5 Long-Term Care Questions to Ask

Key Points – 5 Long-Term Care Questions to Ask

- Looking at What Factors Impact Long-Term Care Costs

- Explaining What Needs Are Addressed with Long-Term Care

- Average Long-Term Care Costs for 2023

- Properly Preparing for the Possibility of a Long-Term Care Stay

- 5 Minutes to Read | 23 Minutes to Watch

5 Long-Term Care Questions

Six months ago, Logan DeGraeve, CFP®, AIF® and Matt Kasper, CFP®, AIF® discussed rising long-term care costs on the Modern Wealth Management Education Series. To the surprise of no one, it appears to be a trend with no end in sight. There’s no question about that, but that doesn’t mean that we’re not receiving plenty of questions about long-term care.

In addition to sharing some staggering statistics, Dean Barber and Bud Kasper, CFP®, AIF® are going to address five questions that we’re frequently asked about when it comes to long-term care.

Schedule a Meeting Get the Retirement Plan Checklist

Long-Term Care Question No. 1: What Is Long-Term Care?

Before we break down the numbers of long-term care costs, we need to define exactly what long-term care entails. Long-term care includes the services and support that help someone meet their everyday needs. This type of care is typically available at adult day care, hospice care, and nursing home facilities.

Instead of being focused on health care, most long-term care facilities assist people’s daily activities, including as dressing, bathing, and cooking. Long-term care services can also include other tasks, such as managing money, caring for pets, and taking medication.

“This whole idea of long-term care seems to be a nagging concern for a lot of people that visit with us as they’re preparing to go into retirement. The earlier that you address the potential need for long-term care, the better off you’re going to be.” – Dean Barber

Long-Term Care Question No. 2: What Might Long-Term Care Cost You?

Now, let’s answer the long-term care question that everyone wants to know the answer to—how much could it cost? Well, it depends on several factors, but the costs can mount quickly. Since long-term care rates aren’t fixed, they can go up as you get older. It’s also important to remember that you can be disqualified from receiving long-term care insurance if you have health issues or pre-existing health conditions.

