Retiring at Market Highs

Key Points – Retiring at Market Highs

- Recent History of 60/40 Portfolios and Withdrawal Rates

- Measuring Inflation, Bonds, and Equities

- Average Annual Returns for Rolling Periods Dating Back to 1972

- The Importance of Dynamic Financial Planning

- The Keys to Retiring at Market Highs

- 15 minute read | 27 minutes to watch

Dean Barber and Jason Newcomer look at how retiring at market highs has been impacted by the recent history of 60/40 portfolios and withdrawal rates. They analyze every rolling 20-year period since 1972 to see how annually increasing withdrawal rates—while accounting for inflation—accommodated for a constant standard of living.

Get a Complimentary Consultation Subscribe on YouTube

Recent History of 60/40 Portfolios and Withdrawal Rates

Dean Barber: Stock market valuations near all-time highs, the threat of inflation, and super low interest rates … What does that have to do with your retirement? Jason Newcomer, CERTIFIED FINANCIAL PLANNER™ and director of financial planning at Modern Wealth Management, and I will measure inflation and what bonds and equities did in every rolling 20-year period since 1972.

Jason, we have some exciting information to share today. You and your team did a lot of research for one major purpose—that was to run through all the 20-year rolling periods, going all the way back to 1972. We are looking at two things: a 60/40 portfolio and a withdrawal rate starting at 5%. Then, we look at increasing that withdrawal rate every year with whatever the inflation rate was for that year so that people can have a standard of living that remains constant.

Market Valuations, Potential Inflation, and Ultra-Low Interest Rates

We’re doing this because a couple of phenomena that are happening today. Number one, we’ve got market valuations. Not the number on the market, but valuations in the market that are higher than we’ve seen since just before the Dot-Com Bubble. We also have a lot of talk about potential inflation and ultra-low interest rates.

So, we’ve got some dynamics at play that are different than what people have experienced over the last 20, 30, maybe even 40 years. We need to talk about it because there’s a lot of people that are entering into retirement right now. I want to make sure that they understand what expectations should be set forth for them with retiring at market highs.

Retiring at Market Highs Is a Good Thing

Jason Newcomer: People get nervous, right or wrong, anytime they hear the headline, “The Market Has Made a New All-Time High Today.” It sends up little alarm bells. When you think about that, that’s a good thing, right? Markets are at all-time highs. We like to see new all-time highs get made. I think we’ve seen more than 50 just this calendar year.

Dean Barber: Right. Retiring at market highs is not necessarily a bad thing. When you look at the backdrop of economic activity that’s happening right now, the market could maintain its elevated status for quite some time. In fact, markets can be overvalued for a longer period, especially when you have strong economic growth as a background.

Jason Newcomer: True. But tell that to someone who is getting ready to retire, give up their paycheck, and start drawing down their investment assets. Now you’ve got some nerves that enter in.

