What Are Tax Brackets?

Key Points – What Are Tax Brackets?

- Comparing 2023 Tax Brackets to 2026 Tax Brackets

- Our Marginal Tax Rate System

- Looking at Tax Planning Strategies

- Inflation-Adjusted Tax Brackets

- 6 Minutes to Read

What You Need to Know About Tax Brackets

Is your NCAA tournament bracket already busted? Well, don’t worry. You’re not alone. Hopefully, your favorite team is still in it or has a bright future to look forward to. Even after basketball season ends, there will still be a lot of talk about brackets in our Barber Financial Group offices. Not about NCAA tournament brackets, but tax brackets.

You might think that the buzz surrounding tax brackets might fizzle out before too long as well since Tax Day is on April 18, but that’s not the case. The talk about tax brackets is going to continue to intensify, and we want you to understand why that is.

Tax Bracket Management

Our Director of Tax Corey Hulstein recently joined Dean Barber and Bud Kasper on America’s Wealth Management Show to discuss tax brackets, tax season, tax planning, and much more about what’s going on in the world of taxes. That show was titled, What Is Tax Planning? Corey, Dean, and Bud noted that another way to ask the question, what is tax planning, is to ask, what is tax bracket management?

“Let’s start with the basics. We work in a marginal tax system, which means that all your income isn’t taxed the same. Whether you’re married or single, the first bucket of money is taxed at 10%. As you scale up your income, it will start getting taxed at higher rates.”– Corey Hulstein

