Understanding US Inflation

Key Points – Understanding US Inflation

- What Is Fueling US Inflation?

- Inflation As It Relates to Retirees

- Accounting for Inflation within the Guided Retirement System

- Reviewing the Financial Triple Threat

- 18 minutes to read | 38 minutes to listen

From prices at the grocery store to the cost of filling up your gas tank, we have all seen the impacts of inflation in recent months. Dean Barber and Bud Kasper give their thoughts on the current inflationary pressures and what US inflation could look like going forward.

What Is Fueling US Inflation?

Dean Barber: Thanks so much to those who join us on America’s Wealth Management Show. I’m your host, Dean Barber, along with Bud Kasper. If you look at any of the current financial headlines, the one word that’s out there that’s prevalent is inflation. We know that US inflation is real.

When you go to the gas pump and grocery store, you can see it’s real. The question becomes, what is fueling US inflation? Is it this super wild demand that’s out there right now? Is it a supply chain scenario? Or is it perhaps the easy monetary policy? Or could there be a combination of those three?

Once we figure out what it is, then the question becomes how long will this phenomenon last? Do we think that the 7% year over year inflation that we’ve seen happening is due to repeat itself in 2022 and 2023? Do people need to prepare for skyrocketing costs to continue?

Bud Kasper: I think it’s a combination of the three, but I point my finger at the Federal Reserve as well. They’ve been slow to the mark in raising rates earlier. I thought we would have an increase at least by December and we still don’t have one. I hate it when the Federal Reserve feels the pressure of having to go in and catch up.

US Inflation and Supply Chain Issues Go Hand in Hand

However, I think Dean’s supply chain comment has the most merit. It’s hard to manufacture whatever you’re building if you don’t have all the parts to build it. Obviously, that slows things down. It puts the current inventory in demand as that starts to wane down and you don’t have supply coming back into those particular things that you’re buying. That’s when you’re going to have a dislocation in the economy.

Dean Barber: If you want to truly understand these US inflationary pressures, read the latest article from Shane Barber titled, Inflation and Supply Chain Issues Are Intertwined. That article has a wealth of knowledge and great perspective from Shane, but I bet you might have a lot of questions about inflation after reading it.

US Inflation’s Impact on Housing

As we discuss US inflation, I specifically want to address two separate issues: housing and automobiles. I think housing is inflating based on two different factors. One factor we’ve talked about this for a long time, and that is that the millennial generation is starting to have babies en masse, As they’re having babies, they don’t want to raise them in apartments. They left home, went to college, and then rented these nice apartments as if it was the house that they were living in when they grew up. Those apartment communities might have even had amenities. Now, they’re buying houses like crazy.

COVID-19 has also played a part in this. If people were going to have to work from home or do something like that, the last place they wanted to be was in an apartment.

One catalyst that really allowed the prices to escalate was the zero-interest rate policy. Mortgage rates that were so cheap that people could afford to spend a lot more money on a home than what they would just a couple of years prior because interest rates were so much higher.

Bud Kasper: We’ve seen this before. I remember when valuations on real estate were going through the roof. People were buying into it. There were clients that were taking money out of their IRA and putting it into houses that they were buying in Arizona. That collapsed as well.

There’s No Quick Answer to Resolve US Inflation

The issues at hand are unfortunately not going to be solved overnight. That’s why I’m a little disappointed in the Federal Reserve. I think we could have met this head on a little sooner and could have made a lot of this tamer than what I’m expecting to see.

You’re seeing US inflation’s impact right now in the marketplace because bonds are suffering and stocks are suffering along with them. I still think it’s going to be a positive return for the market before the end of the year, but it could be uncomfortable in the shorter term.

Dean Barber: There’s no question about that. I talked about this in our latest Monthly Economic Update as well and to expect more volatility. The rising interest rates are coming. But if you want to look at the positive side of the market, you’ve got some very good corporate earnings that I believe are going to be coming out in the next several weeks. Those positive earnings are going to continue and if the supply chain issues are fixed, we should start to see these inflationary pressures soften a little bit. I don’t think there’s a world where Bud and I could agree that we would see another 7% year over year increase. I think we’ll see more in the lines of 3% to 4%, something like that for 2022.

