The Inflation Reduction Act Has No Impact on Inflation

Key Points – The Inflation Reduction Act Has No Impact on Inflation

- Analyzing the Inflation Reduction Act’s Provisions

- Why the Inflation Reduction Act Could Actually Increase Inflation

- Another Layer of Taxation on Already High Prices

- Whether Inflation Decreases or Increases, You Need to Have a Financial Plan

- 17 Minutes to Read

What to Make of the Latest Inflation Numbers

As you are all aware, inflation has been running at 40-year highs for the last several months. It’s affecting the pocketbooks of most Americans. The latest inflation numbers for the month of July show that inflation was lower than expected and were lower than June, indicating that we may have seen the peak in inflation already. And inflation in August was lower than July, further evidence that June was the peak.

However, that doesn’t mean that some in Washington, D.C. won’t take the opportunity to put forth a 730-page bill full of pet projects, written in nonsensical language, that doesn’t address the problem, but name that same bill as if it’s designed to. And they have.

It’s called the Inflation Reduction Act. It was delivered to the president, and he officially signed it into law on August 16. However, as we’ll discuss today, the Inflation Reduction Act contains zero inflation-fighting plans. In fact, the lack of inflation reduction in the bill has led those associated with it to call it the “deficit reduction act,” which is also a misnomer. One thing that is clear, though, is that it’s imperative to have a financial plan to understand how legislation like the Inflation Reduction Act impacts you personally. I’m hopeful that you’ll see the importance of that throughout this article.

More Like the Increasing Inflation Act?

By my reading, and in the analysis of people a lot smarter than me, the bill will result in increased inflation, higher deficits, higher taxes…for everyone. Hold on, I’m not done yet. The Inflation Reduction Act appears to also include a more than doubling of the size of the IRS, dramatically increased tax audits, higher energy costs, and the end of innovation in life-saving drugs. Those are just a few things, and hopefully, we’re all wrong about them. But time will tell.

To say that there has been a lot of bad legislation since the onset of the Financial Crisis in 2008 would be an understatement. We’ve spent trillions of dollars in the last 14 years in the name of “fixing” insert cause here. But this the Inflation Reduction Act may be the worst. To read the complete text of the Senate version of the legislation, click here, if you are into that kind of thing. And you can click here to read the version of the legislation that was recently passed by the House.

Breaking Down the Inflation Reduction Act’s Major Provisions

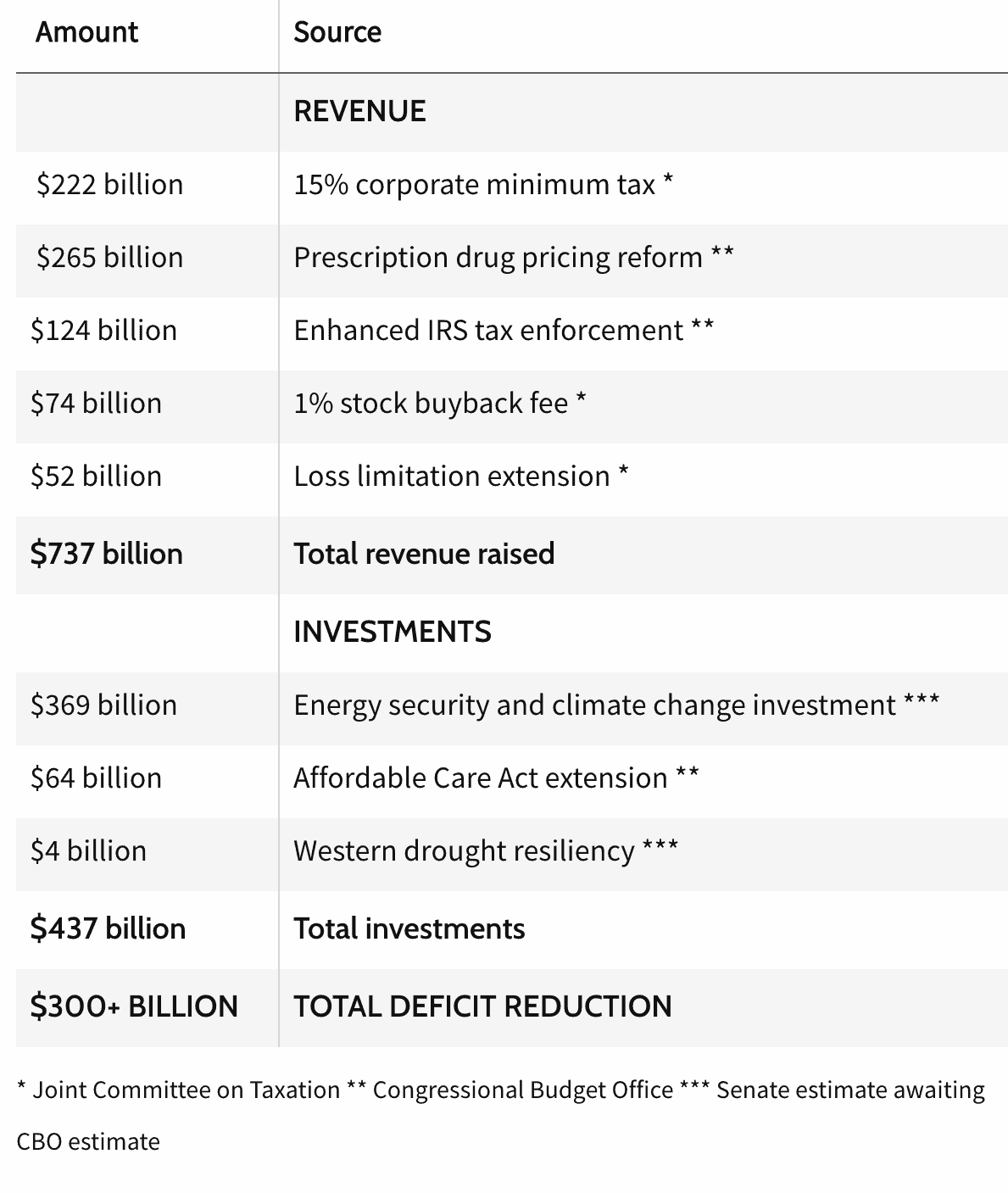

So, let’s dig in and look at the major provisions in the Inflation Reduction Act. I’ll begin by highlighting a very high-level overview of the anticipated revenues and outlays below in Figure 1.

Note that the financial success of the Inflation Reduction Act relies almost exclusively on three provisions. Those are the 15% corporate minimum tax, the regulating of prescription drug prices, and “enhanced IRS tax enforcement.” If any or all of these three provisions fall short of their projected revenue growth, the supposed deficit reduction goes away very quickly. Conversely, if any of the projected spending increases (I know, I know, the government never spends more than it says it will) the alleged deficit reduction goes away. But trust me, there’s more. Let’s look at the provisions individually and see what’s in the details.