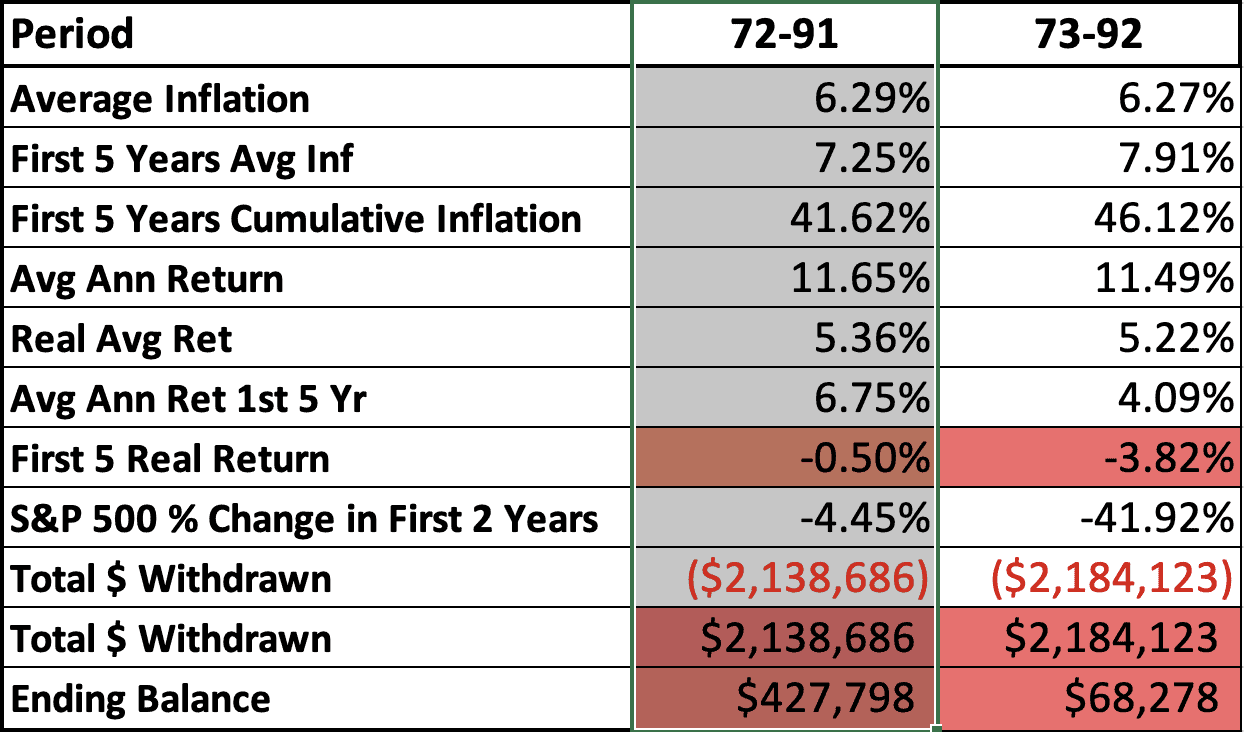

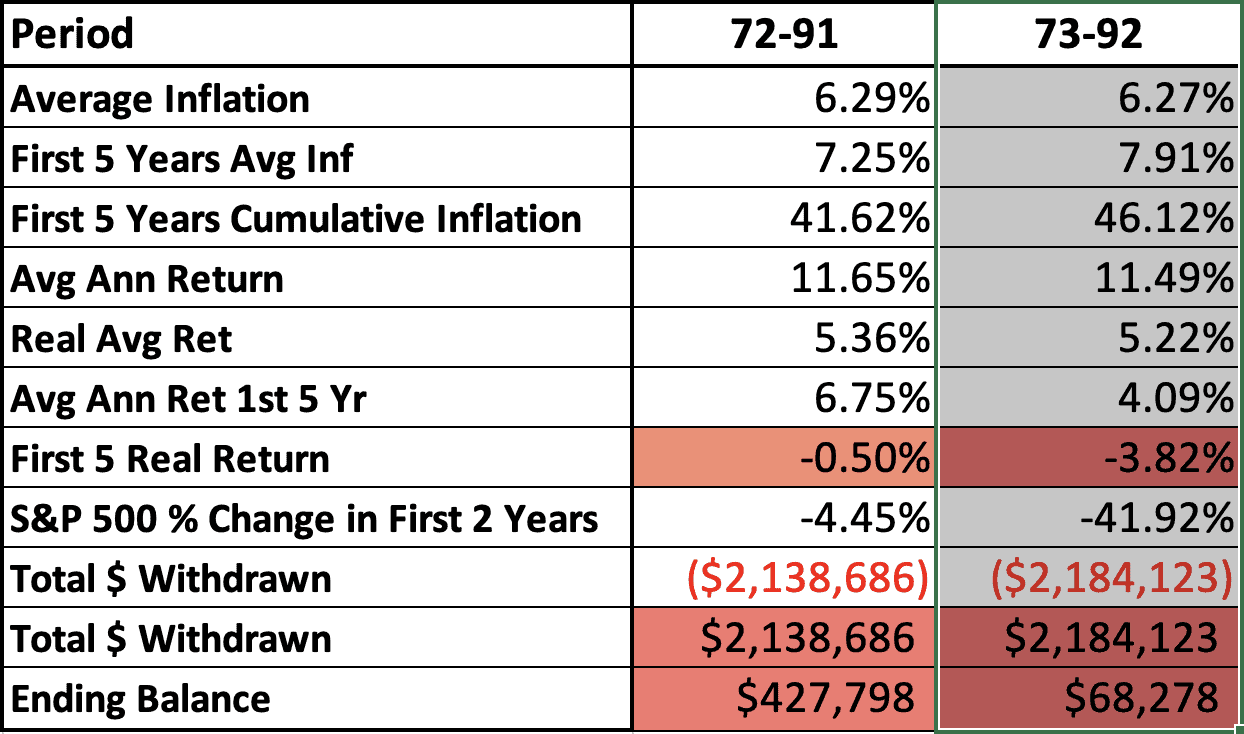

Average Annual Returns from 1972-1991

TABLE 1 – 1972-1991

Dean Barber: Let’s start by looking at TABLE 1 that you put together. It’s very busy, so I’m going to draw our attention to a couple of different things. Let’s begin with this period from 1972 to 1991. What I want to look at first is the average annual return on this 60/40 model from 1972 to 1991 at 11.65%.

