What If We Go Back to Old Tax Rates?

Key Points – What If We Go Back to Old Tax Rates?

- Analyzing the Impact of the Tax Cuts and Jobs Act of 2017

- Will the TCJA Still Sunset After 2025?

- Comparing Current Tax Brackets with 2017/2026 Tax Brackets

- Differences Between CPI and Chained CPI

- Breaking Down Changes in Deductions and Exemptions

- 8 Minutes to Read

What If We Go Back to Old Tax Rates?

Significant tax code changes took place when the Tax Cuts and Jobs Act of 2017 was signed into law, such as reduced tax rates and an increased standard deduction.1 The legislation was so unpopular with Democrats that the Republican authors of the bill wrote in a sunset provision for most of the changes affecting individuals (the corporate tax law changes were made permanent) to work within budgetary constraints.

Well, that Tax Cuts and Jobs Act sunset provision is currently set to go into effect after 2025. That means if no additional legislation is passed between now and the end of 2025, much of the law would be reversed, and we would go back to many of the same tax laws we had prior to 2018.

However, remember that it was President Donald Trump who signed the TCJA into law during his first term in office. Now that he is back in office, extending the TCJA provisions before they sunset is one of his top priorities.2

We don’t have a crystal ball to tell you whether the Trump tax provisions will be extending before the end of the year. But here’s what we can tell you. Our team wants you to be prepared in the event the TCJA does sunset after 2025. Hence why we’re posing the question: What if we go back to old tax rates?

“We have been planning on a sunset after December 31, 2025, as a base case since TCJA was enacted. However, with the new administration, I believe a lot of provisions will be extended, but not permanently. We still need a plan for higher taxes by taking advantage of the current lower tax rate regime.” – Martin James, CPA, PFS

Understanding Tax Rates and Tax Brackets

One of the most significant changes for individuals was the change in tax brackets and rates on ordinary income. New rates and brackets were introduced in 2018, and those changes would be reversed if the TCJA sunsets. Remember that the brackets are adjusted for inflation each year, so while we’ve had different brackets since 2018, the rates haven’t changed.

As you’re filing your taxes for the 2024 tax year, you’ll be using the 2024 tax brackets. The IRS released the 2025 tax brackets in October.3 Comparing the 2024 and 2025 tax brackets will give you an idea of the inflation adjustments that were made.

2017 Tax Rates vs. Current Tax Rates

Let’s compare the 2017 (pre-TCJA) brackets with the 2024 and 2025 tax brackets.