The 15% Corporate Minimum Tax

We’ll look at the revenue side first, starting with the 15% corporate minimum tax. This provision imposes a 15% minimum tax on corporate book income for corporations with profits over $1 billion. It becomes effective for tax years beginning after December 31, 2022.

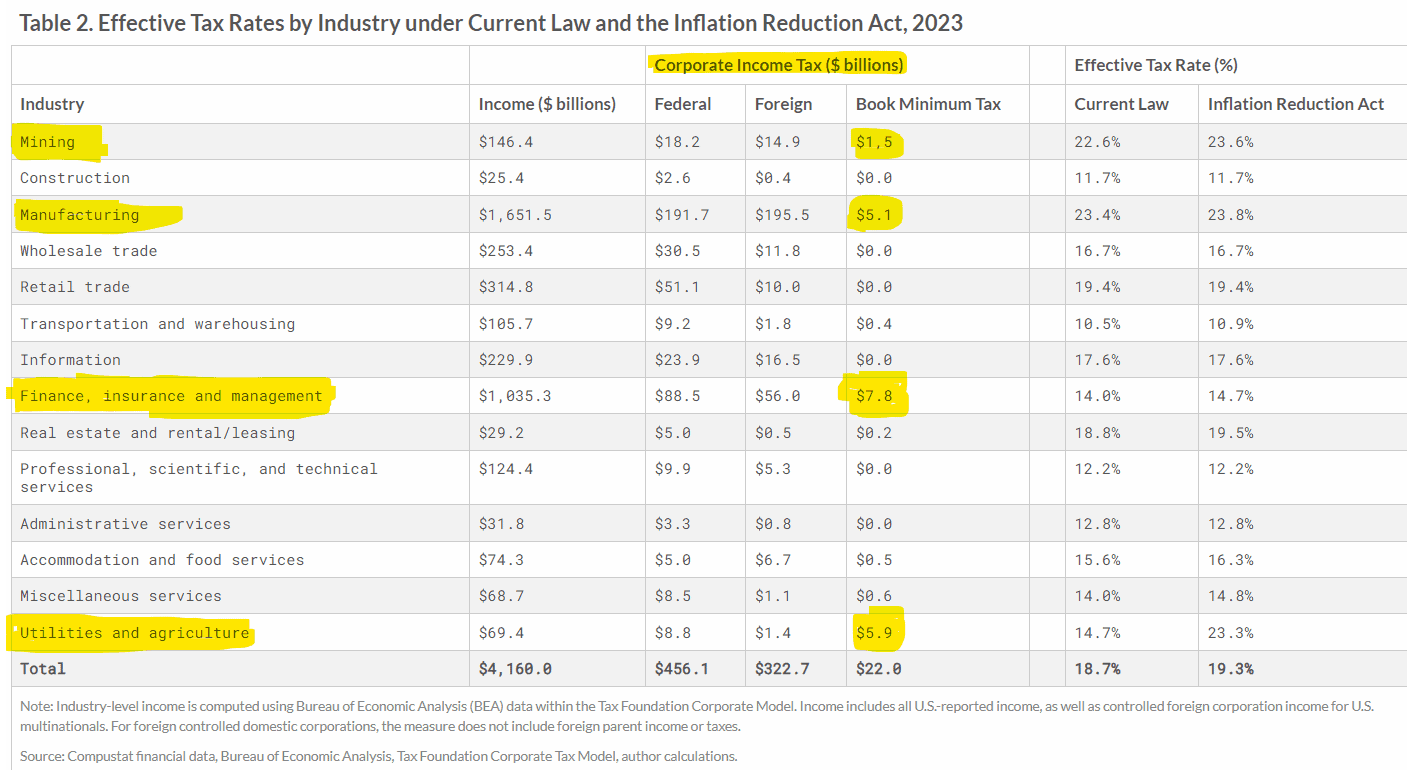

A firm is considered affected by the tax if its adjusted financial statement income averaged over the previous three years exceeds $1 billion. Once a firm becomes affected by the tax, it remains affected for all subsequent years. Tax Foundation conducted an analysis of the industries that will be most affected by the new tax. Figure 2 offers a glance at how 2023 looks.

Note that four industries are going to bear the burden of this tax and note: mining, manufacturing, finance, and utilities and agriculture. Of the $22 billion expected to be raised in 2023 by this tax, $20.3 billion will come from those four. Fully HALF of the projected revenue will come from just two industry groups, manufacturing and utilities and agriculture. Seems lopsided, doesn’t it? That’s because it is.

The Impact of These New Taxes

I need to have a short side bar discussion about who pays taxes and who doesn’t because it’s important to understanding the effects of these new taxes. I’m going to try and make this as simple as I can. Here it goes.

Even though they may write checks to the IRS every year, corporations (mostly) do NOT actually pay taxes. You, their customers, pay the taxes for them. They estimate how much they are going to sell every year and know about how much money they are likely to make in that year.

They then estimate the tax liability they’ll have and incorporate that into the price of the goods or services that you buy from them to meet their profit objectives. So, when they write that check to Uncle Sam, they’re sending YOUR money. It’s been this way since federal income tax became a thing, and it’s not going to change.

Increased taxes on any business or industry DIRECTLY affect the prices you pay. Period. Which means tax increases on businesses or specific industries are tax increases shouldered by YOU, the consumer. You may not think it’s fair, but it doesn’t matter. It’s a fact you must understand.

Some Important Questions to Ponder

So, ask yourself. If the Inflation Reduction Act is about inflation reduction, why are we going to increase taxes on the industries that produce the very goods and services having the largest daily impact on your wallet? How will that help?

Have you seen your electric bill lately? Mine has doubled from last year. Have you been to the grocery store lately and bought beef? It’s $20 a pound for Ribeye steak. Have you tried to buy new furniture or appliances lately. They’re super expensive and take months to get. Do you think your bank fees are too high? Do you think mortgage rates are too high?

What about insurance? Do you think insurance is too expensive and doesn’t cover anything when you need it? What about the cost of propane and natural gas? And yet, we’re going to add another layer of taxation on top of already high prices? To fight inflation? Really? To make matters worse, it’s estimated that this provision will eliminate 20,000 jobs and reduce GDP by 0.1%.

How to Plan for Inflation on America’s Wealth Management Show

The Federal Reserve is raising interest rates to combat it, but inflation still looms large over the US economy. How do you build a plan that considers such a surge in inflation and interest rates? Find out as Dean Barber and Bud Kasper discuss how to plan for inflation.