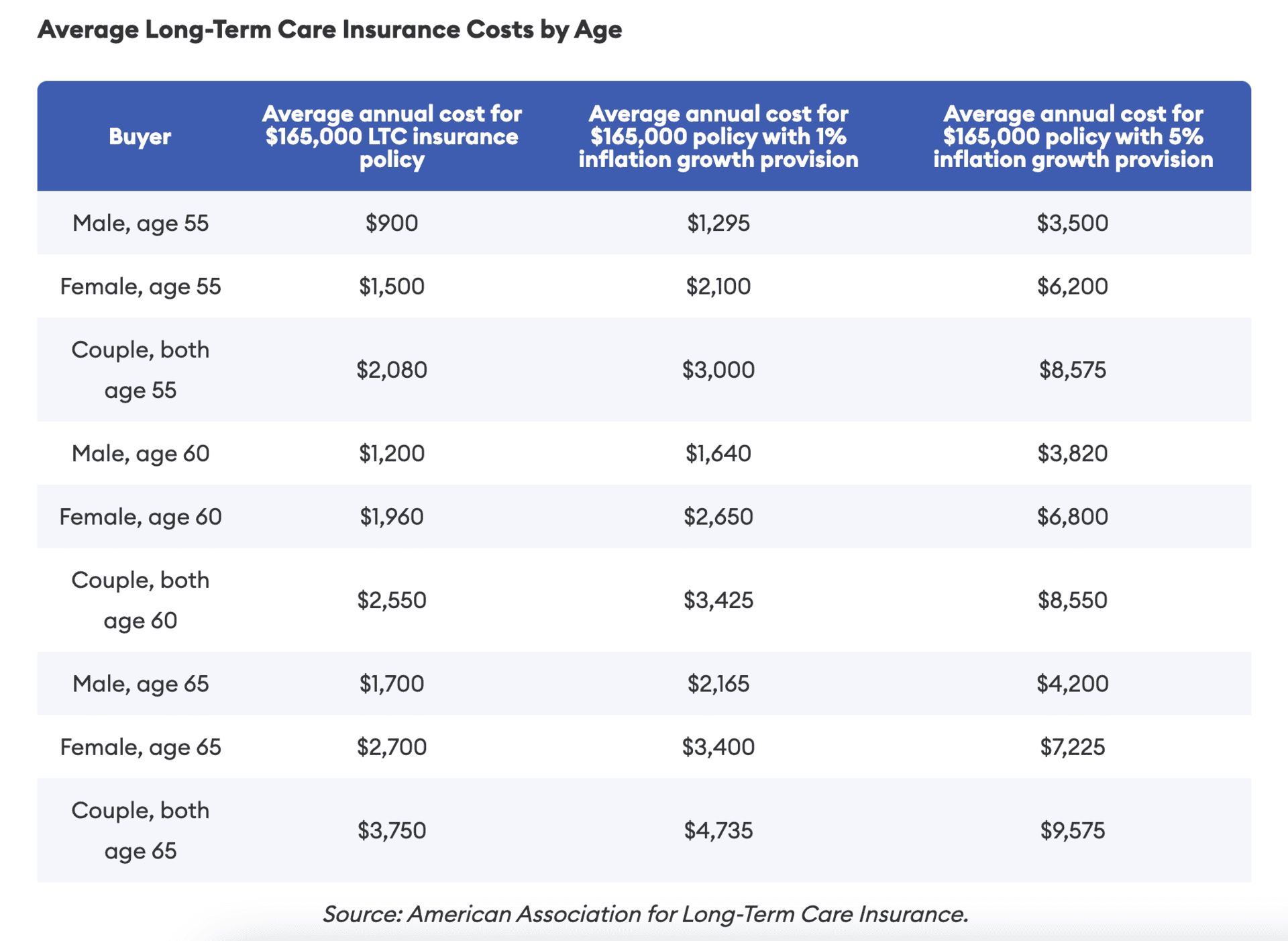

Figure 1, below, outlines the average costs for 55, 60, and 65-year olds to receive $165,000 a year in coverage. Notice that the joint policies cost less than spouses having separate policies. However, that $165,000 would be the total for both spouses combined. If you and your spouse had separate policies, you would each get $165,000 in coverage.

Long-Term Care Question No. 3: What Other Factors Impact Long-Term Care Costs?

You’ll also notice that insurance isn’t the only i-word in Figure 1. Inflation is one of the biggest factors that affects long-term care costs. Look at how much those long-term care costs increase when adding 1% and 5% inflation provisions. There are some obvious trade-offs with purchasing a policy with more protection against inflation. The inflation protection in this instance is an example of a rider, which offers added coverage.

Figure 1 also highlights that your age and gender are also significant factors with cost of long-term care insurance. Again, the younger you are, the less you will initially pay coverage wise.

If you’re a woman that’s looking at Figure 1, it’s probably hard not to be upset seeing that the rates for women are higher than men. Well, there are a couple of reasons for that according to the American Association for Long-Term Care Insurance. One, women live longer than men on average. Two, women tend to require long-term care more often than men.

We mentioned how bad health can disqualify you from being eligible for long-term care insurance. If you do have pre-existing health issues and end up being eligible, you will likely need to pay more for coverage. Long-term care insurance is also no different than other insurance in the sense that the rates will differ depending on what insurance company you select.

“When you look at the various long-term care policies out there, they vary dramatically. It’s best to know which will be best-suited for you.” – Bud Kasper, CFP®, AIF®

Long-Term Care Question No. 4: What Will Government Programs Pay for?

In our recent article, How to Build Generational Wealth, we mentioned that 10,000 Baby Boomers will turn 65 every day through 2030. As the world’s population continues to live longer, seven of 10 people are projected to need long-term care at some point in their life according to the Genworth’s 2023 Cost of Care Survey.

“There are very few of us who aren’t going to need long-term care. The question is, what are you doing today to factor that into your retirement plan? Obviously that’s going to be a financial drain, whether you’re pre-paying it or you have it at the time that you need it.” – Bud Kasper, CFP®, AIF®

That study found that most Americans expected that government programs would assist with at least a portion of their long-term care expenses. That’s usually not the case, though, as long-term care costs typically aren’t covered by health insurance or Medicare.

Medicare and Medicaid

When it comes to Medicare, adults with permanent disabilities/health issues could be eligible for long-term care insurance at a younger age. Medicare Part A can come into play here as well. It helps cover hospital bills for hospice care, inpatient care, and skilled nursing homes (for a limited time). However, copays, coinsurance, and deductibles are usually still required.