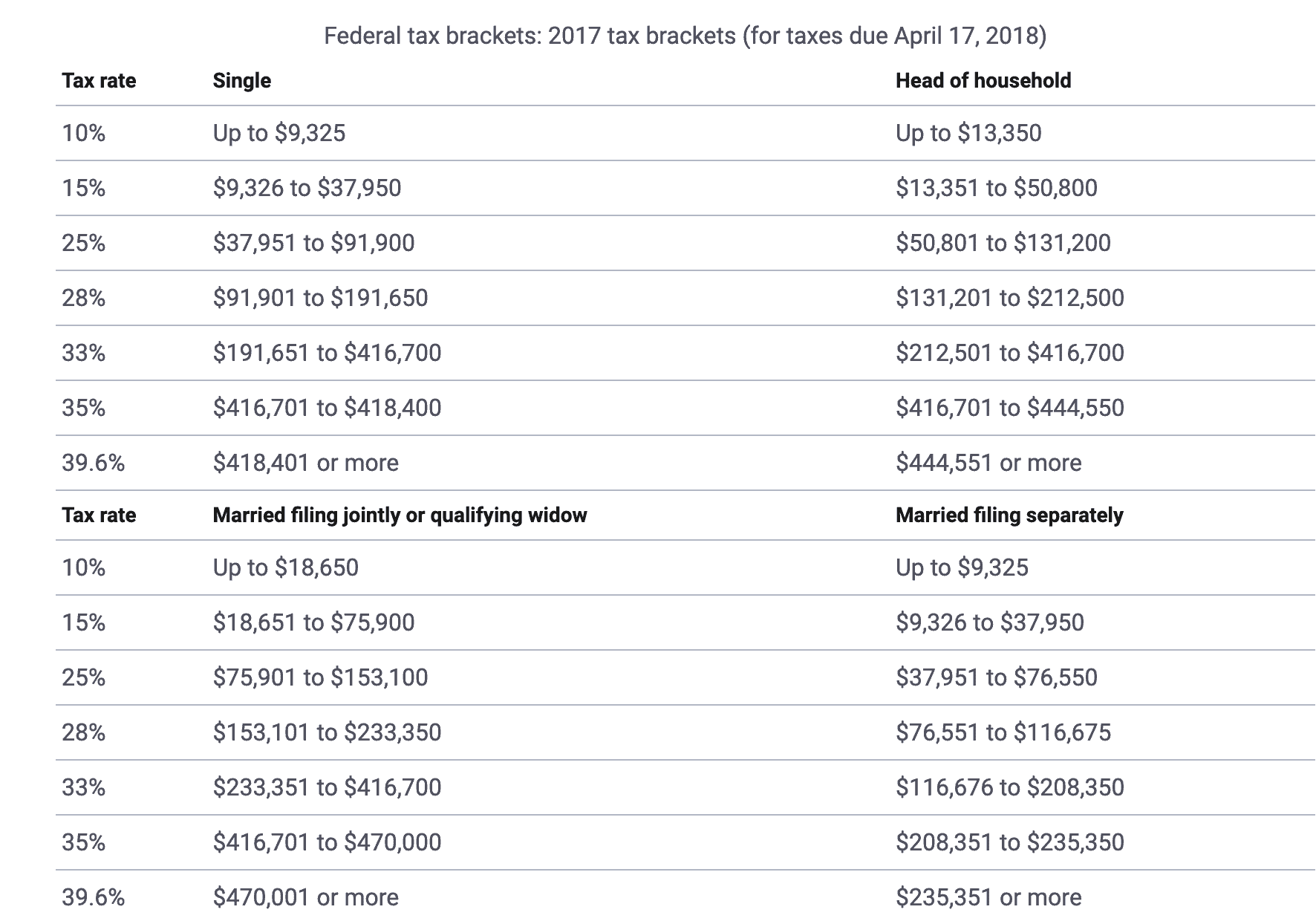

FIGURE 1 – 2017 Tax Brackets – Bankrate/IRS4

Notice that the tax rates from 2017 are set at 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%. Those will be the tax rates again in 2026 if the TCJA sunsets after 2025. Now, let’s see how those tax rates compare to the current tax rates.