If we stopped and set a 60/40 portfolio starting in 1972, going through 1991, and averaged 11.65%, I can take 5% that first year and then increase my income each year to keep up with inflation. You would think that that 11.65% would be ample to allow me to take the income I need. I wouldn’t even have to worry about running out of money.

Jason Newcomer: On its face, it sounds like a no-brainer and that I should be totally fine with that.

Sequence of Returns and Inflation Rates

TABLE 1 – 1972-1991

Dean Barber: Correct. There are two other factors that people must look at when retiring at market highs. Number one is the sequence of returns. In other words, what were the returns in the early years, and what were the returns in the later years?

The other one is, what was the inflation rate during that period? If we look at this, we had average inflation over that 20-year period of 6.29%. We haven’t seen that in our lifetimes. People have been experiencing 2% to 3% type inflation rates. But does that mean that we can’t go back and see those higher inflationary periods?

Then, we had a scenario where the first five-year real return was -0.5%, so explain the real return.

Nominal Returns

Jason Newcomer: Everyone’s familiar with something called nominal return. You might not be familiar with the term nominal return, but all we’re talking about is what the rate of return is that you earned on your portfolio.

You look at your statement, log into your account, and have made 10%. That’s your return in nominal terms. On paper I made 10%, but the real return is where you subtract out inflation. If inflation is 6% and I made 10% on my real return, I’m only 4% better when I factor in inflation.

Dean Barber: OK, so let’s go through this. If we started with $50,000 a year, that being 5%, continued taking that withdrawal, and kept up with inflation, we would have withdrawn $2.138 million over a 20-year period. We’ve got an ending balance of only $427,000.

Jason Newcomer: So, we barely made it by the skin of our teeth over that 20-year period.

TABLE 2 – 1973-1992

Dean Barber: We barely made it. And when you look at the next 20-year period from 1973 to 1982, you had a 6.27% average inflation and 11.49% average annual return. Those two, You would think that those two at face value should come out fairly even, but look what happened. By the end of 20 years, your account balance was down to just $68,000.

The First Five-Year Real Returns

Jason Newcomer: The number that I’d really draw attention to is the first five-year real return.

Dean Barber: Negative 3.82% was your real return for the first five years.

Jason Newcomer: That’s really what killed this scenario. After 20 years, you’ve run out of money in your portfolio.