Medicaid does offer some coverage solely for Americans who struggle financially or have extremely high medical bills. It’s possible that you might need to spend down your assets to be eligible for Medicaid. Keep in mind that Medicaid coverage also varies depending on what state you live in. For more specifics on Medicaid and Medicare, visit medicaid.gov and medicare.gov.

Long-Term Care Question No. 5: How Can You Prepare?

Preparation is key with long-term care. Not factoring in the potential long-term care stay for you and/or your spouse into your financial plan can put you into a serious bind if one is needed. Planning for the unexpected is a critical component of financial planning. That includes the possibility that long-term care insurance costs will increase.

Recommendations from the National Association of Insurance Commission

Health care costs have been inflating at an even higher rate than the cost of everyday goods. That’s why we apply a 6.5% inflation factor to health care expenses when building financial plans compared to a 4% inflation factor for daily expenses. The National Association of Insurance Commission also suggests doing the following things to lessen the burden of long-term care costs:

- Increase the elimination period (the period prior to when a long-term care policy starts paying for claims).

- Lessen your inflation protection.

- Decrease the benefit period and the policy’s daily benefit

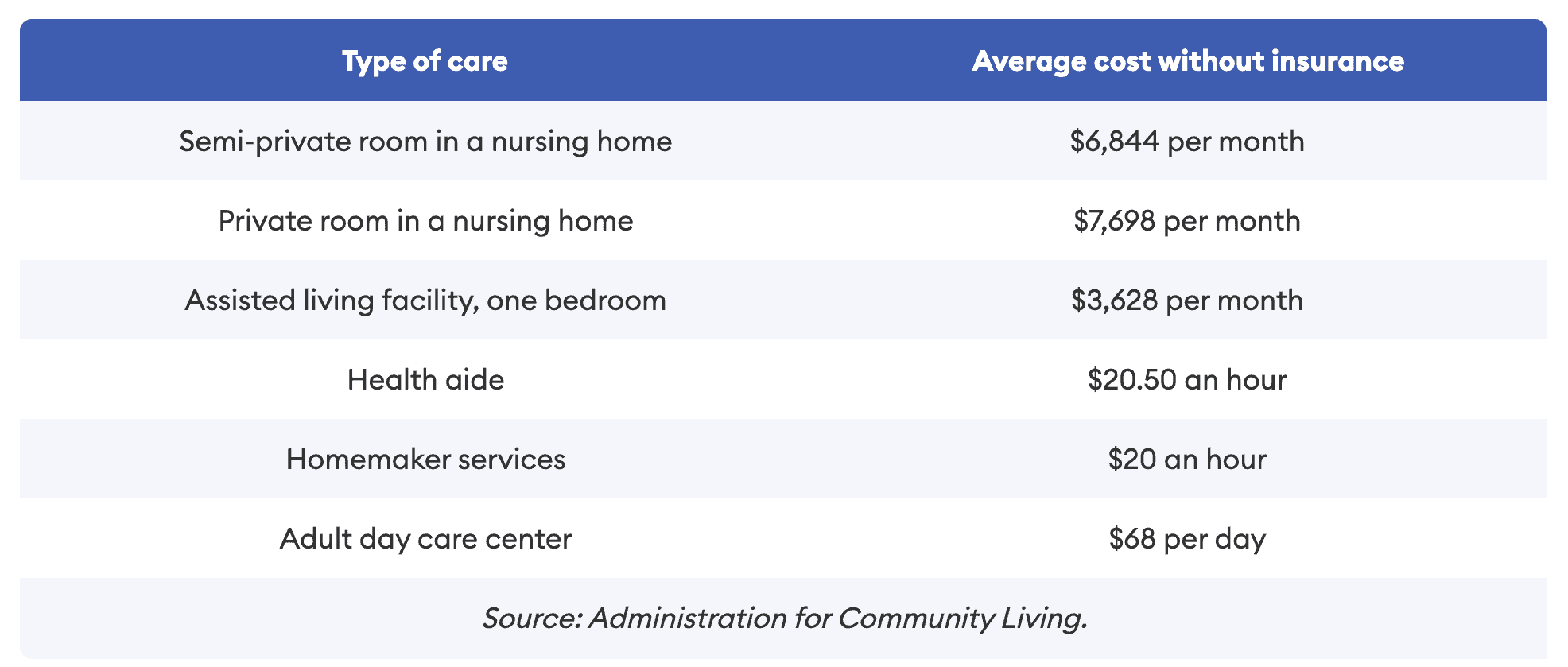

Again, there’s no question that long-term care insurance can be pricey. That being said, though, let’s look at the average cost for different types of long-term care costs without any long-term care insurance in Figure 2.