2023 Tax Brackets vs. 2026 Tax Brackets

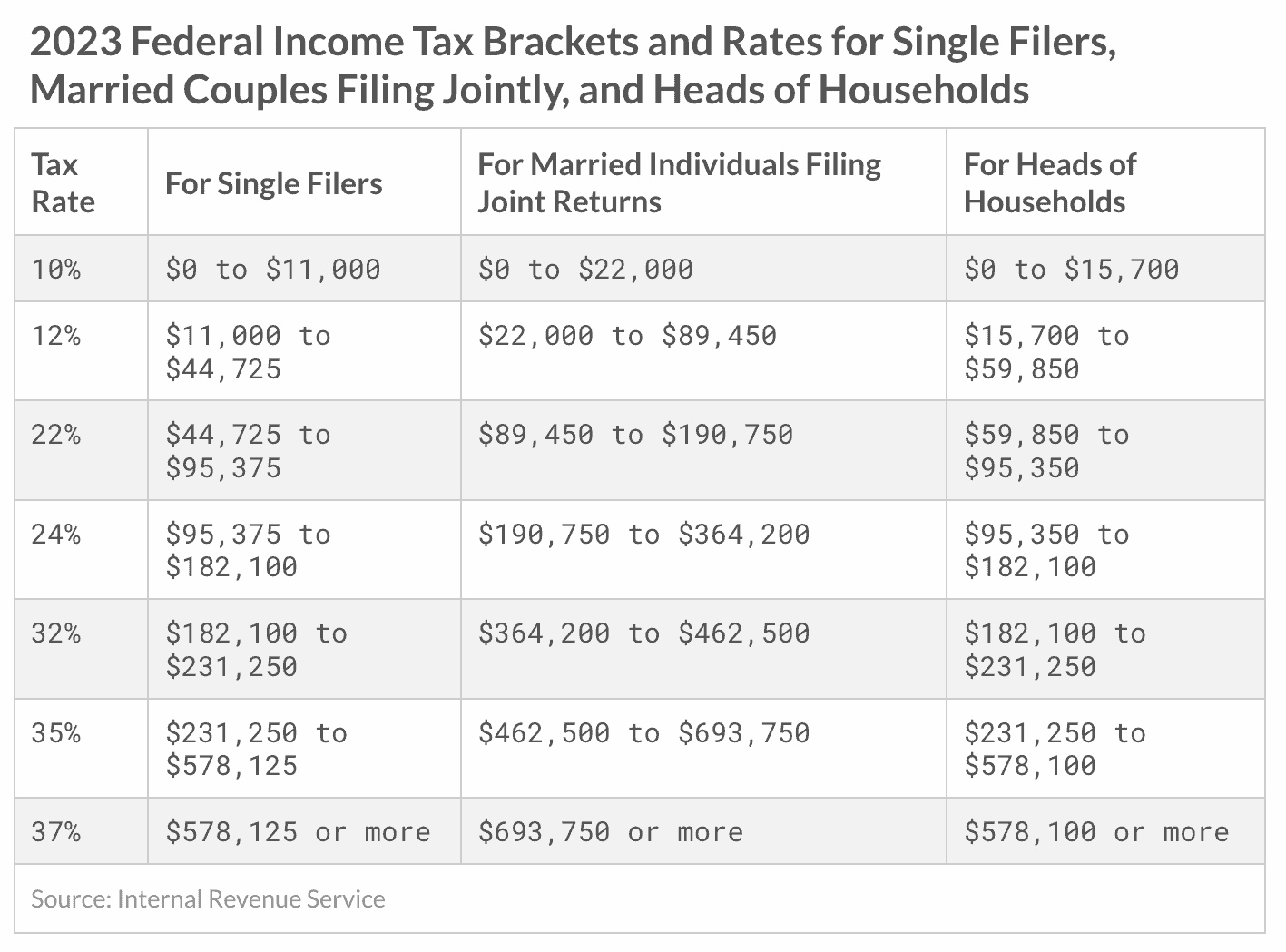

Now that Corey has given us the simple definition of tax brackets, let’s first look at the 2023 tax brackets for single filers, married filing jointly, and heads of households in Figure 1.

FIGURE 1 – 2023 Tax Brackets – Tax Foundation

“That first $10,000-$20,000 is always going to be taxed at 10%. The next chunk of money is taxed at 12%. Now, if you’re in the 12% bracket, that doesn’t mean that all your income will be taxed at 12%. As you scale up to the 22%, 24%, and 32% tax brackets, the marginal dollars that cross those thresholds are taxed at those rates.” – Corey Hulstein

We need to look at what tax bracket we’re in today versus what tax bracket we’ll be in in the future. That’s part of tax planning 101. Do you have years in the future where you know you’ll be taxed at a higher rate? These current tax rates are very low, so why not take advantage of them?

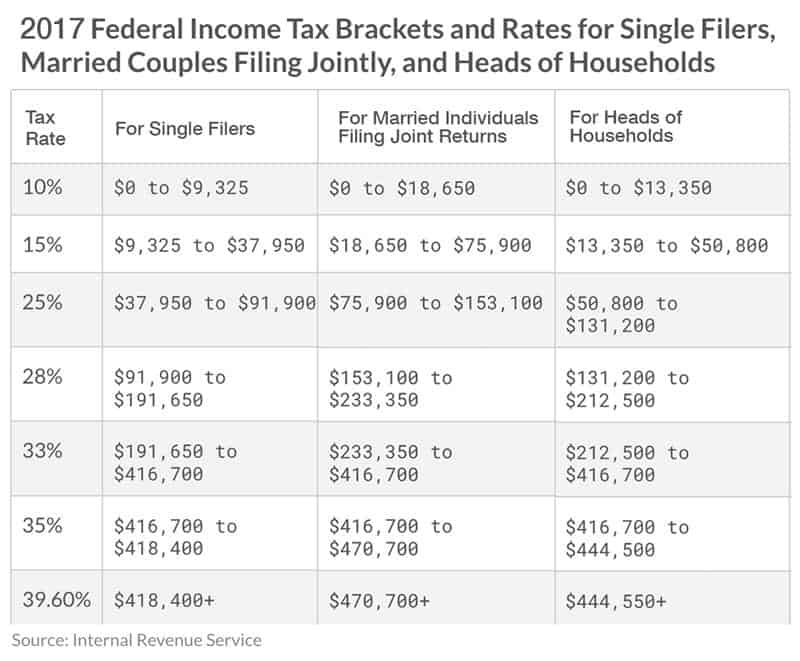

The current tax rates won’t be this low for long. That’s because the tax rates from the Tax Cuts and Jobs Act will be sunsetting in 2026. Unless something changes in Congress between now and 11:59 p.m. on December 31, 2025, the 2026 tax brackets will revert to the 2017 tax rates. You’ll see in Figure 2 that the tax rates go up and the tax brackets will be smaller.

FIGURE 2 – 2026 (2017) Tax Brackets – Tax Foundation

While the 10% rate won’t change in 2026, it probably jumped out to you that our current 12% rate will become a 15% rate. And that’s just the start. The 22% rate becomes 25% and the 24% rate becomes 28%. Those are substantial changes. The 32% rate becomes 33% and the 35% rate stays the same, so there won’t be quite as much of an impact if you reach those rates. Lastly, the 37% rate becomes 39.6%.