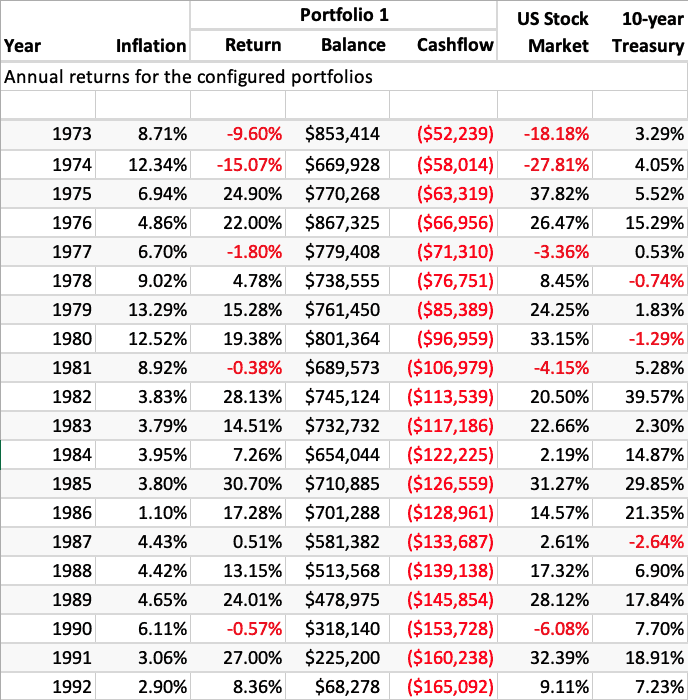

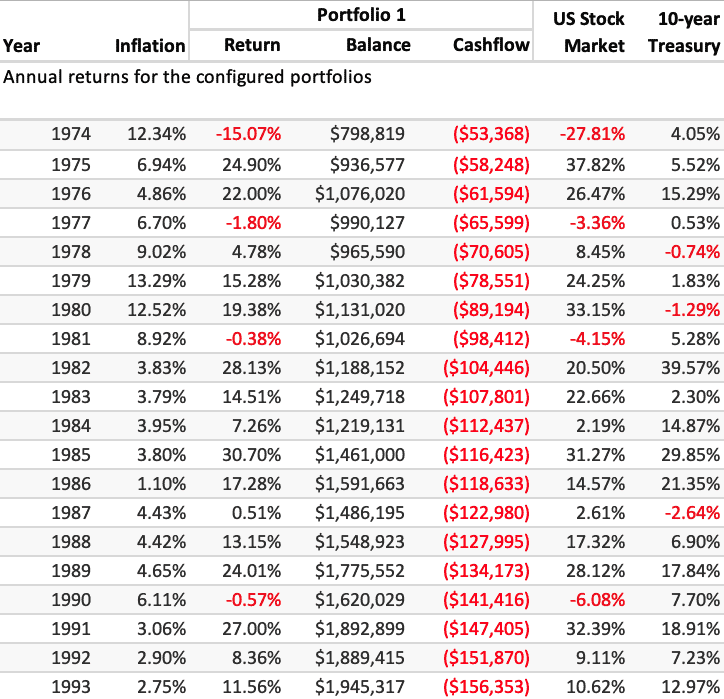

TABLE 3 – Annual Returns from 1973-1993

Dean Barber: Let’s dive into those years a little bit deeper and examine what the markets did during that period. In 1973, we had inflation of 8.71%, the stock market lost 18%, and the 10-year treasury made 3.29%. So, your portfolio lost 9.6%.

The following year, the market went down 27.8% and 10-year treasuries made 4%. That means you lost 15% but look at inflation in 1974 at 12.34%.

Jason Newcomer: It is just compounding the bad scenario there.

Dean Barber: Right. Here’s one thing that I think is fascinating. To keep up with inflation, we needed $106,000, almost $107,000 in 1981 to buy the same thing that $50,000 bought just eight years earlier.

Jason Newcomer: We’ve more than doubled our withdrawal to maintain our same standard of living.

Dean Barber: So, here’s what happens. We got a market value of $689,000 and need to take $107,000 out. Well, we’re not at a 5% withdrawal anymore.

You and I both know that if this scenario played out for somebody, they would not allow this to happen. They would stop spending. They would cut back on all kinds of things and reduce their standard of living before taking out $107,000 on a portfolio that’s only worth $689,000, especially just eight years into retirement.

Jason Newcomer: You probably even need to consider going back to work.

The Monte Carlo Simulation

Dean Barber: Very possibly. This is an important part where we want to talk about how we look this because these types of scenarios can play out in the future. By using something called Monte Carlo simulation in our planning programs, we are stress testing portfolios through these types of conditions to make sure they can work.

We do an historical audit as well as a Monte Carlo simulation. We can take a portfolio that somebody has today and say, “Let’s run that portfolio back through this inflationary period of the ’70s and see how it would’ve worked.” Then, we get some clarity and can say, “What would’ve worked back then? If this coming, we need to adjust portfolios to fight this off as best we can.”

Jason Newcomer: Yeah. It’s adjusting portfolios, the allocation, and even the distribution strategy. How much are we going to be pulling out in a good market? Maybe it’s a higher percentage that we can pull out. When we’re typically discussing retirements, we’re talking about spending the most money in the first five to 10 years of retirement.

Dean Barber: It depends on how young you are when you retire. If you retire at 60, you might have a good 15 years of solid spending. And if your health is good, that may continue for 20 years.