Looking at these most recent US inflationary numbers, the fear is that the Fed overreacts and tightens too fast. When that happens, you get risk recessionary pressures. If you get recessionary pressures because the Fed tightens too fast, that’s where your bear markets can come in. That’s what people really need to be on the lookout for.

US Inflation As It Relates to Retirees

Of course, one of the groups that inflation hits the hardest is the retired community. They’re not going to have the wage increases that working individuals can have. Even if you get a decent increase in Social Security, it is oftentimes minimized by an increase in Medicare premiums.

Retirees need to think about things that are costing more, such as going to the grocery store, getting gasoline, and getting adequate heating and cooling for your home. If people haven’t planned properly for the possibility of higher inflation, they could find themselves living less than optimal lives.

Bud Kasper: Possibly. I was thinking about the impact of inflation just last week because the refrigerator in our Lee’s Summit office went out. My wife, Peggy, and I went over to Best Buy to see if we could find something there. However, the large-sized refrigerators couldn’t be delivered until March 30.

We ended up buying one on the floor that was a modest refrigerator, which thankfully was all we needed. But it still made me think about falling victim to the ongoing supply chain issues. You can manifest that in different categories.

Dean mentioned that the millennials are looking for homes. When I drive around Lee’s Summit, where my wife and I and our family lives, we see duplex construction that is going on around the city. They’re homes to a lesser extent, but getting all the lumber and everything else to build them is nearly impossible right now and therefore it’s slowing the process.

How the Hefty Home Prices Impacted One of Our Clients

Dean Barber: Yeah. It’s interesting. A client of mine sold his place in Leawood, moved to Arizona, and planned to build a home there. Once he got there and started looking at where he was wanting to build, he realized that it was about 50% more expensive to build a home in that market. It was the same case in Dallas, which was the other area he was looking to build in. It’s unbelievable. It’s a factor of where you are and how much those prices have increased, but there’s no question about it that this is impacting people.

Accounting for Inflation within the Guided Retirement System

When Bud, myself, and all our CERTIFIED FINANCIAL PLANNER™ professionals create a financial plan for somebody using our Guided Retirement System, one of the things that we’re cognizant of what US inflation is going to do. We can play around with that inflation number, but we’ll generally start out somewhere around 4% baseline as our average inflation over time.

We’ll also inflate healthcare cost closer to 7%. There are other things that we can adjust the US inflation rate for on certain expenditures. If you adjust that inflation rate just a little bit, either higher or lower, it has a dramatic impact on the success of that plan.

Anybody that hasn’t factored in inflation potentially being higher than the 2% to 2.5% that it had been running at for the last 25 years needs to revisit their plan. Now we’re getting US inflation running 7% and possibly 3% to 4% this year. If their plans didn’t account for that, that means that they run the risk of suffering a reduced lifestyle or spending some of the principle that they didn’t necessarily want to spend.

Bud Kasper: At the Lee’s Summit office, we just made an adjustment in the inflation rate we’re using on our plans to 3.9%. Dean is right on target with that. These are the things that we exponentially need to alter to get a serious number. It needs to be something that people can understand what is happening, how it’s impacting them, and to counteract it if they can.

And this is nothing new. Dean and I have doing this for 30-plus years. It’s nothing new to us from that perspective, but it always feels a little different, doesn’t it?

The Financial Triple Threat

Dean Barber: It does. While it’s nothing new, it’s still uncomfortable because this high US inflation is something that we haven’t seen for some time. We’ve prepared for it and assumed that there’s higher inflation numbers, but the scariest thing are the elevated market values.

You have inflation running rampant. The Federal Reserve committed to raising rates at least three times, possibly four, in 2022. The end of the tapering will be done by the end of first quarter or early in the second quarter. So, you have the threat of rising interest rates, elevated market valuations, and have high US inflation. It’s a triple threat.

