How Much Does a Single Person Need to Retire?

Key Points – How Much Does a Single Person Need to Retire?

- Key Retirement Questions to Ask Yourself

- Retirement Planning for Singles vs. Retirement Planning for Couples

- Income Planning for Retirement

- Creating a Spending Plan for Retirement

- 7-Minute Read

Retirement Planning as a Single Individual vs. Retirement Planning as a Couple

One of the challenges that couples have with retirement planning is making sure that they have a comprehensive financial plan that is tailored to each partner’s needs, wants, and wishes. While financial plans for single individuals don’t have the challenge, there are several unique planning considerations that may apply to them.

While married individuals can eventually become single via the death of their spouse or divorce, we want to focus on financial planning considerations for individuals who have been single by choice. There is an independence factor that single individuals have that plays a large role in the retirement planning process. How can single individuals go about building a support system for themselves in their retirement years since they don’t have a spouse and may or may not have children?

At Modern Wealth Management, we don’t want anyone to feel alone or unsure about how to support themselves financially throughout retirement. There are many different components that come into play with retirement income planning. That’s why we’ve built a team of professionals, which includes specialists in tax, estate, insurance, and investments, to support our advisors (and therefore, our clients). It’s important to us that everyone — single individuals and couples — can enjoy today with confidence for tomorrow. Let’s dive into some specific planning considerations that we frequently address with single individuals as they plan for retirement.

Schedule a Meeting Get the Retirement Plan Checklist

How Much Money Will a Single Person Need for Retirement?

Whether single or married, there is one question that so many people want a quick answer to when planning for retirement: how much do I need to retire? Well, we do have a quick answer to that question, but it’s not a number. The answer is, “it depends.” For example, let’s say that a couple determines that they need $X amount for retirement. That doesn’t mean that a single individual might just need half that amount for retirement.

How much you need for retirement depends on so many different factors, including your goals, desired lifestyle in retirement, your health, life expectancy — the list goes on and on. So, what do you want your life to look like in retirement? Do you want to travel a lot, spend time with family and close friends, or pick up a new hobby that you haven’t had time to pick up while working?

Creating a Spending Plan for Retirement

Keep in mind that your current expenses may be much different in retirement than they are while you’re working. It’s important to create a spending plan (A.K.A., a budget) for retirement rather than just assume that you’ll have the same spending habits as you did before retirement.

As you plan for retirement, break it down into three different stages: your go-go, slow-go, and no-go years. You may want to consider front-loading your spending in retirement. Take advantage of your go-go years while you’re hopefully in good health rather than putting off your dreams. Also, keep in mind that you might not need to wait until retirement to start pursuing some of your dreams. Prioritize them within your financial plan to help build confidence in your financial future.

During your slow-go years, you may still be in good health, but just don’t quite have the same energy and ability to be as active as you were during your go-go years. In turn, you may not need to spend as much as you did during your go-go years.

Then, you have your no-go years, where you spending may increase in large part due to health care costs. If you require long-term care, do you plan to self-insure or purchase long-term care insurance? That’s obviously not something that’s fun to think about, but it’s a very important for consideration for single individuals, especially if they don’t have children, siblings, or other family members that can help care for them.

Even if you plan to age in place and have family members who may be willing to help care for you, take some time to research long-term care options while you’re still healthy. There’s a substantial cost that comes with long-term care, whether you’re self-insuring or using insurance.

When Do You Plan to Retire?

Whether you’re single or married, do you have a plan that’s built on the foundation of hope, or do you have a plan that’s been stress-tested for the possibility of a long-term care stay, prolonged market downturn, and other potential risks during retirement? Don’t just assume that your investments will be able to outproduce your withdrawal rate. No one know what the markets will do over the course of your retirement.