You Can Only Spend Actual Returns

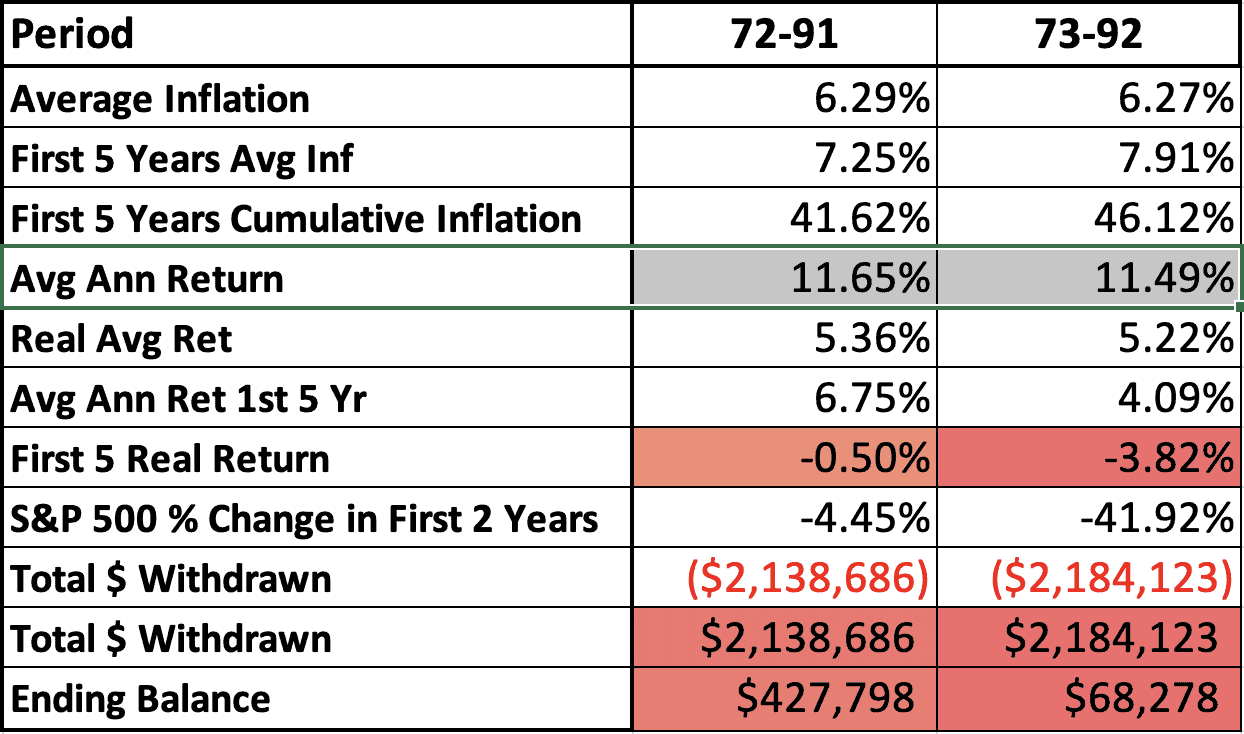

Dean Barber: Let’s go back for just a minute, because I want to point out something I’ve said many times on my radio program, podcasts, and videos. You can’t spend average annual returns. You can only spend actual returns.

TABLE 4 – Average Returns from 1972-1992 and 1973-1992

This is a perfect example where we have two scenarios where we’ve got average annual returns above 11%. Yet in both cases, we come close to running out of money.

TABLE 5 – Annual Returns from 1974-1993

Here’s what I find fascinating. If we take this one year forward and retired in 1974 instead of 1973, we still had those high inflationary periods but didn’t start with the two horrible years in the market. We just had one bad year in the market, and then that was followed up by two good years.

And look at what treasuries did. They were 15.29% in 1976. We wound up with a 22% return and a 24.9% return. The bottom line is that you still needed to keep up with inflation, but in this scenario, you wind up with almost $2 million. You keep the same standard of living as somebody that retired a year before you.

Jason Newcomer: We’ve talked about this before. With sequence of return risk, it’s the risk of you retiring at the wrong time and things are out of your control. It’s not necessarily just the sharp decline in the market followed by a recovery—the typical run of the mill bear market—that puts your retirement long term in jeopardy. It’s the prolonged period of the compounding storm of high inflation, poor returns at the beginning, and poor real returns over a five-to 10-year period in retirement.

Maintaining the 60/40 Average

Dean Barber: This is fascinating. Here’s one of the things I think is critical for us to point out. What you’ve done here is a 60/40 portfolio, and you’re assuming a systematic withdrawal. We’re selling a portion of the stocks and a portion of the bonds each month, and we’re rebalancing at the end of each year. We’re maintaining that 60/40 average.

If you took and invested $1 million and you didn’t have any withdrawals, it doesn’t matter what the sequence of return is. You’re going to wind up with the same amount regardless of whether you had the good returns at the beginning or the end if it averages 11.7% or 11.4%.

One thing we like to do, especially if somebody’s heading into retirement with valuations where they are today, is step back and say, “What are we going to need to live on for the first three or four years out of the portfolio?” Maybe even the first two years, for sure.

Let’s set that aside in something that can’t lose money and spend that. That way if these things occur, we can allow the markets to reset and gain our composure. If we have a good year, we can take those winnings and put them into a very safe account. That can prevent something like what we saw happening from 1973 to 1992 from happening.

Jason Newcomer: That’s right. In a scenario like that where you’ve set aside maybe two, three years of cash reserves or something liquid that’s not tied to the performance of the market, you’re not having to sell those stocks that are down 30%, 40%, 50% in a bear market.