Is a Bear Market on the Horizon?

The markets are going to be volatile when you get that combination. We have seen those markets be very volatile so far this year. The question is whether we are headed toward a potential bear market or if it’s just normal market volatility based on the economic conditions that we find ourselves in today.

Bud Kasper: I always go back to the basics. Remember that the stock market is a gauge of a profitability of companies—let’s say the S&P 500 index. If those companies are profitable, they can justify where their price level. They are right now. I think that’s one thing that we need to keep in our pocket.

Other Things to Keep in Mind

The goal is to work through the end of the year without any extemporaneous activities that could disturb us. That includes Russia going to the Ukraine, North Korea doing the stupid things it does all the time, etc. The good thing that’s coming out of a lot of this is the United States is picking up some production back in the United States or transferring it out of China. That needs to continue, but you know how businesses are. They’re looking for the greatest profit margins they could bring in. If they can get cheap labor, that’s where it is.

What bothers me the most right now is how parents are being impacted by decisions related to Omicron. Since the decisions are being made on a state-by-state basis, people are saying the teachers don’t want to teach because of their fear of Omicron. Therefore, parents are coming in and teaching.

It’s a cascading effect because a lot of those people would be working, but now they volunteer because they want their children to have them have an education. They’re now going into the schools and are no longer productive with what they can contribute to businesses. It’s a crazy world from this perspective. This darn disease has really caused a lot of angst in so many different areas and we’re not through with it yet. But I believe if it’s going to start winding down toward the end of the year.

Potential Fallout from Federal Reserve Decisions

Dean Barber: I think so too. I think that the biggest risk in the market today is the Fed getting too aggressive. What if we don’t have a soft landing and end up having a hard landing and going into a recessionary period?

I think this is a time where corporate earnings are going to be strong. While I think we’re going to see some choppiness, I think we’ll see a positive year this year unless the Fed overdoes it. But I also believe that this is the time when people should be looking at their overall financial plan and understanding their personal return index. That is the return is required on your money for you to accomplish your objectives.

Once you know that, you can determine the least amount of equity that you can have in your portfolio and still accomplish your overall goals. That is a defensive play based on where we are today. If you haven’t built a plan, the first thing you need to do is build one. Once you build that plan, then you can get the answer to what the least amount of risk is that you can be taking in your portfolio and still accomplish your objectives.

Protecting Yourself from Inflation Through Financial Education

My suggestion would be to position yourself like that right now until we start to see what’s going to happen with the Fed, Omicron, and corporate earnings. Give yourself some protection. That also starts with educating yourself by reading articles like Shane’s, so make sure you read, Inflation and Supply Chain Issues Are Intertwined. He’s got a lot of supporting material there, charts, and graphs to pull it all together in that article.

Bud Kasper: Dean and I do a tremendous amount of reading. Unfortunately or fortunately, it comes with the job to try and familiarize ourselves with so many things that are impacting the financial plans that we’re creating for our clients.

Shane has become my favorite author. He has incredible insight. His details are impeccable. He provides a better perspective on things that are going on right now, so kudos to him. He’s got a flare about how to bring it home and ground it down sometimes so that we can understand some of the important facts that he shares with us in his articles.

Dean Barber: He can write on multiple sides of an issue. That’s another kind of neat thing. The reader can come to their own conclusion. It’s an educational way that he writes that I think is so good. Along with reading Shane’s article, check out our latest piece on 7 Ways to Build the Best Retirement Plan, and our other educational content, Being educated on US inflation is critical. Right now, we have is a scenario where things could go either way. You want to make sure that you’re protected.