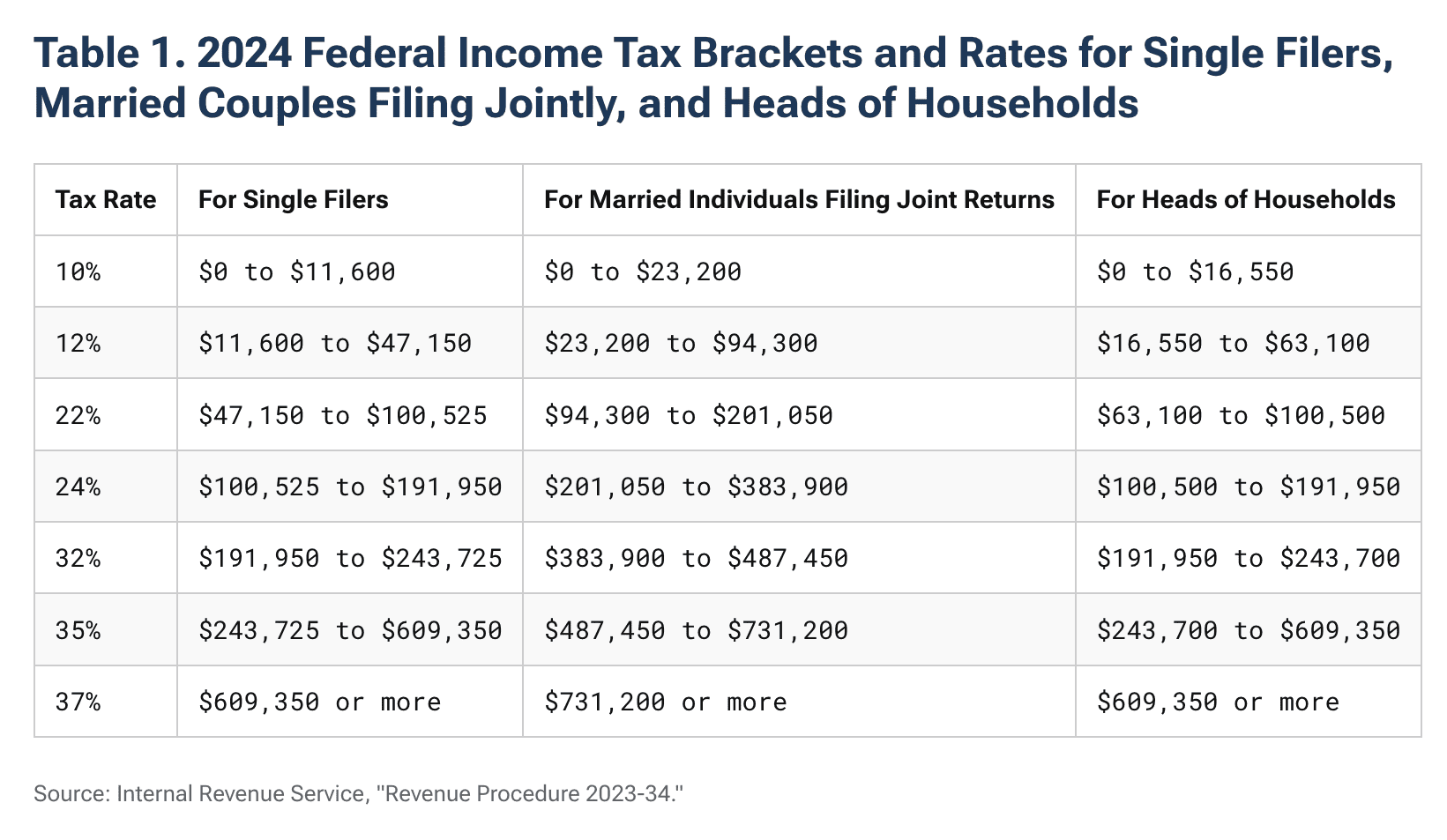

FIGURE 2 – 2024 Tax Brackets – Tax Foundation/IRS5

FIGURE 3 – 2025 Tax Brackets – Tax Foundation/IRS6

While the lowest bracket is at a 10% tax rate for the 2024 and 2025 tax brackets and the 2017 tax brackets, the other tax rates for the 2017 brackets were higher.7 If we go back to the pre-TCJA tax rates, the current 12% tax rate would increase to 15% in 2026. The current 22% tax rate would increase to 25%. The biggest jump would be the 24% tax rate increasing to 28%. Lastly, the current 32% tax rate would bump up to 33%, the 35% tax rate wouldn’t change, and the 37% tax rate would increase to 39.6%.

“Lower-and middle-income taxpayers could see significant increases in taxes, especially in retirement as Required Minimum Distributions begin. More of their Social Security benefits could be taxed with potentially moving the marginal bracket from 12% to 25% (see Figures 1 and 3). The effective rate will be higher as more Social Security is taxed. The death of a spouse will have a significant tax impact on the survivor, as they would now be filing single. Higher-income taxpayers will also see an impact, not only because the highest rate goes from 37% to 39.6% (see Figures 1 and 3), but also because of the realignment of how much money is taxed at each marginal rate.” – Martin James, CPA, PFS

Differences Between CPI and Chained CPI

The TCJA also included a major change to how inflation will adjust the tax brackets year by year. In the 1980s, the tax brackets were made to adjust annually by the consumer price index (CPI), an index tracked by the Bureau of Labor Statistics that is designed to measure the change in prices of consumer goods and services.