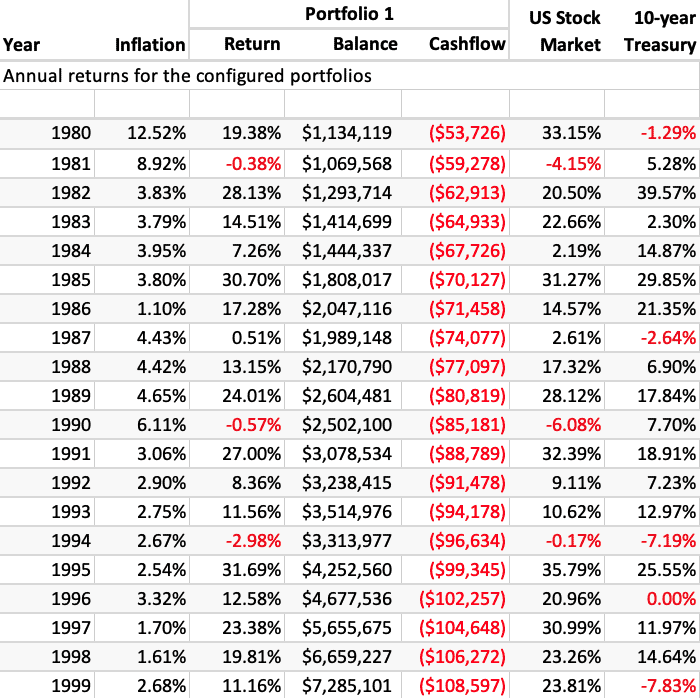

Average Annual Returns from 1980-1999

TABLE 6 – Annual Returns from 1974-1993

Dean Barber: Exactly. I want to fast forward. We’re going to look at 1980 to 1999, so a totally different timeframe. We are still going to start by taking the $50,000, and then increase it to keep up with inflation. However, we didn’t need to double our income until 1995. We went a full 15 years as opposed to eight years before we needed to double our income.

We kept our standard of living the same for that 20-year period with $7.28 million. That’s a far cry from the person that retired in 1973, yet we did the exact same strategy. Here’s what I think happens to a lot of people. I call it recency bias.

Leading Up to the Bursting of the Dot-Com Bubble

In 1999, we were right in the middle of the tech bubble. We had Alan Greenspan talking about irrational exuberance. You’re too young and weren’t in the business at that time, but I remember it well. In 1999, people in our industry were saying, “You know what? That 5% to 6% withdrawal rule that you did, that’s dead. You can withdraw 8% and it’s going to be safe.”

The last time that we saw valuations as high as they are today was at the peak of the market in 1999. That was just before Dot-Com Bubble burst. What I want to do is fast forward and look at what happened in the last 20 years. People are probably saying, “If I do a 60/40 portfolio, why couldn’t I take 8%? I can take that and I’m still going to have a heck of a lot of money left over. And guess what? I’m going to have a better retirement life.”

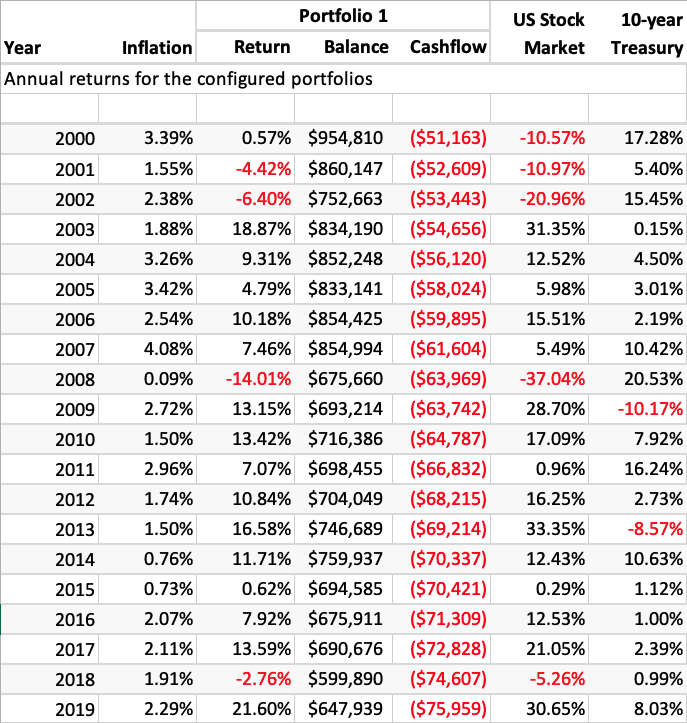

Average Annual Returns from 2000-2019

TABLE 7 – Annual Returns from 2000-2019

Now let’s say somebody retires in January 2000. You get a -10%, -11%, and -21% in the stock market, but look at what treasuries did here in 2000. They earn 17.25%, 5.4 %, and 15.45%, respectively.