Prescription Drug Pricing Reform

Let’s move on to the next item: prescription drug pricing “reform.” We all want prescriptions to cost less, but how are they going to reform prescription drug pricing in a way that produces revenue to the federal government to the tune of $265 billion over the next 10 years?

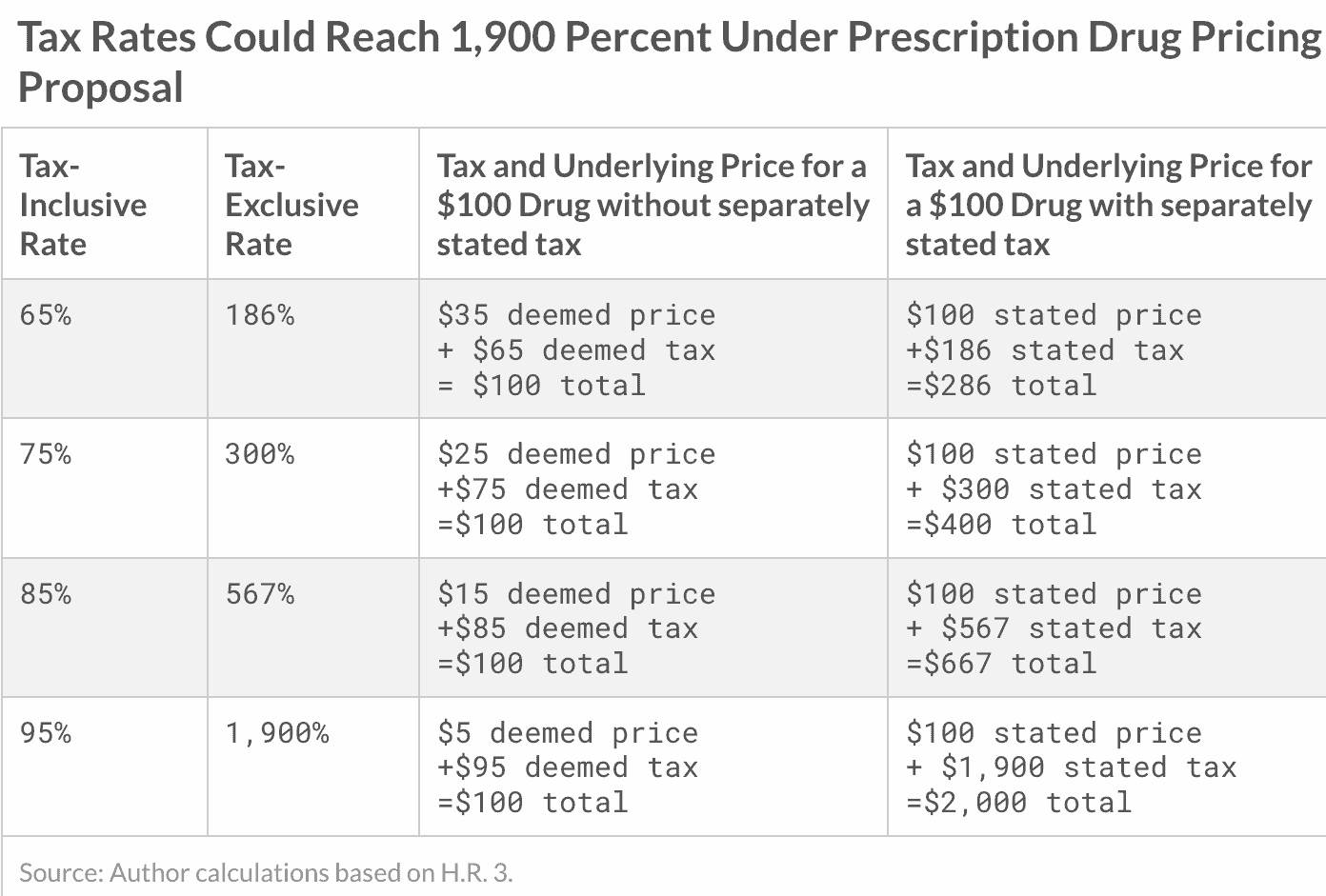

Good question. The short answer is…they can’t. Here’s what they are going to do. They are going to force pharmaceutical companies to “negotiate” prices on existing drugs with Medicare. If they choose to opt out of the negotiations, they will be hit with the most punitive excise tax scheme ever devised by man. Look at Figure 3 below to see what I mean.

The Joint Committee on Taxation (JCT) “expects” that all manufacturers would participate in the price “negotiations” rather than pay the ridiculous excise taxes on drug sales or pull a particular drug(s) off the U.S. market. The authors of the legislation believe that government-set prices would lower spending by the federal government over time. So, the provision provides no real income, though it’s touted as bringing in $265 billion to be spent over the next 10 years. Color me skeptical.

A Not-So-Healthy Decision

The reality is that the cost of this is going to be bourn by us, as pharmaceutical companies pull back on research and development and lay off workers due to dramatically reduced profitability. Bringing new drugs to market takes a LOT of time and a LOT of money…to the tune of billions of dollars per drug. If there is no financial incentive to do so because the government is setting the prices, you can kiss innovation in life-saving drugs goodbye.

“The reduction in R&D, innovation, and new drugs is why the nonpartisan CBO, when analyzing past versions of drug pricing legislation, found, ‘The overall effect on the health of families in the United States that would stem from increased use of prescription drugs but decreased availability of new drugs is unclear,’” Tax Foundation Senior Economist, Research Manager Erica York said. “In other words, it is not a clear win for Americans’ health to force lower prices for certain existing drugs today at the expense of the development of new drugs tomorrow.”

Enhanced IRS Tax Enforcement

This next provision is probably everyone’s least favorite, except for the 87,000 new agents who will benefit from it. I’m talking about the enhanced IRS tax enforcement provision, which will cost the taxpayers $80 billion over the next 10 years. That $80 billion isn’t included in the “spending or investment column.”

Instead, they assume that enhanced enforcement will produce $204 billion in gross revenues over the next 10 years which, minus the $80 billion spend, would be a net new revenue of $124 billion. It has been calculated that the IRS could/would add 87,000 new agents with the money they’ve been allotted to facilitate these enhanced enforcement goals. This is not a number that people made up. The IRS actually published it in a report last year.