The TCJA made it so the tax brackets will adjust by Chained CPI instead of CPI. The Bureau of Labor Statistics has a good video on their YouTube channel explaining the difference between traditional CPI and Chained CPI if you want to have a good understanding for how tethering the tax brackets to Chained CPI will impact you.8

FIGURE 4 – CPI vs. Chained CPI — YCharts9

An article from the Congressional Budget Office spoke to the impact by saying, “The chained CPI-U results in lower estimates of inflation than the traditional CPI does. CBO expects that annual inflation as measured by the chained CPI-U will be about 0.25 percentage points lower, on average, than annual inflation as measured by the traditional CPI.10”

Translated to English – the tax brackets will not grow as “fast” in the future. Therefore, someone who was near to going into the next tax bracket and receiving regular increases to their income may wind up in the next higher tax bracket sooner. Of note, the tethering of the tax brackets to Chained CPI is a change that will not sunset after 2025.

Deductions and Exemptions

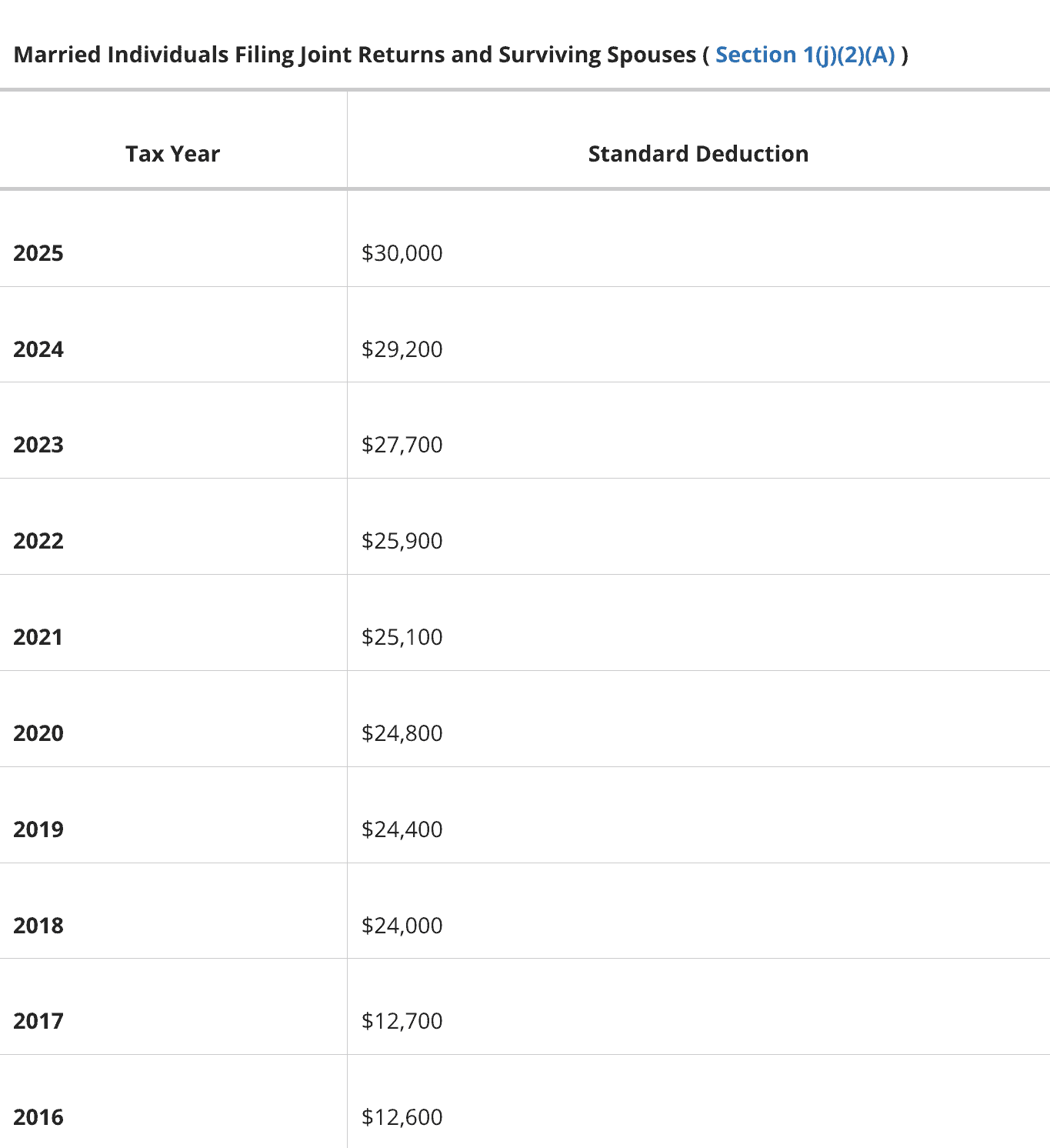

There was also a major change to deductions. Pre-TCJA, the standard deduction for a single tax filer was $6,350 ($12,700 for married filing jointly).11 The TCJA greatly increased the standard deduction. For the 2024 tax year, the deduction is $14,600 for a single tax filer and $29,200 for married filing jointly.

Inflation adjustments increased the standard deductions for the 2025 tax year to $15,000 for single filers and $30,000 for married filing jointly. So, if the TCJA does sunset, the standard deduction would be about half of what it is today come 2026.

“If we go back to the old standard deduction and personal exemption deductions, more taxpayers will again be itemizing. Alternative Minimum Tax could become a factor for more taxpayers, as itemized deductions and personal exemptions being phased out for higher income taxpayers.” – Martin James, CPA, PFS

FIGURE 5 – Standard Deductions – Tax Notes/IRS12

The SALT Cap

For example, state and local taxes (SALT) are capped at $10,000.13 For taxpayers in states with high tax rates, this greatly reduced the income deduction they could claim on their tax return. The TCJA also reduced the amount of mortgage interest that could be deducted by only allowing the interest on the first $750,000 of mortgage debt to be deducted, reduced from a limit of $1 million prior to TCJA.

“The potential repeal of the SALT cap will allow more taxpayers to itemize. However, SALT deductions could be reduced if Alternative Minimum Tax applies and there could be phase outs of itemized deductions for higher-income taxpayers.” – Martin James, CPA, PFS

