titled, Security Analysis,5 which was written by Economist Benjamin Graham and David Dodd in 1934, the co-authors noted the same wild P/E trends during the Roaring 20s and Great Depression. Therefore, they wanted to determine a more accurate way to calculate the market’s value. As a result of their work, they determined that the illogical P/E ratios they witnessed were due to temporary, and sometimes extreme, fluctuations in the business cycle.

Using a Multi-Year Average of Earnings

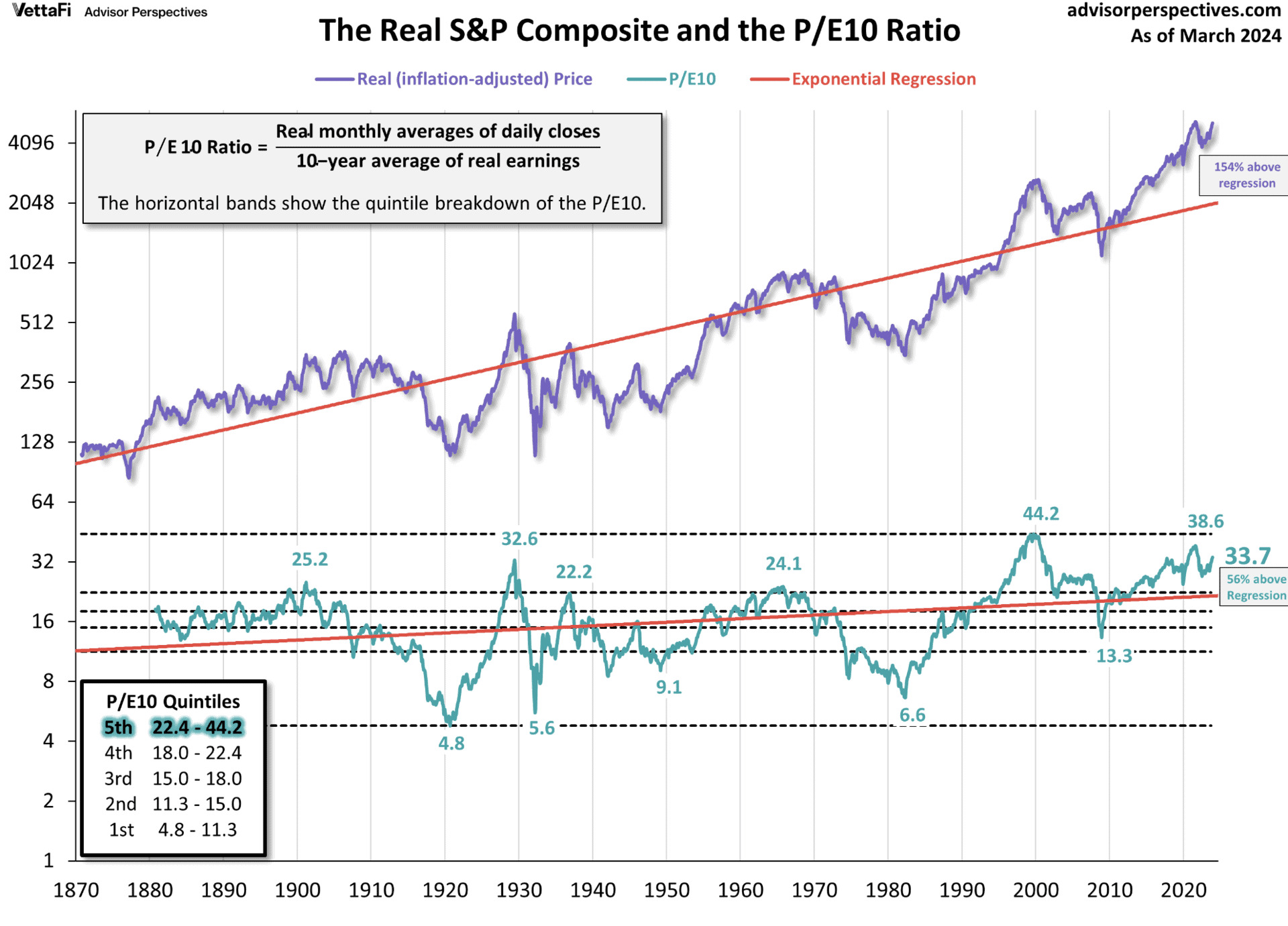

Their solution was to divide the price by a multi-year average of earnings and suggested five, seven, or 10 years. Shiller, who is a Yale professor and Nobel laureate, has taken this concept and made it readily available to all investors. He selected the 10-year average of “real” (inflation-adjusted) earnings as the denominator. Shiller refers to this ratio as the Cyclically Adjusted Price Earnings Ratio (CAPE). This is also referred to as the P/E 10 ratio because it uses the 10 years trailing.