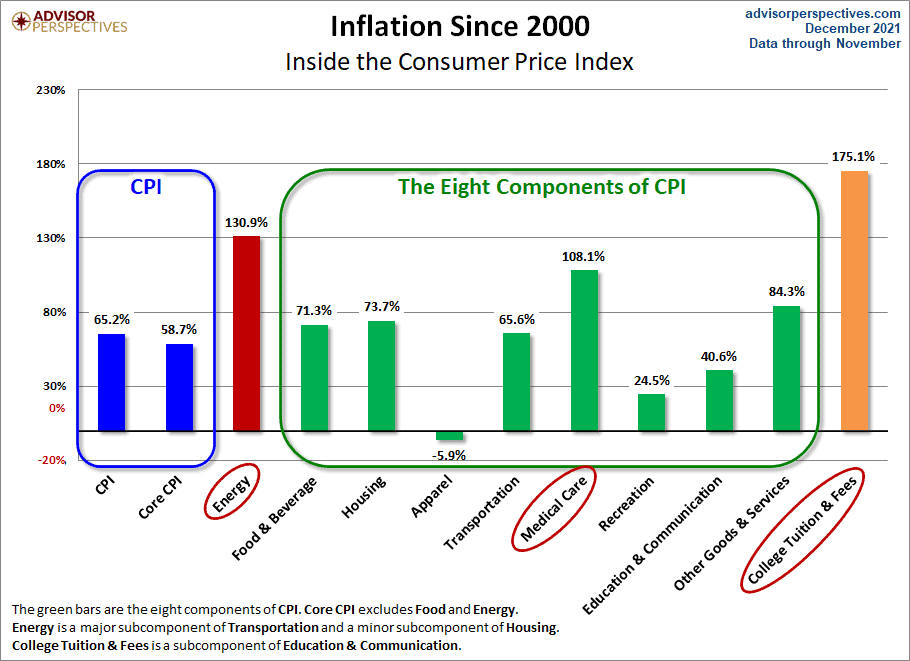

Checking Out the Components of the Consumer Price Index

One chart I want to point out in Shane’s article outlines the components of the consumer price index. Let’s look at Figure 1 below.

TABLE 1 | Inflation Since 2000 | Advisor Perspectives

If we go back to 2000 and up through the end of 2021, the CPI has risen by 65.2%. Core CPI has risen by 58.7%. You could easily take those, divide them by 21, and that’s your average annual rate of US inflation since 2000. But if you did that, I think you sell yourself short in your financial planning process. By doing that, you’re not applying the proper inflation rate to where you’re spending money. That’s a critical thing to do.

Bud Kasper: I agree. It’s interesting that people sometimes don’t think about some of the components having very much of an US inflationary impact. But there’s nothing that’s left out of it. Apparel is the only one that was a negative number inside of that. The things that are important to people such as energy and college tuition and fees have gone up exponentially with that.

Insane Energy Cost Increases

Dean Barber: If you look at energy alone since 2000, you’ve got 130.9% increase. The other one that I think hits our target audience the most is medical care because. Bud and I both know that the older we get, the more medical care we need. We really need to pay attention to the increase in medical costs.

Over the last 20 years, medical care has increased by 108.1%. And then your food and beverages up by 71.3%. If you think about when a person goes into retirement, where are they spending most of their money? Food, energy, medical care, and then other goods and services that are up by 84%.

They probably don’t have to worry about college tuition and fees, which was up by 175.1%. But those people that have kids that are younger and are trying to plan for that. They need to understand that college tuition prices are going up at a much faster rate than the core rate of inflation.

Bud Kasper: Yeah. When I look at Figure 1 and see that energy up 130.9%, it just frustrates me. That didn’t have to happen. When Biden came in, the first thing he did was shut down the Keystone Pipeline. He impacted that directly in terms of how oil prices and prices that the pump were going to go increase. It wasn’t necessary.

It’s important for America to work on climate change, but why suffer in the meantime while you’re trying to get to the result that everybody would probably rather see? It just doesn’t make any sense to me.

The Domino Effect

Dean Barber: I agree. Bud is spot on there because we were totally energy independent and a net exporter of energy. But the Biden administration has obviously changed that. On my trip down to Florida, virtually every gas station that I stopped at had a little Joe Biden sticker of him pointing to the price on the gallon of gas with the caption saying, “I did that.”