The TCJA also eliminated personal exemptions, which is a deduction taken by the taxpayer, his or her spouse, and their dependents.14 In 2017, the personal exemption amount was $4,050. If the TCJA sunsets after 2025, we can expect a reduction in the standard deduction, removal of the SALT cap, and return of the personal exemptions.

Gift and Estate Tax

The TCJA effectively doubled the amount of the lifetime exemption of assets that passed on tax-free. That means the amount of lifetime gifts you can give while avoiding the gift tax is $13.61 million for the 2024 tax year and increases to $13.99 million for the 2025 tax year.15 Keep in mind that those totals are just for one donor, so you can effectively double them if you’re married.

We’ve been accustomed to the lifetime exemption going up each year. But if the TCJA sunsets after 2025, it would be reduced to about $7 million ($14 million for married couples). Families with assets that total several million or that are on track to leave behind significant wealth to their beneficiaries may want to consider estate planning techniques that have been out of fashion in recent years. Such strategies include using certain types of irrevocable trusts to avoid estate tax.

“If the current federal estate tax exemption sunsets, many more households will need to be engaged in estate tax reduction strategies that we have not needed to address in the past several years. Over the last several years, for all but the wealthiest families, estate planning has been based solely on the income tax attributes on assets passing to heirs. A sunset would change that.” – Martin James, CPA, PFS

Planning for These Potential Changes

These changes may have positive, negative, or mixed impacts on your personal financial plans. Fortunately, we can plan for potentially going back to old tax rates and the possibility of the TCJA sunsetting after 2025. It does, however, require some effort to run these projections in your personalized financial plan.

Our team of financial professionals at Modern Wealth includes CFP® Professionals that will build you a financial plan that’s tailored to your unique situation and goals. They’ll work with you to help understand how you want your life to unfold.

But there’s so much more forward-looking planning that needs to be done besides outlining your needs, wants, and wishes. This article is meant to shed light on how critical it is to have a forward-looking tax plan that is geared to help reduce taxation over your lifetime.