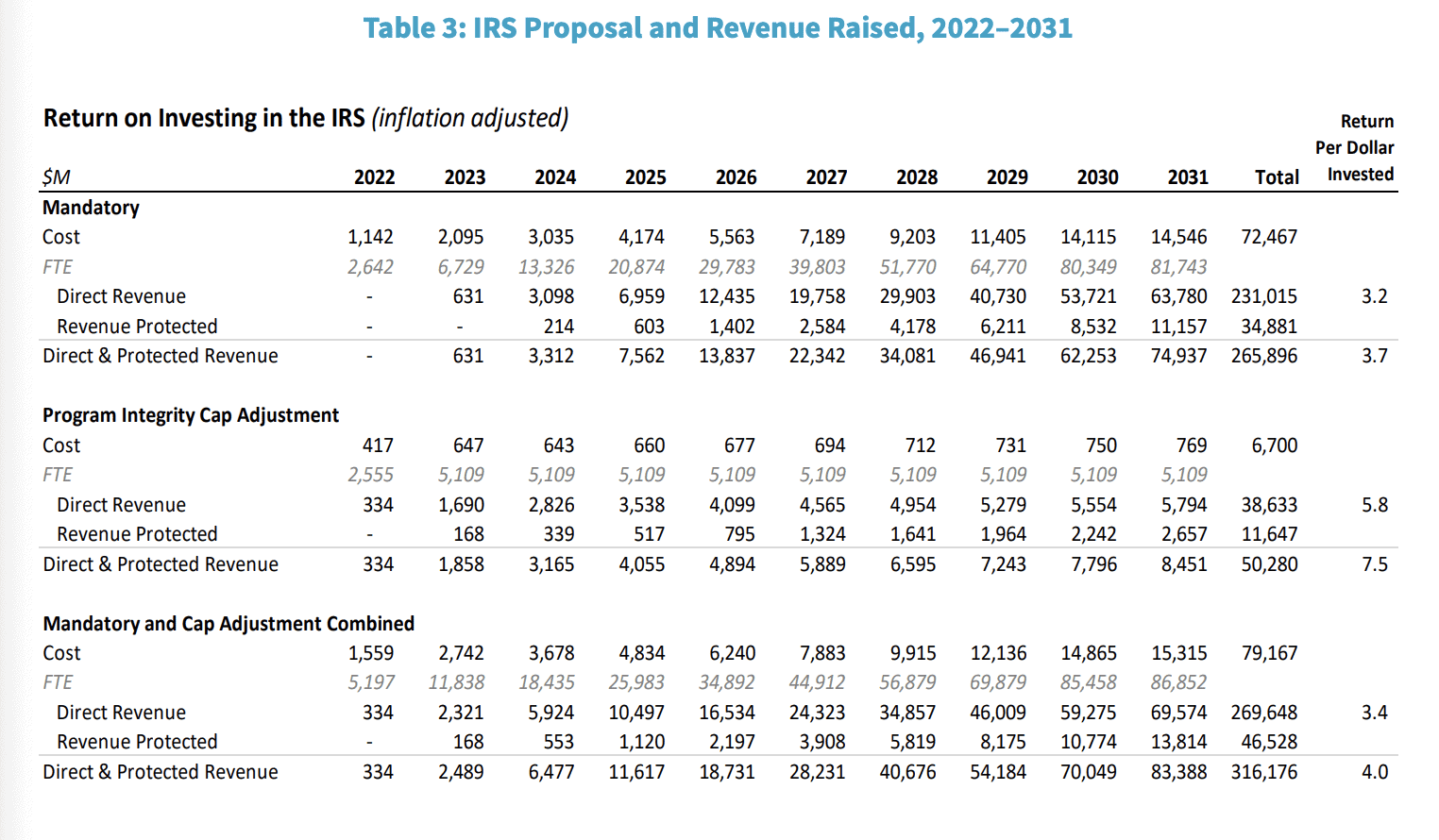

Figure 4, below, is from that report and shows the numbers. The IRS currently has roughly 81,000 employees, including 10,000 part-time workers. An additional 87,000 full-time employees would more than double the size of the agency from today.

FIGURE 4 – IRS Proposal and Revenue Raised, 2022-2031 – The U.S. Department of the Treasury

Look Out for Uncle Sam

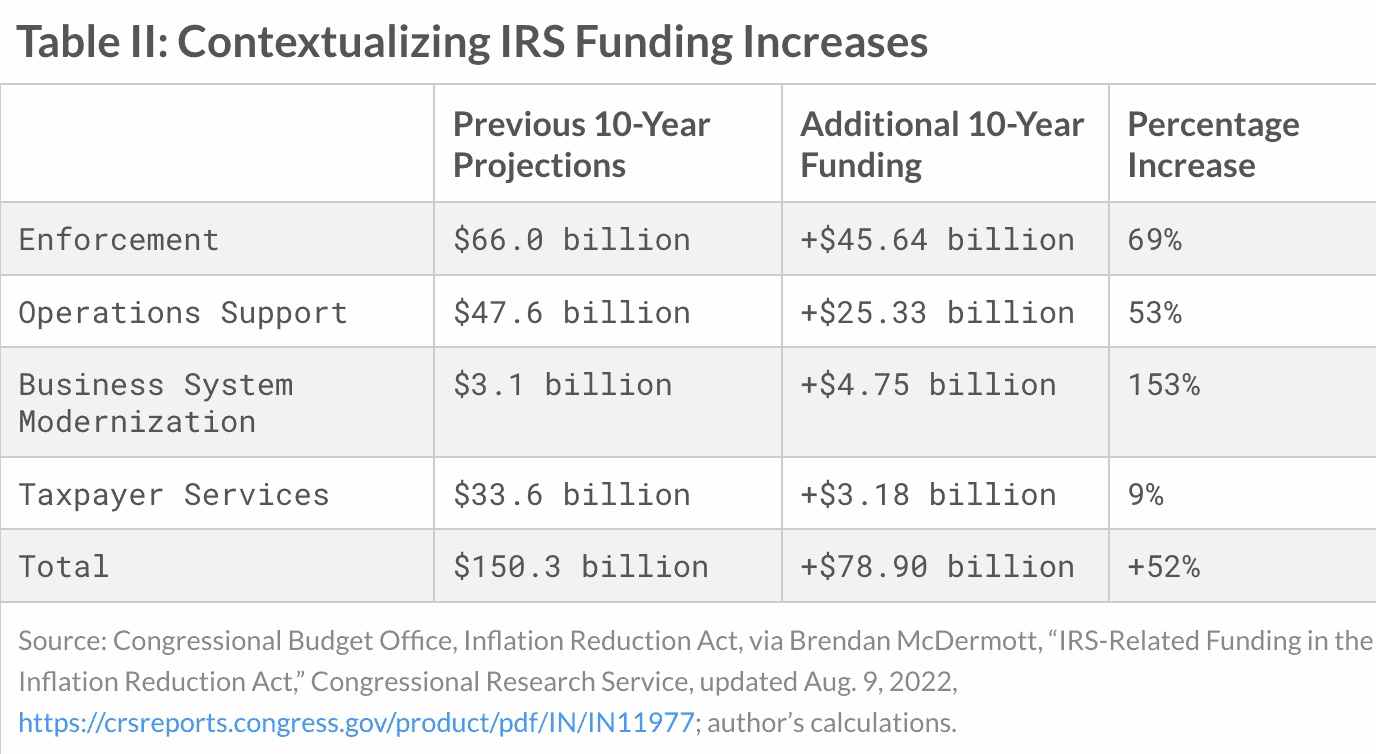

And look at where the $80 billion is going to be spent. A 69% increase in enforcement, a 53% increase in operations support, a 153% increase in business system modernization, and a PALTRY 9% increase in taxpayer services. That seems sketchy to me.