Bud Kasper: Only people as old as I am remember when we had odd and even license plates that told you the day that you could go in and fill up your tank. That’s how bad things could get when the supply side of it is not where it needs to be.

Dean Barber: When you start talking about these increases in energy prices, that leads to increase in shipping costs. That then leads to an increase in the goods and services that are provided, so it’s a domino effect. I don’t know that we’re going to see those energy prices come down anytime soon because of what the Biden administration is doing. That is the one part of our inflationary scenario that really has nothing to do with supply chain and all it has to do with is government policy. I think inflation will continue, but just not at the 7% per year that we’ve seen over the last year.

You Don’t Have to Live Like You’re Broke Because of Inflation

People need to rethink their financial plan and how they’ve put inflation in there. They need to look at it in the context of the different components of inflation and the economy. How much money are you spending in that particular component? Inflate that amount of money at that rate. That’s going to give you a far more accurate look at the reality of your financial plan and you doing all the things that you want to do as you reach and go through retirement.

Bud Kasper: It’s like you’ve said many times that inflation won’t cause you to be broke, but it will make you live like you’re broke. This is one of the things that happens. Suddenly gas is going up and some people allow that to manipulate their minds. They won’t travel as much because they don’t want to pay a certain price for gas. Unfortunately. it’s a negative cause and effect.

Dean Barber: It is and it’s leading to higher prices at our grocery stores as well. People are feeling the impact of US inflation. A lot of people are saying that they need a raise or more income to be doing the same things. Well, if you built your plan properly in the first place, that raise would be automatic.

Let’s say you account for a 4% US inflation rate on an annual basis in your portfolio. Do you want that 4% raise this year or not? You might say, “I’ll take 2% or 3% more, three more.” A couple of years later you might say, “No, I need 7% because I want to continue the same lifestyle.” That’s the key.

Don’t Let the Sequence of Returns Throw Off Your Retirement

I think inflation is one of two things that is kind of out of your control when you enter retirement. However, can still plan for it and make sure your plan is ready for inflation. That can help.

The other thing you can’t control in retirement is the sequence of returns. Bud joined me recently on the Guided Retirement Show™ to take an in-depth look at the sequence of returns. We discuss the importance of being properly positioned so that the sequence of return can’t throw off your retirement. You can listen to the episode on your favorite podcast app or on YouTube.

Wild Swings in the Market

As Bud and I try to wrap up this discussion on what is making this inflationary pressure so hot right now, it’s important to ask a few questions that we touched on earlier.

- Do we go into a soft landing?

- Does the Fed overdo it?

- How soon do the supply chain issues get fixed?

There are a lot of different components to this. Those different components are causing the market to be bipolar. Some days you’re going to get a big upside and then the next day you might get a 500-point down day. The NASDAQ has been rocked more than any other major market index. Does that mean that technology can’t do well in a US inflationary or rising interest rate environment?

Safely Entering the Technology Sector

I think that’s silly. The advancement in technology is going to continue to change the way that we live. The major companies that are developing this technology are going to continue to be winners. People should be looking for opportunities to enter that technology sector in very careful ways. I think there’s going to be a lot of opportunity that’s going to present itself with this volatility.

Bud Kasper: I agree. If you go back 25 years or so and look forward, it’s amazing what difference technology has made to our lives. I don’t think there’s any reason why that is going to change.

The Latest Tech Trends

Look at what Microsoft did this past week. Microsoft spent a ton of money for a gaming company. This is going to entertain us. It’s going provide us exponential ways that we can engage and work through that type of a format. Once again, Moore’s Law is proving to be true. Every three years, the power of the computer is dramatically changing the way we live our lives. In my opinion, it’s been all for the good.

Dean Barber: There’s no question about it. The major tech companies that are trying to develop a set of eyeglasses or sunglasses that will have the same or better technology than our cellphones.