Tax Planning Strategies

So, does it make sense for you to pay more tax today knowing that rates are scheduled to go up in 2026? It depends on your financial situation, but in most cases, the answer is likely yes. That has been evident by the massive number of Roth conversions we’ve done in recent months. Those clients are paying tax up front, but the growth on their money and the distributions when they take it out of their accounts will be tax-free.

Tax-free is a beautiful thing that has become even more beautiful because of the strict rules on retirement accounts that are outlined in the SECURE Act and the SECURE Act 2.0. It’s what Dean is calling the Rothification of retirement accounts.

Paying tax up front with Roth IRAs and 401(k)s might not sound fun for this current tax year. But again, we’re not just looking at this year with tax planning. Keep thinking about 2026 and beyond. 2026 might seem like a long way off, but it will be here before we know it. The time to do tax bracket management (tax planning) is now. You don’t want to be blindsided by these drastic changes in 2026.

We can go on and on about other tax planning strategies. Some might work great for you and not as well for others and vice versa. That’s why you need to have a financial plan to help show you what will work best for you. After you’re done reading this article, we encourage you to review and download our Tax Reduction Strategies guide. We hope you’ll start seeing the bigger picture of minimizing taxation over your lifetime rather than just in one year. You can download our Tax Reduction Strategies guide below.