It seems like we’re not the focus, but rather the target of this new spending. Look out middle class taxpayers, crypto purchasers, and small businesses. You have money, and Uncle Sam wants it.

FIGURE 5 – Contextualizing IRS Funding Increases – Tax Foundation

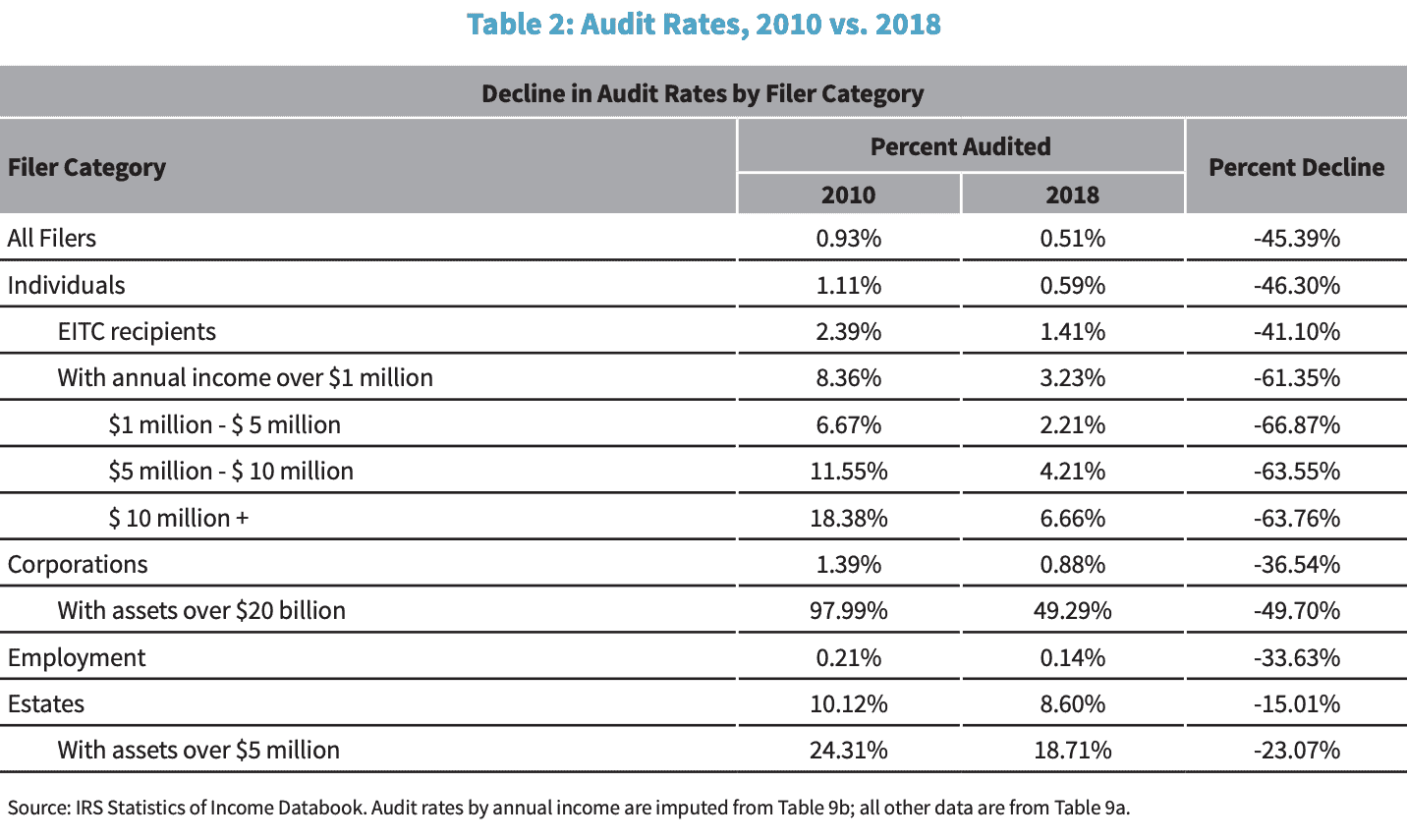

The IRS’s case to Congress that it needs additional funding laments the fact that audit rates have fallen by roughly half since 2010. Look at Figure 6 below.