There’s speculation that these new optical glasses will actually take the place of your cell phone. You can make a phone call, read your emails, watch movies and much more with this technology. I believe that is what Microsoft’s purchase of this gaming company is doing. They want the technology that that company.

All the big companies want to be the leaders in this new technology—Google, Microsoft, Amazon, the list goes on. There are companies out there that have the components necessary to create this technology. I still think that we see a major shift.

We can’t pretend that the iPhone or the Android phone is going to be what it is today 10 to 15 years from now. Do you remember flip phones and bag phones? We’ve had a progression there. Now, we have a smartphone and essentially have a computer in our hands. It’s more powerful than anything we had available to us just 15 years ago.

Analyzing the Ripple Effects of Technology

That technology is going to continue to improve. You need to look for the companies that are going to bring that technology to the table. Think about the ripple effects of how that’s going to affect our everyday lives. The fact that the NASDAQ is getting beat up over this threat of rising interest rates and tapering from the Fed is an opportunity. It’s not a time to panic and get out of technology.

Bud Kasper: I agree. I’ve looked for a correlation between rising interest rates and technology, but I don’t get it. Nevertheless, it’s happening, so we need to recognize it for what it is. I haven’t had the experience of having an Oculus headset, but I’ve heard that it’s so incredibly real.

It’s a whole new dimension of gaming and things that we would like. We can pretend we’re skiing or whatever the case may be. So that’s kind of exciting from that perspective. Of course, I count on my children to bring me up to speed and tell me how good it is. But, nonetheless, it’s a fascinating field.

And, by the way, Microsoft doesn’t make very many mistakes. That’s one heck of a company. Companies are using artificial intelligence for the picking of stocks, bonds, or anything like that.

Looking Back on a Big Win for Watson

Think back to when IBM created Watson. It’s a computer that is constantly learning every second of the day. To prove the power of Watson, Jeopardy! had it go up against two of its all-time champions. They pitted Watson on live television against these two guys. The two human contestants finished with like $3,000 and $25,000, respectively, but Watson won with $70,000.

As the show was going on, you have this computer that is learning from the people that it’s competing with and getting an advantage. I think that’s what technology is about—a few advantages that you didn’t have before. Let’s embrace it.