Download: Tax Reduction Strategies

Tax Brackets Adjust Due to Inflation

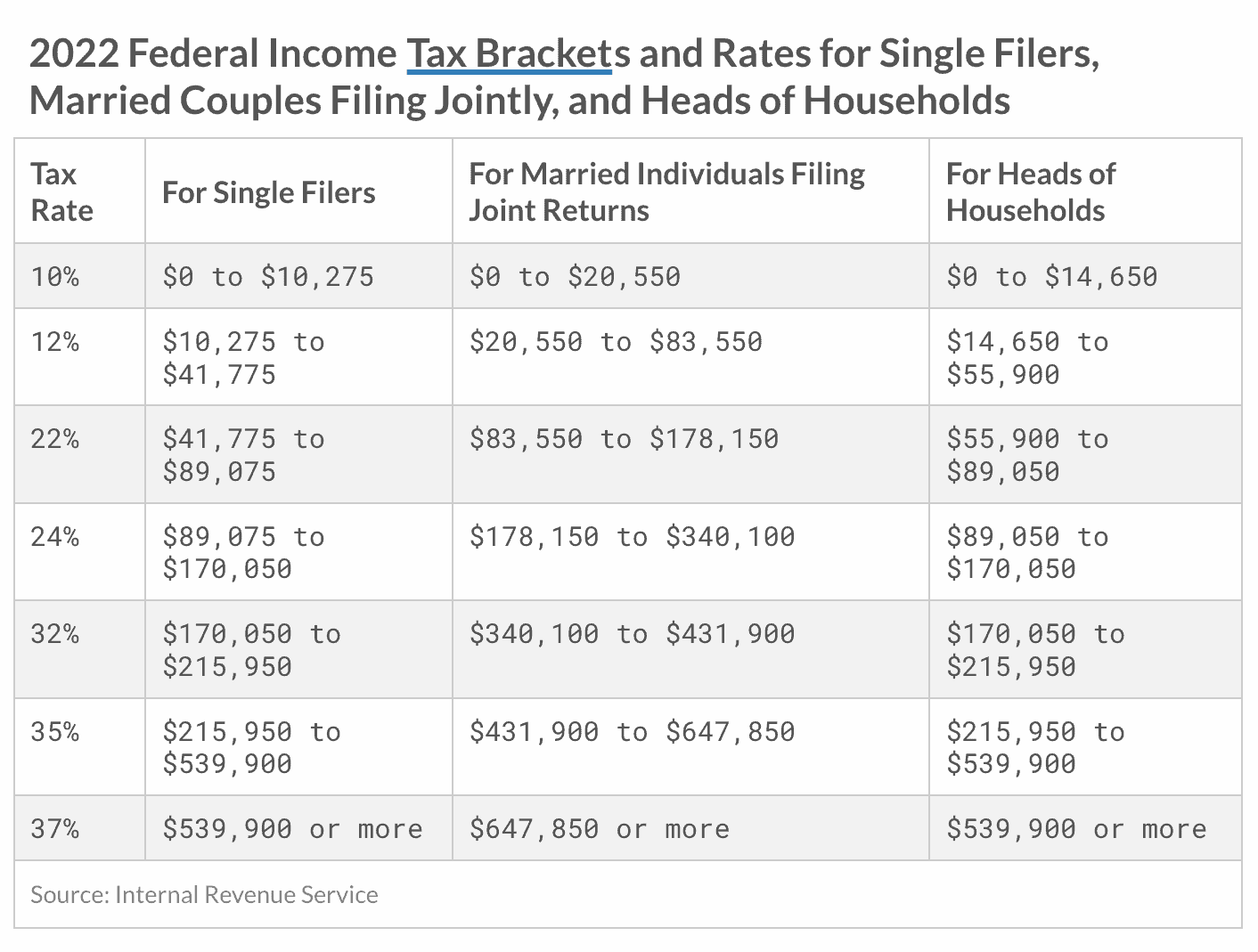

Along with looking ahead to 2026, it’s critical to remember that tax brackets will adjust annually based on inflation. The impact of inflation over the past year hasn’t been pleasant, but we did get some relief with the 2023 tax brackets. Before you keep reading, go back up really quick and look over the 2023 tax brackets in Figure 1.

Now, look at the 2022 tax brackets below in Figure 3.

FIGURE 3 – 2022 Tax Brackets – Tax Foundation

You can see that the tax brackets increased for 2023. Hopefully, you’ll realize that when filing your 2023 tax return next year. If you haven’t filed your 2022 tax return yet, you have a little less than a month left to do so before the April 18 deadline!

With the tax brackets increasing for 2023, that means that if you earned the same amount of income in 2022 and 2023, you’ll see a small decrease in taxation on your tax return. Again, this goes back to the marginal tax rate system that Corey described earlier.

Working with a CPA and CFP® Professional

There’s a lot of number crunching that can take place when determining what tax bracket(s) you’ll be in going forward. The bottom line is that it’s pivotal to have a financial plan in place to truly understand the impact of tax planning. In fact, that leads us into a bit of a preview of our next Modern Wealth Management Educational Series event with Corey. It’s titled, Tax Planning for Individuals: 5 Tips to Save.

We won’t give too much of it away, but Corey’s first tip happens to be getting a financial plan done with a CFP® Professional. When we’re building someone’s plan, we’re not just looking at their investments. We’re looking at things like what tax bracket you’re in now versus what tax bracket(s) you’ll be in later on. What tax planning strategies can you use so that you’re paying the least amount of tax possible, not just in one year, but over your lifetime?

Tax Planning Plays a Big Role within Financial Planning

That’s a big reason why when we’re building someone’s plan, it’s not just a CFP® Professional that’s doing it. We’ll have a CPA that reviews your plan from a tax perspective. Our CFP® Professionals will also consult estate planning attorneys, Medicare experts, and other insurance experts to make the necessary adjustments throughout the life of your plan.

If you want to see how all these components of financial planning work together for you, check out our financial planning tool. As you’re building your plan, you can really start to see how tax planning is important, especially between now and 2026. That’s why we’ve been trying to get the word out about the differences between today’s tax brackets and tax brackets in 2026, and why you need a financial plan to give you clarity and confidence moving forward.

To begin building your plan with our financial planning tool, simply click the “Start Planning” button below. You can use it from the comfort of your own home and at no cost or obligation.

Do You Have Questions About Tax Brackets?

Trying to understand all this on your own can be overwhelming. We certainly don’t want that because making emotional decisions with financial planning can oftentimes make matters work. We’re here to help you so that doesn’t happen. If you have questions about the tax brackets, tax planning, or other components of financial planning, let us know.

You can ask us those questions by scheduling a 20-minute “ask anything” session or complimentary consultation with one of our CFP® Professionals. The setting of the meeting is completely up to you. We can meet with you in person, by phone, or virtually. We hope this information about tax brackets has been enlightening for you and welcome the opportunity to discuss them more with you going forward.

Investment advisory services offered through Modern Wealth Management, LLC, an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management, LLC, an SEC Registered Investment Adviser. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management, LLC does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.