FIGURE 6 – Audit Rates, 2010 vs. 2018 – U.S. Department of the Treasury

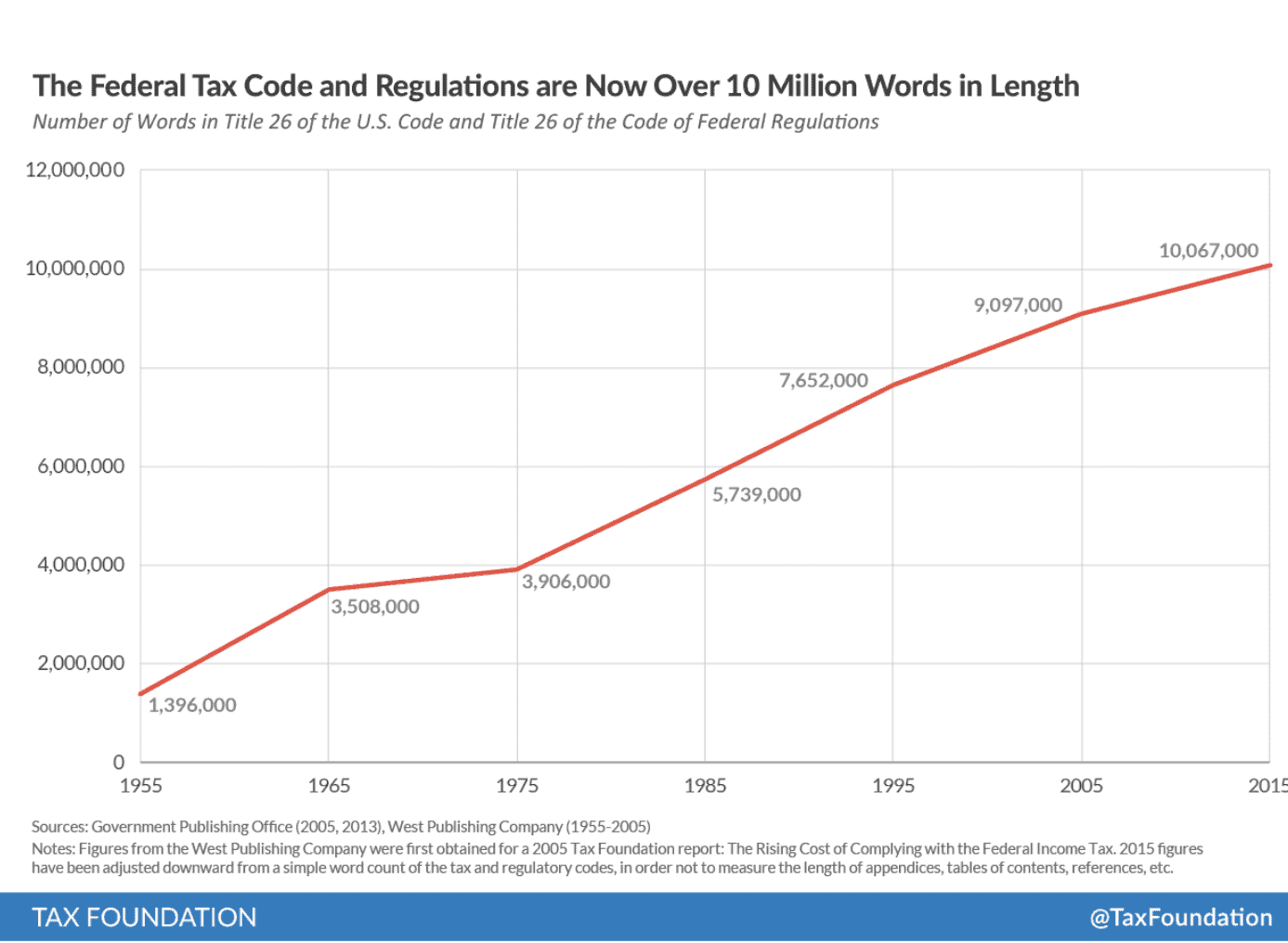

How Is Anyone Supposed to Understand the Tax Code?

Apparently, the IRS wants to be the new helicopter mom that looks over everything that everyone does to ensure that none of “their” money goes uncollected. This is despite having an incomprehensible 10-million-word tax code that absolutely no one understands—not even the IRS. In fact, if you have 46 different tax preparers complete the same family’s return, with the same exact information, you’ll get 46 different results. Audit bait for sure.

Wouldn’t a better, far simpler, and far less costly solution be to just simplify the tax code to make compliance with it easier? Call me crazy, but I think so.

The 1% Excise Tax

Next up is the 1% stock buyback fee (excise tax) that will be assessed on all stock buy backs in the future. This provision is estimated to raise up to $74 billion in additional revenue. But there’s a problem. That estimate assumes that stock buyback behavior will remain unchanged in the face of additional taxation. That’s a poor assumption.

Businesses usually engage in stock buybacks when they’ve exhausted reinvestment opportunities and are looking to reinvest in their own business while returning value to the shareholders. Currently, 95% of funds received by shareholders from repurchases get reallocated to other public companies. So, it’s an efficient way for the market to reallocate assets.

Another way a company returns value to its shareholders is through the issuance of dividends. And, since most of the corporate stock is held in tax-preferred retirement accounts, if the corporations who were otherwise inclined to do stock buybacks issue dividends instead to avoid the 1% excise tax, this provision may prove to be far less valuable than the $74 billion estimate. I predict that is exactly what is going to happen. Tax Foundation Federal Tax Economist Alex Durante put it nicely in the excerpt from his recent article.

“Overall, the new buyback tax introduces uncertainties and potential downsides in terms of the efficient allocation of capital. With inflation still running high and the economy showing some signs of slowing, now is not a good time to try out a new tax of this nature.”

Loss Limitation Extension

Finally, we come to the last item on the list of “revenue” generating provisions in the bill. And that item is the loss limitation extension, which is estimated to generate $52 billion over the next 10 years. Allegedly, in the years 2027 and 2028, this extension will collect an average of an additional $26 billion in each of those two years.

Again, color me suspicious. The loss limitation pertains to sole proprietorships, S Corporations, and LLCs, which are “pass through” entities. That means that they pay taxes at individual income tax rates. These are small businesses, mom-and-pop types, that sometimes suffer large losses through no fault of their own, i.e., COVID lockdowns.

Under the current rule, they can only write off losses below a certain threshold. And they must eat the rest of the losses regardless of whether the loss was out of their control. By the way, these people in large part are not rich. In most cases, everything they have is in that business, and those losses devastate them financially. But hey, Uncle Sam needs to pay for some new spending. So, suck it up mom and pop.

Why Gas Could Go Even Higher

Another fun feature of the Inflation Reduction Act is that it raises the Superfund Tax on crude oil and imported petroleum from 9.7 cents to 16.4 cents…indexed to inflation…and increases other taxes and fees on the fossil fuel sector. A great idea when gas is already too high.

That provision is projected to bring in an additional $13.7 billion over the next 10 years and is guaranteed to raise the price of everything that uses energy…which is everything. Whether its electric vehicles, windmills, solar panels, they’re all going to cost more. That’s the exact opposite of the title of the bill, the Inflation Reduction Act. Weird.

Spending, Spending, and More Spending

So, since we’re raising all this new revenue, what are we going to do with it? Apply it to the deficit? Of course not, we’re going to spend it. Where are we going to spend it?

Basically, in two places: green energy and health care. That’s it. Well, kind of. There’s a whole lot of other “stuff” in the Inflation Reduction Act that no one wants to talk about, but the CBO scored it in its letter to Congress.

Specifically, Green Energy and Health Care Spending

We’ll talk about it shortly, but let’s see what’s going on with green energy and healthcare spending. The following is a list from Investopedia’s analysis of the Inflation Reduction Act.

- Tax credits for energy production and investments in wind, solar, and geothermal energies.

- Incentives to businesses to deploy lower-carbon and carbon-free energy sources.

- Tax credits for investment in battery storage and biogas.

- Tax credits for investments in nuclear energy, hydrogen energy coming from clean sources, biofuels, and technology that captures carbon from fossil fuel power plants.