FIGURE 4 – The Real S&P Composite and the P/E 10 Ratio – Advisor Perspectives6

Figure 4, above, shows the trend regression of the CAPE or P/E 10 going all the way back to 1871 versus the S&P Composite. Note the eerie similarity. It’s interesting to note that the average CAPE over this timeframe is 17. At the end of June in 2020, we were sitting at 29. Today, we are at 33.7.

The Stock Market Is Overvalued … But It Could Go Higher

While that is certainly elevated, it’s not the highest levels we’ve seen by a long shot. Even though the market is clearly overvalued today, it can obviously go higher if history is our guide based on these numbers.

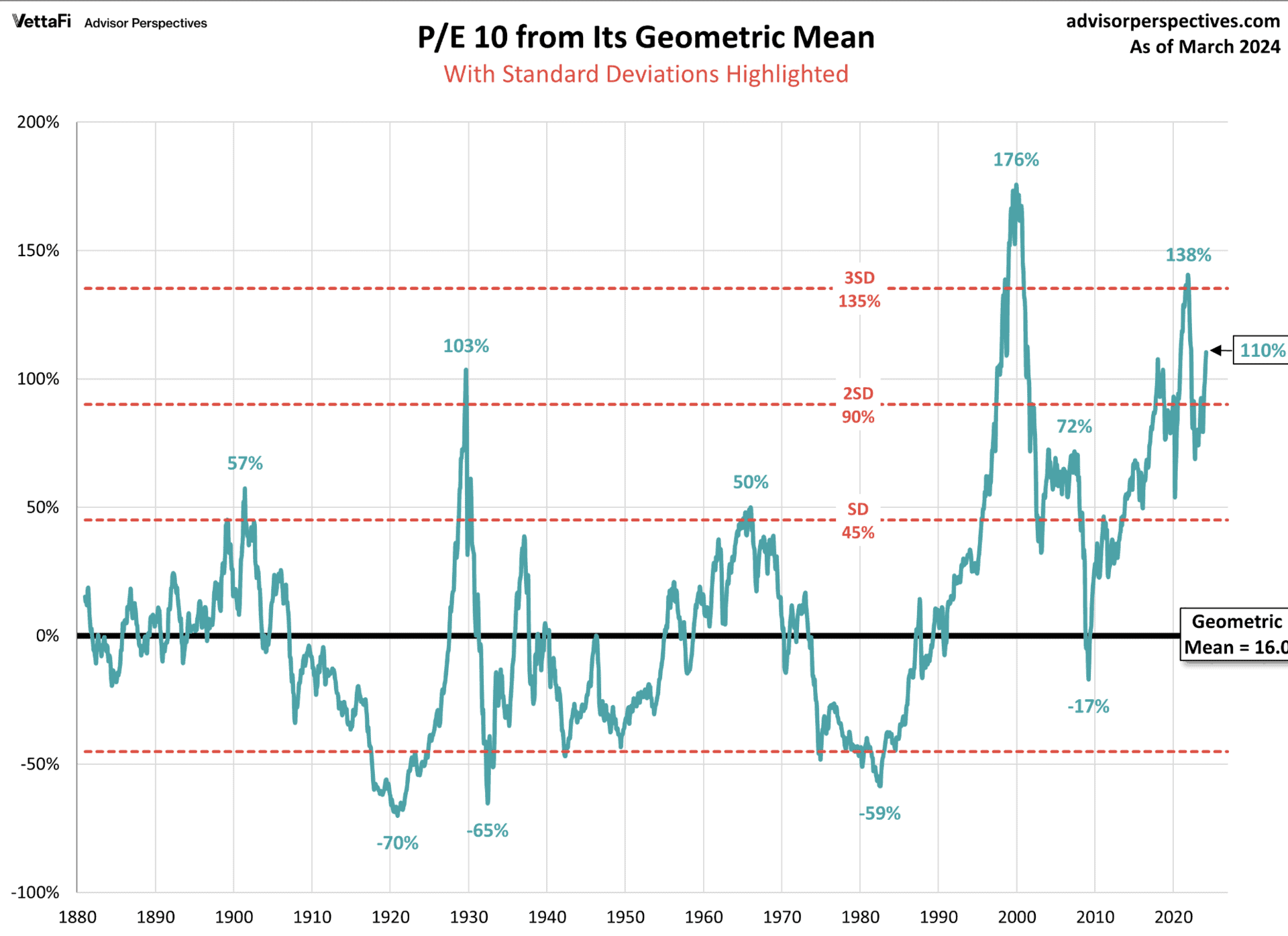

Viewed in a different way, you can see in Figure 5, below, the overvaluation shown as a percentage above the mean valuation which is shown as the zero line. The CAPE is currently 110% above its mean valuation, which is quite elevated.

Back in 2020, it sat at 84% above its mean. You can see the effects of the interest rate, tariff, and COVID panics which have occurred since the fourth quarter of 2018 in the far-right hand side of Figure 5 as valuations fluctuated wildly. And though there have been plenty of market drops over that time, valuations have remained extremely elevated.

The Relationship Between GDP and Earnings

Easterling recognized the value in the methodology of Shiller’s CAPE. However, Easterling also found that the inherent time lag in values could be a drawback and decided to modify the calculation to account for current economic growth. Easterling’s theory uses the fundamental relationship between Gross Domestic Product (GDP) and earnings. In his article titled, P/E So Many Choices: Part 1,8 that he published in 2011, he notes the following:

“The fundamental relationship is driven by two elements. First, GDP essentially represents composite revenues. Second, profits emanate from revenues. Therefore, over time, profits grow in line with economic growth.” – Ed Easterling, Crestmont Research Founder