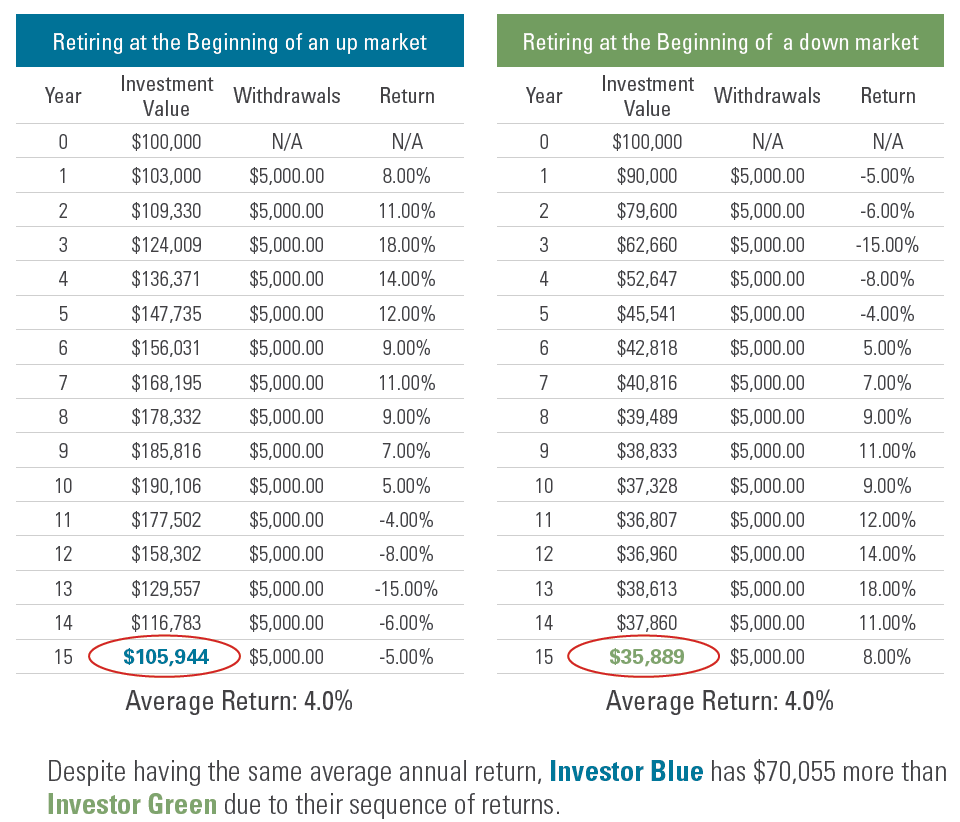

Additionally, it’s important to understand that when you retire matters. It’s one thing for a prolonged market downturn to occur later in your retirement. It’s another for one to occur at the beginning of your retirement. This is because of sequence of returns risk. Figure 1, below, from Simplicity OID shows an example of two investors that start a 15-year period with $100,000 apiece and have an average annual return of 4%.1 One investor retired at the beginning of an up market and ended the 15-year period with $105,944. The other retired at the beginning of a down market and ended with $35,889.

Educational content only. Examples are simplified and not a projection of any investment, strategy, or account. This is not individualized advice or a recommendation. Actual results vary, and investing involves risk, including possible loss of principal.

FIGURE 1 – What Is Sequence of Returns Risk? – Simplicity OID

While there is no way of knowing whether you’ll retire at the beginning of a down market, it’s important to prepare for that possibility. Establishing an emergency fund and maintaining a diversified investment portfolio are strategies that may help manage the impact of market volatility and sequence of returns risk.

How Long Will Your Retirement Last?

This is another question that no one knows that answer to, but it’s critical to think about, especially with people projected to live longer on average. According to the World Health Organization, the number of people who are 80 and older is projected to triple from 2020 to 2050.2 Living longer obviously presents opportunity to create more special memories, but the cost of those memories is also likely to be more expensive in 2050 than they are in 2020 due to inflation.

As you stress test your financial plan, longevity risk and inflation are two crucial components that come into play. You’ll also notice that they are both items that are mentioned as a part of our Retirement Plan Checklist. This white paper consists of a 30-question yes-or-no checklist to help gauge your retirement readiness as well as age-and date-based timelines that address key retirement planning considerations. Download your copy today and keep it handy throughout the retirement planning process.

Tax and Estate Planning Considerations for Single Individuals

It’s worth reiterating that there’s much more to retirement income planning than investment management. Taxes and estate planning are also two of Modern Wealth’s Advantage Offerings, and both have unique considerations for single individuals. Let’s start with taxes.