Before we get too deep into what’s going on here, I have a question for you as a CERTIFIED FINANCIAL PLANNER™ who understands how bonds react in different interest rate environments. What do you think the possibility is in the next market downturn for treasuries to give that kind of a boost to a portfolio, if that were to occur in the next couple of years?

Jason Newcomer: It’d be tough. Interest rates are totally different than they were 20, 21 years ago. In 2000, we had treasuries significantly higher than where they’re at today.

Interest Rates Fall, Bond Values Rise

Dean Barber: Back then, you could even go buy a 5.5% or 6% CD, so your 10-year treasuries are doing better. So, what happened during the recession? The Dot-Com Bubble. Interest rates fell. As interest rates fall, bond values rise. We can’t have that phenomenon when we’ve got a 10-year treasury yield hovering around 1.3%. We can’t expect to be the case. But again, we just took out 5% and continued that.

All we had to do was get the $75,959 of income to get same standard of living that we had at $50,000 in 2000. We didn’t have to take out near as much money out of our portfolio, but look what happens. We’re down to $647,000 at the end of 2019, taking a $75,000, almost $76,000 withdrawal. We’re well above that 5%.

Jason Newcomer: We’re north at 10%. If you just run the quick back-of-the-envelope math, this portfolio with that level of spending is probably not going to last much longer.

Dean Barber: Yeah. Maybe seven, eight years. When people are thinking about retiring at market highs, it’s scary. What do you do? How do you position yourself? The only answer is a comprehensive financial plan using our Guided Retirement System™.

Dynamic Planning Is Paramount

Jason Newcomer: Planning must be a part of it when retiring at market highs. You can’t just set it and forget it. Remember the scenario where we had $65,000 left in the balance of the account after 20 years. That plan has failed and was bad to begin with. Alternatively, you could look at one of these scenarios where you’ve left behind $7 million.

Dean Barber: That was a bad plan too.

Jason Newcomer: Exactly right. We weren’t making adjustments and saying, “Hey, we’ve had better than expected market growth. Your balance in your account after the first few years of retirement is significantly better than what we thought it would’ve been.”

Dean Barber: Let’s adjust your lifestyle and spending. Give money away, do charitable things, help your kids, or do something to fund college for your grandkids. If those things weren’t already in the retirement plan, you can start to add those things in.

Jason Newcomer: That’s right. Planning needs to be dynamic; it must be done constantly. That’s part of the financial planning process is to monitor the plan and adjust it as time goes on.

Strong Financials and Deep Value Stocks

Dean Barber: What you’ve modeled here is two things: U.S. total stock market and the 10-year treasury. In 2000, 2001 and 2002, the technology portion of the S&P 500 reached about 37%. That means if you looked at the S&P 500 and the total valuation of the stock within the S&P 500, the technology component of that was 37%. That’s very large.

What did well in 2000, 2001, and 2002 were financials and deep value stocks. In fact, those stocks made money in 2000 and 2001. They might have lost a little bit in 2002, but by and large, those sectors did extremely well, even amid the Dot-Com Bubble. That means that most of the time, you can look for opportunities of market sectors that are less overvalued or potentially undervalued as compared to the entire market.

Jason Newcomer: Factor investing or active management might come into play in a scenario like that where you’re not looking to own the entire market, but be selective with where you’re investing.

Dean Barber: Right. You don’t just go in and say, “I’m going to get completely out of this sector and go over here.” It tells you where you should potentially be overweight, and where you could be underweighted. That is the key. It’s dynamic. It’s not a set-it-and-forget-it type of a scenario.

The Fallout of Too Much Exposure to Hot, Overvalued Sectors

Now the old saying is, “A rising tide lifts all boats.” That’s true. Then, there’s another one of my favorite sayings from Warren Buffett. He said, “It’s not until the tide goes out that you see who is swimming naked.” If you have too much exposure to the sectors that may have been the hottest or the most overvalued, you can get smacked hard when those things lose money.

Jason Newcomer: That goes into your strategy of, how are you getting money out of the investment account and into your checking account to be spent? Be selective—not just maybe selling investments pro rata across the board—but rebalance the account strategically to sell the things that maybe have made money in periods where there’s investments in your account that have lost money. Maybe you’re not touching those.