“Although economic growth has some variability, earnings has its own cycle from the business cycle of competitive market forces. It is the second cycle that most affects EPS due to its frequency and magnitude. Over time, however, EPS reverts to its baseline relationship to GDP. Economists recognize that the profit margins cycle is one of the most mean-reverting cycles in the economy. Therefore, profits (as reflects in EPS for public companies) has a strong and fundamentally driven relationship with GDP.” – Ed Easterling, Crestmont Research Founder

To obtain a normalized EPS for his valuations, Easterling uses overlapping 50-year regressions of nominal GDP and actual reported EPS. This allows him to smooth the business cycle distortions in the EPS and to generate an accurate current valuation. The results look very similar to the CAPE, though their values are different. Take a look below in Figure 6.

Comparing Valuation Methodologies

Note how they both eliminated the crazy spike in P/E that occurred in 2009. Both methodologies work as intended and both provide valuable insight. While some prefer to choose one over the other, I believe more information is better, which is why I like them both. Figures 7 and 8, below, show the Crestmont regression and overvaluation that look very similar to those of the Shiller CAPE in Figures 4 and 5.

Note that Figure 8 really illustrates the effect of using the GDP and earnings data that Easterling included in his valuation method. His calculation shows the market is currently overvalued by a full three standard deviations—almost as high as the valuations of 2000 just prior to the Dot-Com Bubble bursting.

It also shows that the Crestmont hit a peak HIGHER than the Dot-Com Bubble in February of 2020—again a factor of using the GDP and earnings regression data in the calculation. Figure 8 is probably the most troubling chart of any you’ll see, for obvious reasons. We were above four standard deviations at the end of 2021 and are currently on our way back to those levels.