- Bonuses for companies based on worker pay and the manufacture of steel, iron, and other components in the U.S.

- Incentives to companies and consumers who make cleaner energy choices.

- Tax credits for residential clean energy costs including rooftop solar, heat pumps, and small wind energy systems. 30% credit through 2032—phases down after 2032.

- Electric vehicle tax credits of up to $7,500 on new EVs and $4,000 on used.

- Tax credit for energy efficiency in commercial buildings.

- Grants and loans to help companies reduce emissions of gas methane from oil and gas.

- Fees levied on producers with excess methane emissions.

- $27 billion toward additional incentives for clean energy technology.

- $3 billion for environmental justice block grants—community-led programs that address harms from climate change and pollutants, including $20 million for technical assistance at the community level, through fiscal 2026.

- $3+ billion for air pollution monitoring in low-income communities with $117 million going to communities in close proximity to industrial pollutants.

- Excise tax increase from 9.7 to 16.4 cents per barrel on imported petroleum and crude oil products to fund the cleanup of industrial disaster site increases.

- Permanent extension of the tax on coal production that funds the Black Lung Disability Trust Fund, which finances claims from workers with the condition.

Those Points Don’t Touch on Inflation

Nothing in that list above says, “I’m serious about reducing inflation!” Nothing. It doesn’t even say, “I’m all about deficit reduction.” What it basically says is, “I wanted to pass all this stuff, but I couldn’t. So, I put it in a bill that I named the Inflation Reduction Act/Deficit Reduction Act because it sounded good.

If you are considering an electric vehicle and are excited to see that there are electric vehicle tax credits in the list above, you might not be as excited when you realize that they are going to be difficult to get. To qualify for the tax credit, your electric vehicle must be made in North America. Not that I’m against buying American. In fact, I’m all for it.

But this restriction means that you are going to be limited in the vehicles that qualify for the credit. The credit is also eliminated for more expensive electric vehicles like the Hummer, Lucid Air, and Tesla Model S and Model X. Additionally, the tax credit is lowered for electric vehicles with battery minerals sourced from countries other than the U.S., which is virtually all of them.

The Affordable Care Act Extension

And then there’s the Affordable Care Act extension, which extends financial assistance to enroll in the ACA through 2025. That assistance was scheduled to stop at the end of this year. This provision also expands eligibility to allow more “middle class” people to receive premium assistance.

This extension is estimated to cost $64 billion for just a three-year extension. So, I ask you, do you think they’ll eliminate this extension in 2025? Or do you think this will more likely become permanent. My bet is on it becoming permanent. If you do the math, it will cost $213 billion, at minimum, over the next 10 years. Deficit “reduction” just evaporated.

But let’s assume that the intentions of the bill are honorable and see how these two spending goals add up.

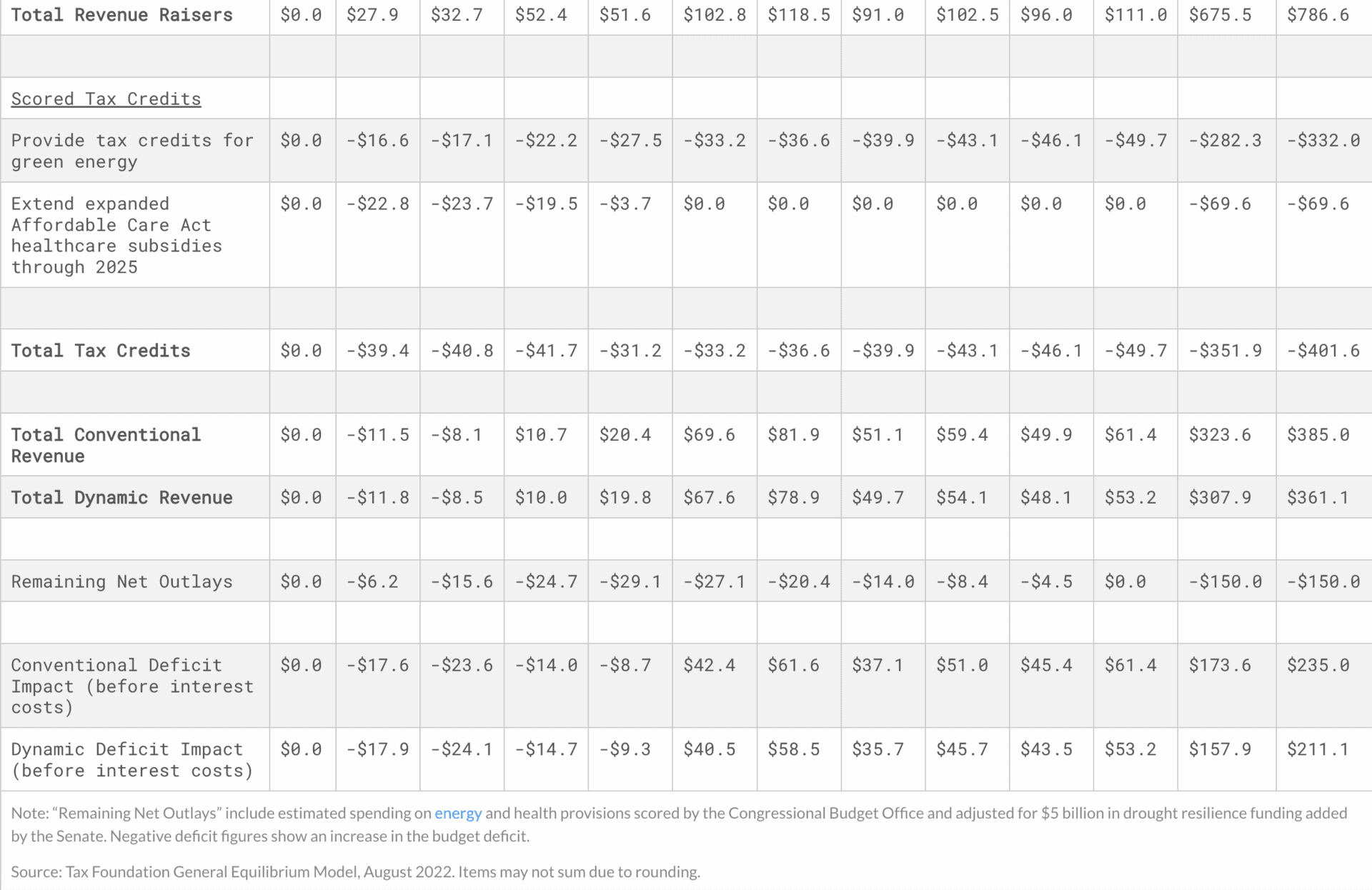

FIGURE 8 – Revenue Effects of the Inflation Reduction Act (billions of dollars) – Tax Foundation

The answer, as you can see above in Figure 8, is $401 billion of spending on these two items as currently written, the majority of which is green energy. Note below the total tax credits line is another $150 billion of “remaining net outlays.” Those aren’t even scored or explained in any analysis of the Inflation Reduction Act. And the dynamic deficit impact before interest costs is only $211 billion, if everything goes exactly as modeled.