Understanding the Tax Brackets

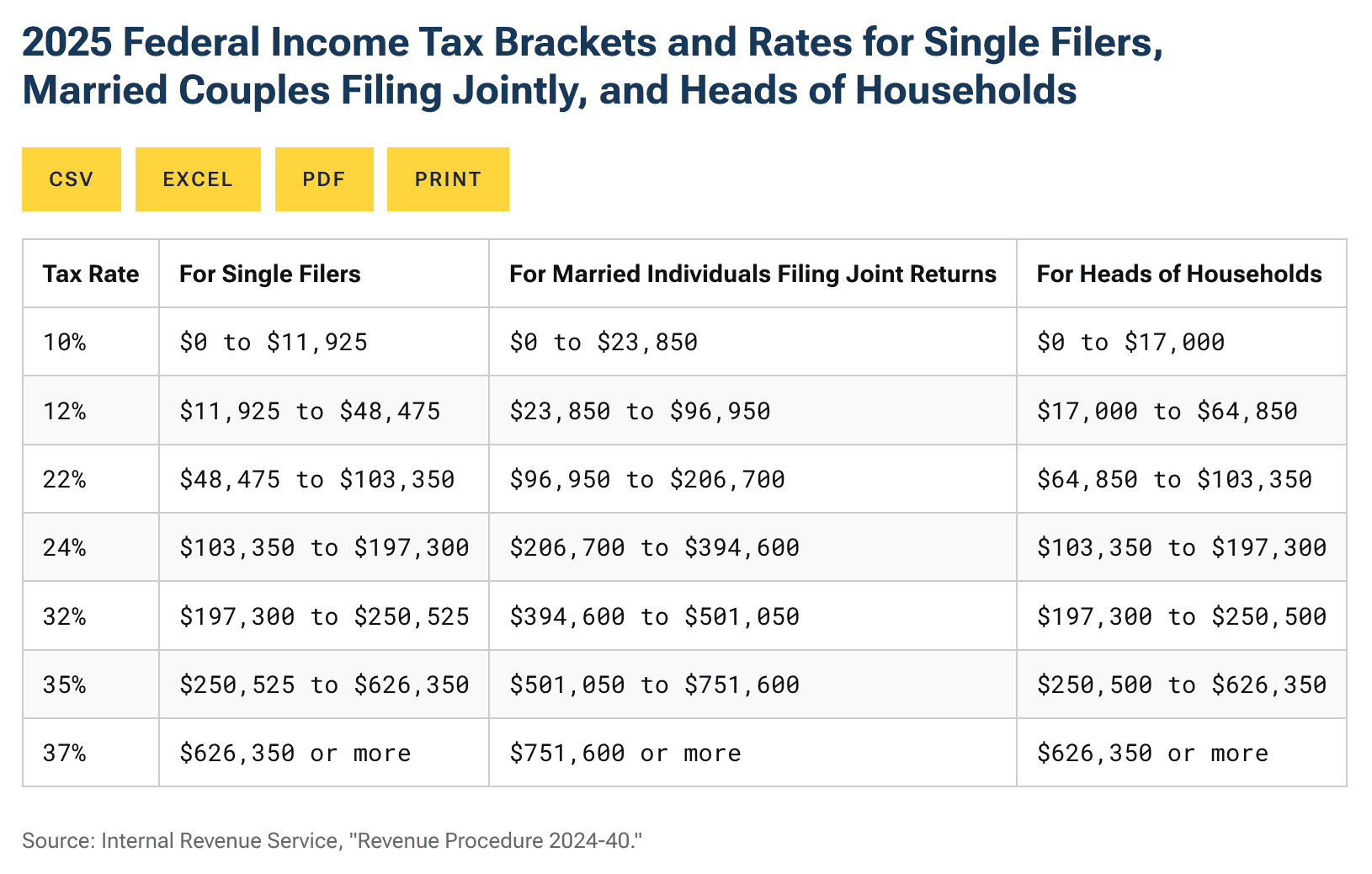

Hopefully you’ve started to at least gather your 2025 tax documents, but whether you have or not, let’s look at the 2025 federal income tax brackets.

FIGURE 2 – 2025 Tax Brackets – Tax Foundation/IRS3

If you’re a single filer who made $100,000 in 2025, that will put you toward the top of the 22% bracket. Your first $11,925 will be taxed at 10%, your next $36,550 ($48,475 – $11,925) will be taxed at 12%, and the rest ($100,000 – $48,475 = $51,525) will be taxed at 22%.

However, if you’re married and filing jointly and made $100,000 in 2025, you would be on the bottom end of the 22% bracket. Your first $23,850 would be taxed at 10%, your next $73,100 ($96,950 – $23,850) would be taxed at 12%, and only $3,050 ($100,000 – $96,950) would be taxed at 22%.

But if your married and filing jointly in 2025 and you or your spouse suddenly passes away in retirement, keep in mind that the surviving spouse will possibly have similar income and become a single filer. The death of a spouse can have a significant impact on the surviving spouse’s long-term tax situation, which is a possibility that needs to be planned for.