Dean Barber: Especially if it’s a sector that you have a lot of conviction in that you know and we’re in a temporary lull. You can hold onto those things, but you must have the plan set up. Toward the end of each year, people should sit down and say, “This is how much we need to spend next year based on our plan. Where’s that money going to come from? Should we raise some capital from some winnings this year?”

When you look at just what’s happening in 2021, we’ve had to do rebalancing multiple times this year because the equity markets have gotten out of whack. If you had a 60/40 portfolio and the equity markets are up 20% and bonds are flat, you’re going to have to rebalance if you want to maintain that 60/40 discipline.

Jason Newcomer: We’ve written extensively about rebalancing portfolios.

Stress Testing Plans in All Sectors

Dean Barber: If we could take one thing away from this, it’s that we can’t go back and just look at history. If I looked at this history and said, “This is my last 20 years and that is my reality.” That’s not reality. We need to look back and say, “When were valuations high? What did you do? When was inflation high? What did you do?”

We must stress test people’s plans through all those scenarios to come up with the proper allocation today. That might be different six months or a year from now, but what is it today that gives us the highest probability of success with the least possible amount of risk?

Jason Newcomer: If someone had come up to you or I and said that they’re thinking about retirement, but are just not sure that it’s a good time to retire right now with what’s going on in the stock market, what kind of response might you give them?

It’s Not All About the Stock Market

Dean Barber: Retiring at market highs is a legitimate concern, but people need to think about life and not just the stock market. There’s nothing out there that can’t be navigated with proper planning and attention. It may not be smooth sailing, but we can set up strategies that will allow us, for example, to carve out our first three years of income.

Let’s take that first three years of income and set it aside into something that’s safe. We know that we don’t have to sell anything if the markets take a decline in the next three years. If we happen to get another good year or six months, we can take those winnings and dump it back over into that safe bucket.

It’s important that we’ve always got the confidence to know we’ve got the money to spend, and we’re not hampering the ability to keep a longer-term perspective from our investment strategy.

Taking Pressure off the Portfolio

The other thing that I would say is that proper financial planning techniques can take a lot of pressure off the portfolio. Those techniques include proactive, forward-looking tax planning, Social Security maximization strategies, or dynamic gain harvesting.

There are different ways during different periods that people need to be thinking about things, but it all ties back into what you do in our Integrated Financial Planning Department, which is creating that robust financial plan that’s not just looking at the investment. In fact, you don’t even look at the investments until after your financial plan is completed.

It’s All About the Planning When Retiring at Market Highs

Jason Newcomer: That’s right. I love that answer to this hypothetical question. I understand you’re concerned about markets, but go with this portfolio and you won’t need to worry about anything because it leads with planning. It’s all about the planning when retiring at market highs.

Dean Barber: The worst thing that a person could do in today’s environment is buying one of those target date funds or a simple balanced fund. If that fund is a balanced fund and it has a discipline that says that we are going to maintain a 60/40 mix, that means they’re going to maintain a 60/40 mix.

They’re not going to raise cash. You’re going to be forced to sell into down markets. It is one of those things where that can become a self-fulfilling prophecy of you running out of money. You need to have far more control than just a balanced fund or a target date fund.

Jason Newcomer: Retirement planning and financial planning is so much more than what’s in your portfolio. It takes into consideration all those other things—Social Security, tax strategies, pension election options. All these things come into play that are far more important.

Dean Barber: They do. I hope that this has been beneficial and served as an eye opener. Anybody out there that’s thinking about retiring in the next five to 10 years, or even if you’re already retired, get a conversation started with one of our CERTIFIED FINANCIAL PLANNER™ Professionals. They can welcome you through our whole process, engage you in our Integrated Financial Planning Department, and put together a plan that can provide the clarity that somebody needs to have confidence.

Jason Newcomer: It starts and ends with the plan in mind.

Clarity Equals Confidence; Confusion Equals Chaos

Dean Barber: There’s a good saying out there, “Clarity equals confidence; confusion equals chaos.” If you’re confused about what you should be doing, we can help you get the clarity. That’s the key. And it changes over time.

Jason Newcomer: It’s dynamic. Retiring at market highs was a fun case study to look at.

Dean Barber: Absolutely.

Schedule Complimentary Consultation

Click below to get started. We can meet in-person, by virtual meeting, or by phone. Then it’s just two simple steps to schedule a time for your Complimentary Consultation.

Investment advisory services offered through Modern Wealth Management, LLC, an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Adviser. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.