As I said a moment ago, any change in the anticipated spending to the upside blows up any potential deficit reduction. They are attempting to thread a needle from space here. I’m not confident.

The Inflation Reduction Act Can Result in Massive Deficit Increases

But there’s something else going on too that no one has really addressed as far as I know. You see, there were amendments to the Inflation Reduction Act in the Senate on August 7. The amendments were not fully scored by the CBO before the House-passed bill went to the President for his signature on August 16. Again, click here to read the letter sent to the House chairman by CBO Director Phil Swagel. Note that this was sent to the house on the August 12, and the bill became law on the 16th, even though CBO said the final analysis wouldn’t be done for “a few weeks.”

Of the nine provisions addressed by the director in his letter to the House chairman, only one is said to reduce the deficit. And it would only be by $1 billion over the next 10 years. The other eight all are projected to increase the deficit. If you add up all the increases in the deficit listed above, you come up with $1.052 TRILLION in deficit increases.

What that says to me is that, if the best-case estimates of the Inflation Reduction Act, prior to the amendments, of $330 billion of deficit reduction were to be reality, the net effect of the legislation would be an increase in the deficit of $722 billion over the next 10 years. Perhaps I’m reading all this wrong. I’m willing to admit that I might be. But if I’m not, we’ve been swindled by free spending politicians yet again.

And Then There’s the Student Loan Forgiveness Proposal

But even if I am wrong, the student loan forgiveness proposal looms large on the horizon. It faces some constitutional challenges, and most likely will not become law. However, if it does, the Penn Wharton School of Business has scored the proposal and found the following:

- We estimate that President Biden’s proposed student loan debt cancellation alone will cost between $469 billion to $519 billion over the 10-year budget window, depending on whether existing and new students are included. About 75% of the benefit falls to households making $88,000 or less per year.

- Loan forbearance for 2022 will cost an additional $16 billion.

- Under strict “static” assumptions about student borrowing behavior and using take-up rates within existing income-based repayment programs, the proposed new IDR program will cost an additional $70 billion, increasing total package costs to $605 billion.

- However, depending on future details of the actual IDR program and concomitant behavioral changes, the IDR program could add another $450 billion or more, thereby raising total plan costs to over $1 trillion. These details require future study.

Essentially, all deficit reduction that could potentially occur with the Inflation Reduction Act would be wiped out in short order.

Some Final Thoughts on the Inflation Reduction Act from Some Reputable Sources

Speaking of inflation reduction, I’ve saved this until the end of the article intentionally. All the institutions who have scored the Inflation Reduction Act have come to the same conclusion. Here are some of their conclusions, in their own words.

Penn Wharton School of Business

“The Act would have no meaningful effect on inflation in the near term but would reduce inflation by around 0.1 percentage points by the middle of the first decade. These point estimates, however, are not statistically different from zero, indicating a low level of confidence that the legislation would have any measurable impact on inflation.”

Tax Foundation

“The history of the corporate alternative minimum tax indicates the book minimum tax may be a diminishing source of revenue. By increasing spending, the bill worsens inflation, especially in the first four years, as revenue raisers take time to ramp up and the deficit increases. We find that budget deficits would increase from 2023 to 2026, potentially worsening inflation. To the extent the tax credits and health-care subsidies are expected to be extended on a permanent basis, these policies put upward pressure on inflation”

“Lastly, to the extent the durability of the bill’s provisions are in doubt—that is, due to the lack of bipartisan support—it may have little impact on expectations about the fiscal outlook and therefore inflation. On balance, the long-run impact on inflation is particularly uncertain but likely close to zero.”

The Congressional Budget Office (CBO)

“In calendar year 2022, enacting the bill would have a negligible effect on inflation, in CBO’s assessment. In calendar year 2023, inflation would probably be between 0.1 percentage point lower and 0.1 percentage point higher under the bill than it would be under current law, CBO estimates. That range of likely outcomes reflects uncertainty about how various provisions of the bill would affect overall demand and output, the supply of labor, the persistence of disruptions in the supply of goods and services, and how the Federal Reserve would respond to offset any increase in inflationary pressure. Responsiveness to the enhancement of health insurance subsidies established by the Affordable Care Act is the most important factor boosting inflationary pressure, and responsiveness to the new alternative minimum tax on corporations is the most important factor reducing inflationary pressure. The range applies to multiple measures of inflation: the GDP price index, the personal consumption expenditures price index, and the consumer price index for all urban consumers.”

No Matter What Comes from the Inflation Reduction Act, You Need to Have a Plan

Perhaps they should have just renamed the bill. It would have been a lot more honest. The important thing, as always, is to have a plan to deal with the ever-changing tax and economic landscape that keeps you solidly on track to do all the things that are important to you, with the people that are important you, without having to worry what might happen to your plan “if” [insert unnecessary worry topic here].

Life is way too short for all that. Remember, if we’re lucky, we get 36,500 days on this marvelous blue ball. Sadly, most won’t get that many, which makes every day we do get precious. Don’t waste another one worrying because you don’t have a plan for the what ifs in life.

As I said earlier, only time will tell on whether the Inflation Reduction Act will reduce inflation. Whether you share my skepticism about it or not, it’s critical to have a comprehensive financial plan that gives you clarity, confidence, and control about your financial life.

We’re Here to Help You Better Understand the Inflation Reduction Act

If you want to break down the numbers that I shared in this article even further to see the impact that the Inflation Reduction Act could personally have on you, we’re giving you the opportunity to do exactly that with our industry-leading financial planning tool. It’s the same financial planning tool that our CFP® professionals use for our clients, and you can use it from the comfort of your own home. Just click the “Start Planning” button below to start building your plan today.

Keep in mind that our financial planning tool is intended for professional use. Should you have any questions while using it, our CFP® professionals are ready to answer them. By scheduling a 20-minute “ask anything” session or complimentary consultation with one of our CFP® professionals, they can screen share with using while using the tool and answer your questions. We help people make plans every day, and we’d love to help you too. All you need to do is ask.

Schedule a Complimentary Consultation

Click below to get started. We can meet in-person, by virtual meeting, or by phone. Then it’s just two simple steps to schedule a time for your Complimentary Consultation.

Investment advisory services offered through Modern Wealth Management, LLC, an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Adviser. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.