Taxes on Retirement Income

Along with Social Security benefits, employer-sponsored retirement plans are typically one of the main sources of income for people in retirement. However, if you have $X amount in a traditional 401(k), remember that that is a tax-deferred asset. That means that the money will generally be taxed as ordinary income upon withdrawal. However, if you have a Roth 401(k), the money is taxed at the time the contribution is made, but withdrawals are tax-free under certain conditions.

Should You Consider Roth Conversions?

Prior to the One Big Beautiful Bill Act become law on July 4, 2025, the tax rates from the Tax Cuts and Jobs Act were scheduled to sunset after December 31, 2025. If that sunset had occurred, the higher pre-TCJA tax rates would have gone back into effect. OBBBA

“permanently” extended the TCJA tax rates, but that just means there is no sunset date for them to expire. So, make sure that you’re planning for the possibility of there being higher tax rates in retirement.

If you anticipate being in a higher tax bracket later in retirement, it may make sense to consider Roth conversions. When doing a Roth conversion, you’re converting funds from a traditional IRA to a Roth IRA. You’re required to pay tax on the converted funds, but they’ll be able to come out tax-free under certain conditions.

There are several pros and cons to doing Roth conversions. Roth conversions may help with reducing Required Minimum Distributions, in certain situations, which could affect long-term tax exposure. However, Roth conversions could push you up into a higher Medicare bracket if you’re unaware that your Medicare income-related monthly adjustment amount is determined based on your Modified Adjusted Gross Income from two years prior.

Also, if you’re charitably inclined, it may make sense to keep money in your traditional IRA until you’re 70½ or older. At that point, you’ll be eligible to make Qualified Charitable Distributions (QCDs) directly from your IRA to a qualified charity without it showing up on your tax return.

Speaking of Charities…

If you’re single and don’t have any children or grandchildren, who do you plan on leaving your inheritance to? Nieces and nephews might be possible options if you have siblings with children, but don’t forget about your favorite charities either. Regardless of your intentions when it comes to legacy planning, it’s important to have open and honest conversations with your family (and potentially charities) about your wishes. If you haven’t recently reviewed your beneficiaries and other estate planning documents, make sure to do so soon and update them if necessary.

How Much Does a Single Person Need to Retire?

If you were wondering how much a single person needs to retire prior to reading this article, can you now see why there are many factors for the answer being “it depends?” Whether you’ve been single for most of your career or you’re recently single following a divorce or death of a spouse, it’s important to have a team of wealth management professionals as a part of your support system.

If you have any questions about retirement planning considerations for single individuals, start a conversation with our team below.

Resources Mentioned in This Article

- 5 Types of Financial Plans

- Financial Checklist After the Death of a Spouse

- Gray Divorce and Its Financial Impact

- What Is a Good Monthly Retirement Income?

- Transition into Retirement Following These 5 Steps

- Setting Up a Spending Plan for Retirement

- Monthly Expenses for Everyone’s Budget

- 4 Phases of Retirement

- Mitigating Inflation on Healthcare Costs with These 7 Strategies

- 5 Questions to Ask About Long-Term Care

- Paying for Long-Term Care: Insurance vs. Self-Insuring

- Stress Testing Your Financial Plan

- 4 Retirement Risks That Are Out of Your Control

- What Is Market Risk?

- Why When You Retire Matters

- Sequence of Returns Risk and Why Timing Matters

- How Much Cash Reserves Should You Hold?

- Longevity Risk and How to Plan for It

- 10 Ways to Fight Inflation in Retirement

- 2025 Tax Brackets: IRS Makes Inflation Adjustments

- Maximize Social Security Benefits

- 10 Retirement Income Streams

- Traditional vs. Roth 401(k)

- The One Big Beautiful Bill Act: What You Need to Know

- New Tax Provisions in the One Big Beautiful Bill Act

- 2026 Tax Brackets: IRS Makes Inflation Adjustments

- Roth Conversion Strategies Under the One Big Beautiful Bill Act

- 6 Reasons to Roth Conversions Could Work for You

- How to Reduce RMDs with 5 Strategies

- 7 Reasons NOT to Convert to a Roth IRA

- What Is Modified Adjusted Gross Income?

- 5 Key Estate Planning Items to Address

Downloads

Other Sources

[1] https://simplicityoid.com/sequence-of-returns-risk/

[2] https://www.who.int/news-room/fact-sheets/detail/ageing-and-health

[3] https://taxfoundation.org/data/all/federal/2025-tax-brackets/

Investment advisory services offered through Modern Wealth Management, LLC., a Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management, a Registered Investment Advisor. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.