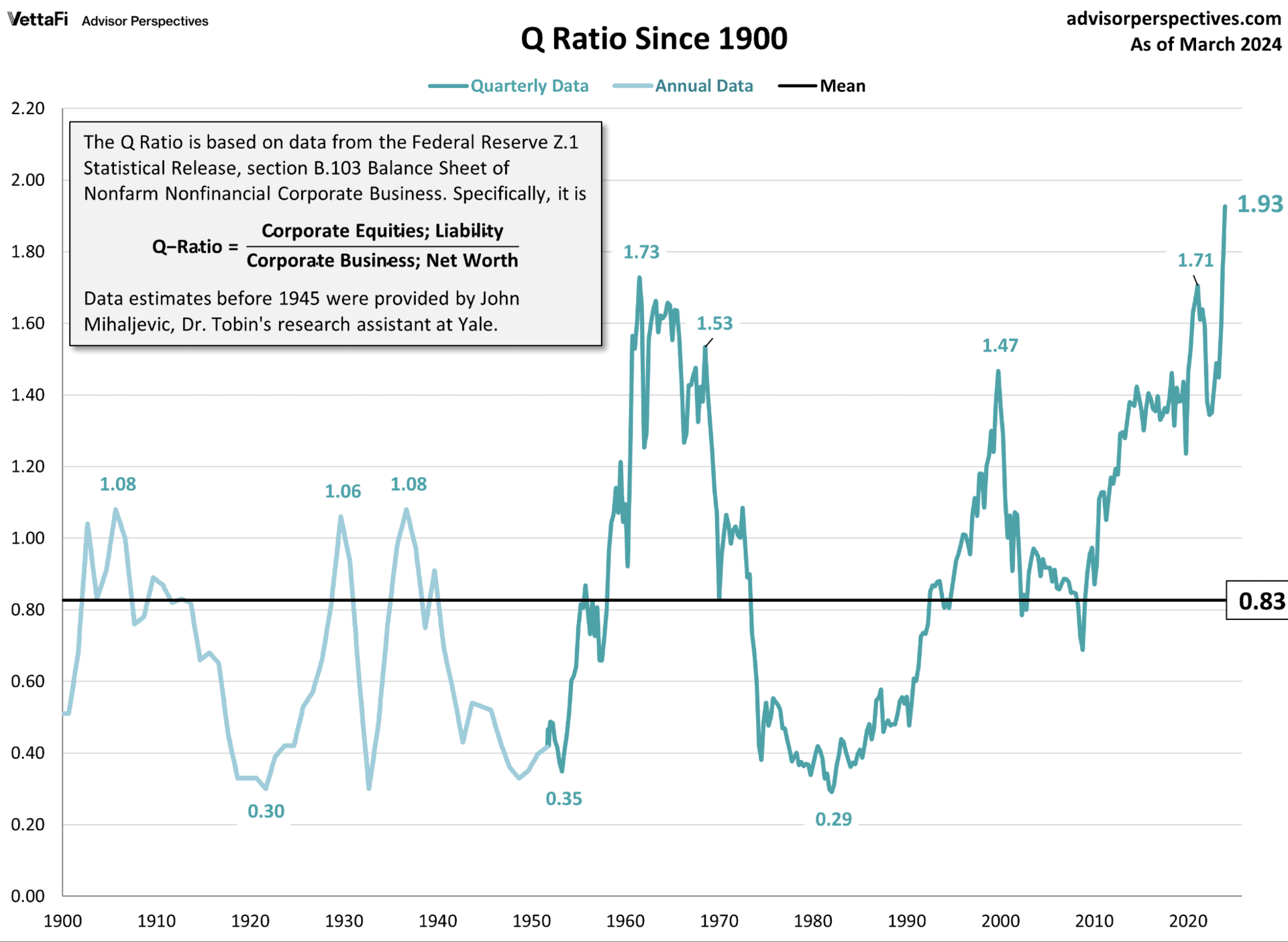

The Q Ratio

And finally let’s talk about Tobin’s Q ratio before we tie all these measures together. Tobin developed his Q ratio as a measurement of the total value of the market, divided by the replacement cost of all its companies. This data is found in the Federal Reserve Z.1 Statistical Release, section B.103, Balance Sheet and Reconciliation Tables for Nonfinancial Corporate Business.12

The drawback for Tobin is that the data is always lagging by two months and is only updated quarterly. As a surrogate, for monthly calculations, they use the Vanguard Total Market ETF to represent corporate equities. The average Q ratio today is .83,13 which is a little counterintuitive. One might think that a ratio of 1:1 would represent fair value, but the replacement costs of corporate assets tend to be overstated. Shocking right?

Figures 9 and 10, below, show the current levels of the Q ratio.

FIGURE 9 – Q Ratio Since 1900 – Advisor Perspectives14

Note here that the Q ratio meant that a company in 2000 was priced at 1.47 times the replacement cost of ALL its assets. That seems pretty steep to me. In 2020, the Q ratio was at 1.7 times total replacement cost, and today it sets at 1.93.