FIGURE 2 – Average Costs of Long-Term Care Prior to Insurance – Administration for Community Living

The Bottom Line with Long-Term Care

So, while long-term care insurance can be very expensive, those long-term care costs without insurance are also staggering. It’s important that you weigh all the pros and cons of long-term care insurance and ask yourself and your spouse these long-term care questions as you’re building and reviewing your financial plan.

“It’s expensive, but you don’t buy long-term care insurance for yourself. You buy it for your loved ones, whether it’s your surviving spouse or your children.” – Dean Barber

This is why we asked questions related to health care (and specifically long-term care) in our Retirement Plan Checklist. It’s a retirement planning resource that consists of 30 yes-or-no questions and an age-based timeline that gauges your retirement readiness. Download your copy below!

Making sure that you’re properly insured and still having plenty of income to support you and your spouse’s desired retirement lifestyles can be a tricky balancing act. It’s of the utmost importance to have a financial plan that gives you clarity and confidence when making these key decisions.

What About Keeping Life Insurance in Retirement?

It’s crucial to consider long-term care within your financial plan, but there’s also an alternative to long-term care insurance to keep in mind. Let’s talk about life insurance. If you buy life insurance, you know that you’re going to get money back out of the policy. If you go into long-term care, you might dwindle down your estate, but as soon as you pass on, the life insurance will come in tax-free and buoy back up the estate.

“That’s always been my preferred to address long-term care. When they put the critical care riders on life insurance that allows you to access some of the death benefit while you’re alive, it makes it even better.” – Dean Barber

Do You Have Any Additional Questions?

With there being so many nuances about health care expenses and insurance, it’s also critical to working with a team of financial professionals. In addition to having what we call the Three C’s—CFP® Professionals, CPAs, and CFAs—we also have insurance and estate specialists on staff at Modern Wealth. It’s important to have a team of professionals that works together to put your needs first.

If you want further clarification about the long-term care questions we addressed or have additional questions about long-term care, schedule a conversation with us so we can help you address them. Conversations about long-term care aren’t exactly fun, but they’re critical to have. We want to make sure that you’re educated to make the best decisions for you about long-term care.

5 Long-Term Care Questions to Ask | Watch Guide

00:00 – Introduction

02:03 – What are the 5 Questions?

03:07 – How Much Does Long-Term Care Cost?

04:34 – Who Do You Buy Long-Term Care Insurance for? (Hint: It’s not yourself)

07:13 – A Story About Our Retirement Plan Checklist

07:52 – TRIVIA: What % of Folks Over 65 Will Have a Severe Need for LTC?

08:37 – Surviving Spouses and Long-Term Care Insurance

12:26 – Bud’s Insurance Situation

15:16 – Digging Into Long-Term Care Costs Further

19:00 – Financial Planning Around Long-Term Care and Life Insurance

21:35 – What We Learned Today

Articles

- Rising Long-Term Care Costs

- How to Mitigate Inflation on Health Care Costs

- How to Build Generational Wealth

- Components of a Complete Financial Plan with Logan DeGraeve

- Financial Stress: How Do You Deal with It?

- Why You Need a Financial Planning Team with Jason Gordo

Past Shows

- 10 Ways to Fight Inflation in Retirement

- Retiring Before 65: What You Need to Consider

- Couples Retirement Planning: What You Need to Know

- Unexpected Expenses and How to Plan for Them

- What Is Financial Planning?

- Life Insurance in Retirement: Do I Still Need It?

Downloads

Schedule a Complimentary Consultation

Click below to get started. We can meet in-person, by virtual meeting, or by phone. Then it’s just two simple steps to schedule a time for your Complimentary Consultation.

Investment advisory services offered through Modern Wealth Management, LLC, an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Adviser. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.