Working with a Team of Professionals to Understand the Impact of Reverting to Old Tax Rates

That’s why we have CPAs that work alongside our CFP® Professionals to review financial plans for potential tax planning opportunities. From Roth conversions to gifting strategies, our Tax Reduction Strategies guide includes examples of tax planning strategies that could result in substantial tax savings. We also have a Roth Conversion Case Studies white paper that reviews considerations for why someone should or shouldn’t do Roth conversions. Download your copies of those white papers below.

Tax Reduction Strategies Guide

We also have estate planning specialists on our team that work with our tax team and CFP® Professionals to help you understand the various complexities with estate planning. Given the impact that the sunsetting of the TCJA would have on future taxation and estate planning needs for our clients and prospective clients, these potential changes have had our team’s full attention.

“Overall, we are in a wait-and-see mode as the 2025 tax law proposals are being presented. Things are progressing quickly. Unlike prior years, we may know more sooner than later. Planning for the outcomes in 2025 and beyond is going to be critical.” – Martin James, CPA, PFS

If you want to learn more about how the potential sunsetting of the TCJA could impact you and your family, start a conversation with our team below.

Taxes are a source of financial stress for so many people and can be a large wealth-eroding factor for retirees. Planning for events like the potential sunsetting of the TCJA can go a long way toward alleviating that financial stress. We’re ready to build you a financial plan that includes a forward-looking tax plan so that you have confidence that you’re doing the right things with your money as you approach and go through retirement.

Resources Mentioned in This Article

- Tax Rates Sunset in 2026 and Why That Matters

- Financial Checkup Time: Review These Annual Items

- The 4-Year Presidential Election Cycle and the Stock Market

- 2025 Taxes: What to Watch

- 2025 Tax Brackets: IRS Makes Inflation Adjustments

- 2024 Tax Return Tips

- 2024 Tax Brackets: IRS Makes Inflation Adjustments

- What You Need to Know About Tax Deductions

- Estate Tax: How Will My Assets Be Taxed When I Die?

- Generational Wealth Management

- The Great Wealth Transfer Has Arrived

- 5 Estate Planning Documents That Everyone Needs

- A Successor Trustee Checklist with Matt Kasper, CFP®, AIF®

- 5 Types of Financial Plans

- Why You Need a Financial Planning Team with Jason Gordo

- Short-Term, Mid-Term, and Long-Term Financial Goals

- Setting Up a Spending Plan for Retirement

- Tax Planning Tips with Corey Hulstein, CPA and Martin James, CPA, PFS

- How Do I Pay Less Taxes?

- The CFP® Professional and CPA Relationship with Logan DeGraeve, CFP® and Corey Hulstein, CPA

- 5 Tax Planning Examples

- Roth Conversions Before and After Retirement

- 5 Reasons to Convert to a Roth IRA

- 5 Reasons Not to Convert to a Roth IRA

- Charitable Giving in Retirement

- Estate Planning Mistakes to Avoid with Tim Denker

- Financial Stress: How Do You Deal with It?

- 6 Wealth Destroying Factors

- IRA RMD Requirements

- Maximizing Social Security Benefits

- Avoiding Costly Mistakes When Claiming Social Security Benefits

- Tax Issues to Consider When My Spouse Dies

Downloads

Other Sources

[2] https://www.cbsnews.com/news/trump-tax-cuts-extension-republican-salt-deduction-student-loans/

[3] https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2025

[4] https://www.bankrate.com/taxes/2017-tax-brackets/

[5] https://taxfoundation.org/data/all/federal/2024-tax-brackets/

[6] https://taxfoundation.org/data/all/federal/2025-tax-brackets/

[7] https://taxfoundation.org/blog/2026-tax-brackets-tax-cuts-and-jobs-act-expires/

[8] https://youtu.be/JrE_Ur5b7Ag

[10] https://cbo.gov/publication/44088

[11] https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2025

[12] https://www.taxnotes.com/research/federal/reference-tables/standard-deduction/1x7yp

[13] https://taxfoundation.org/taxedu/glossary/salt-deduction/

[14] https://taxpolicycenter.org/briefing-book/what-are-personal-exemptions

[15] https://smartasset.com/taxes/all-about-the-estate-tax

Investment advisory services offered through Modern Wealth Management, Inc., a Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management a Registered Investment Advisor. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.