FIGURE 10 – Q Ratio Percent Change from Its Geometric – Advisor Perspectives15

The Q ratio today is currently just over three standard deviations above its mean, which indicates a pretty overvalued market. It’s 159% above mean, or fair value, well above the 2020 peak of 129% above fair value.

The Correlation Between the Valuation Methodologies

Taken by themselves, the Composite regression, the CAPE, the Crestmont, and the Q ratio are all exceedingly valuable tools. They were created by exceptionally intelligent people to help us understand the value of the market and whether it’s expensive or cheap.

However, when you blend them all into a single measurement, you get a valuation measurement that is taking advantage of the strengths and minimizing the weaknesses of all of them. Let’s first look at all of them together in Figure 11 to see the correlation between the four.

FIGURE 11 – Market Valuation Methods Adjusted to Their Geometric Means – Advisor Perspectives16

The correlation is undeniable, but the differences are also recognizable. That, to me, is the beauty of this blend of measurements. But it’s a little difficult to read Figure 11 with it being so busy. I look at the updated version of Figure 12, below, every month without fail because it distills all the information down into one combined valuation measurement that is easy to read and understand.

The Stock Market Is Overvalued … Where Could It Go from Here?

See what I mean? Clear, concise, and to the point. It also answers the question we asked at the beginning of the article, Is the Stock Market Overvalued? The answer is obviously yes. However, keep in mind what we also talked about at the beginning of the article.

The markets can, and do, remain elevated for far longer than anyone thinks is possible. And, with history as our guide, they can go quite a bit higher from here without setting a new record. They are currently 148% above the mean valuation going back to 1871, but they were 162% above mean valuation at the end 2021, and 127% above just before the Dot-Com Bubble burst in 2000.

Circling Back Again to 2020

Before I wrap up this article, I want to circle back again to the research I was doing in 2020 as I was consistently assessing whether the stock market was overvalued. In July 2020, there were two big near-term questions that were top of mind.

- Was the economy going to keep expanding after the post-COVID panic?

- Would states allow their economies to remain open for business and not make the same economically disastrous decisions they made in March?

Mercifully, the economic growth did continue from that time, so much so that we had some very uncomfortable inflationary pressure that the fed had to step in and try and tame in 2022 with steep and rapid interest rate hikes. Now, inflation has slowed, and there’s even talks of a rate reduction at some point this year. Should that happen, today’s monstrous valuation numbers may get even larger. Only time will tell, and we will know soon enough.

In the meantime, if you have any questions about market valuations or anything else that I’ve covered in this article, start a conversation with our team below.

I hope you’ve found this article to be informative, and will be sure to report back with more education on market valuations as I continue to pose the question, is the stock market overvalued?

Resources Mentioned in This Article

Other Sources

- [1 and 2] https://www.advisorperspectives.com/dshort/updates/2024/04/02/regression-to-trend-s-p-composite-154-above-trend-in-march

- [3] https://www.investopedia.com/terms/b/bell-curve.asp#

- [4, 6, and 7] https://www.advisorperspectives.com/dshort/updates/2024/04/02/p-e10-and-market-valuation-march-2024

- [5] https://www.amazon.com/Security-Analysis-Classic-1934-GRAHAM/dp/0070244960

- [8] https://www.advisorperspectives.com/dshort/updates/2011/04/26/p-e-so-many-choices-part-1

- [9] https://www.crestmontresearch.com/docs/Stock-PE-Report.pdf

- [10 and 11] https://www.advisorperspectives.com/dshort/updates/2024/04/02/crestmont-p-e-and-market-valuation-march-2024

- [12] https://www.federalreserve.gov/apps/fof/DisplayTable.aspx?t=b.103

- [13, 14, and 15] https://www.advisorperspectives.com/dshort/updates/2024/04/02/q-ratio-and-market-valuation-march-2024

- [16 and 17] https://www.advisorperspectives.com/dshort/updates/2024/04/02/market-valuation-is-the-market-still-overvalued

Investment advisory services offered through Modern Wealth Management, LLC, an SEC registered investment adviser. Securities offered through Mutual Securities, Inc., Member FINRA/SIPC. Modern Wealth Management, LLC and Mutual Securities, Inc. are not affiliated companies.

The views expressed herein represent the opinion of Modern Wealth Management, an SEC Registered Investment Adviser. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.