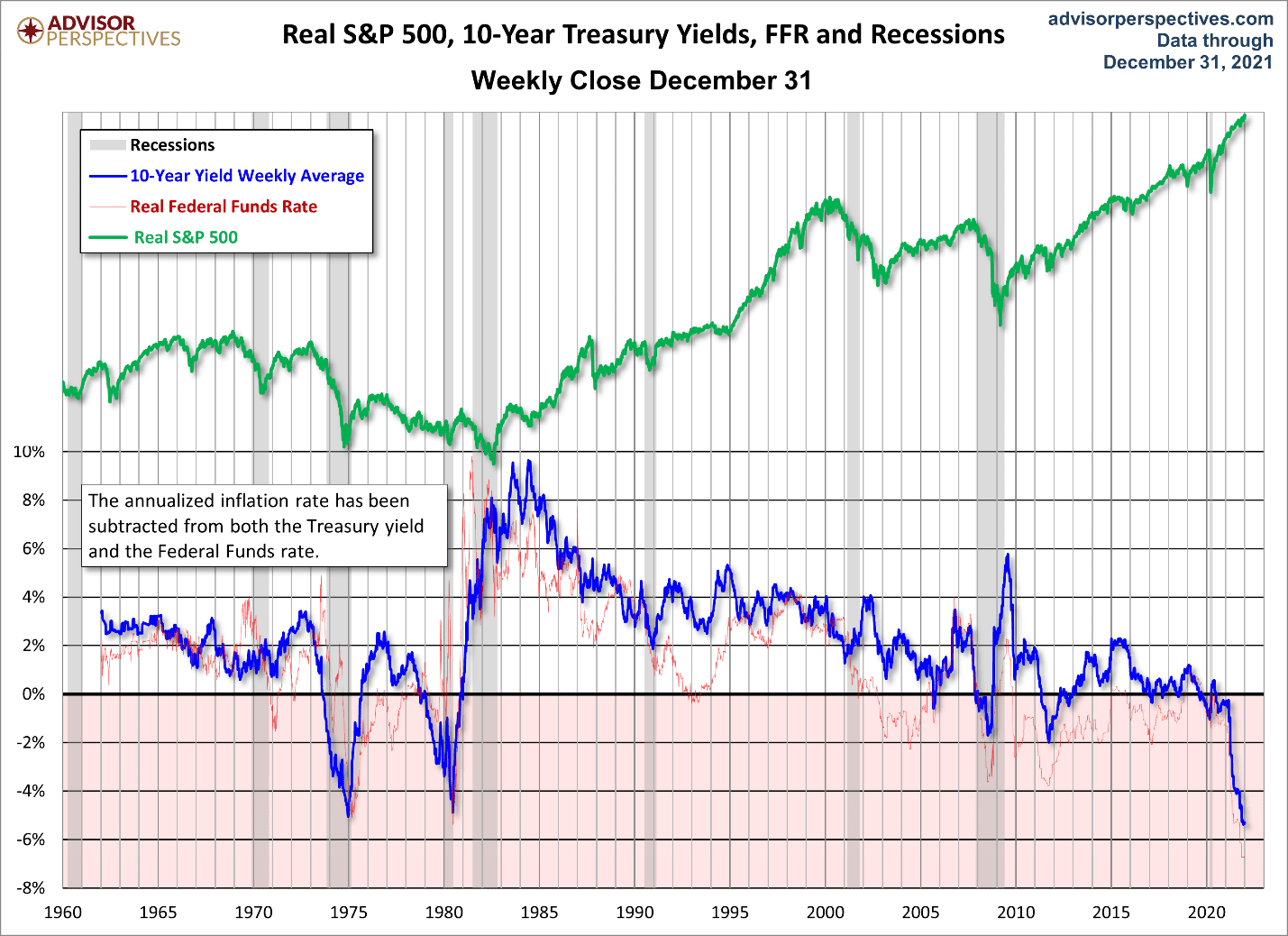

Dean Barber: It’s going to continue to advance and change the way that we live. I want to go back to this idea that you can’t make money in the stock market in a rising interest rate environment.

Figure 2, below, was used in Shane’s article shows us that when we came out of all the quantitative easing from the Federal Reserve after The Great Recession, the Fed started raising interest rates from mid 2011 up through 2016. We saw a gradually rising market. It wasn’t a straight up line, but the markets had good returns during that period.

You can look at the volatility shown in Figure 2 and see that it’s a bit greater than if you were simply in an environment like what we were in last year with a zero-interest rate policy in place for the last two years. But, nonetheless, I don’t think people should get discouraged.

Feel Free to Reach Out to Us with Questions About Inflation

People need to understand that we’re going to have increased volatility and risk. Go back to your financial plan and make sure that you have the right amount in each asset class.

Once again, make sure you read Shane’s latest article, Inflation and Supply Chain Issues Are Intertwined to get a better understanding of US inflation. If you have any questions about inflation and how to account for it in your financial plan, schedule a 20-minute ask anything session or a complimentary consultation with one of our CERTIFIED FINANCIAL PLANNER™ professionals. You can meet with us virtually, by phone, or in person.

We appreciate everyone who listens to America’s Wealth Management Show. I’m Dean Barber, along with Bud Kasper. Stay healthy, stay safe, everyone. We’ll be back with you next week. Same time, same place.

Schedule Complimentary Consultation

Click below and select the office you would like to meet with. Then it’s just two simple steps to schedule your complimentary consultation. We can meet in-person, by virtual meeting, or by phone.

Schedule a Complimentary Consultation

Investment advisory services offered through Modern Wealth Management, Inc., an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Advisor. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.