Considering RMDs Before and After Retirement

Key Points – Considering RMDs Before and After Retirement

- RMD Age Changes to 73 in 2023 … and to 75 in 2033

- The Implications of Choosing Between Roth or Traditional

- There Are Always Tradeoffs

- Assessing Current and Future Tax Rates

- 8 Minutes to Read | 18 Minutes to Listen

A Big Change with RMDs

Thanks to SECURE 2.0, the Required Minimum Distribution age changed to 73 in 2023. If someone turns 73 in 2023, they don’t need to start taking RMDs until April 1 of the year after they turn 73. However, if they wait until that point, they’ll need to take two RMDs in that year. There are some cases where that makes sense, but it also makes sense to start RMDs when you turn 73.

Knowing that that RMD age change is in place, Dean Barber and Will Doty, CFP® will look at Considering RMDs Before and After Retirement in our latest Modern Wealth Management Educational Series webinar.

Another Big Question to Consider: Roth or Traditional?

Before we dive into considering RMDs before and after retirement, there’s another question that needs to be asked. Should you go with a traditional IRA or 401(k), where you get a tax deduction before putting the money in? Or should you go with a Roth IRA or 401(k), where you pax tax before the money goes in and all the earnings are tax-free?

“We need to look at long-term projections of where you’re going to be in retirement from a tax perspective. In the past decade, all these Baby Boomers were told to take their tax deduction because they were going to be in a lower tax rate in the future. Well, we’re finding out that that won’t necessarily be the case. A lot of their tax rates will actually be climbing.” – Will Doty

Avoiding a Potential Tax Nightmare by Preparing for RMDs

An RMD forces the distribution of a required amount based on a uniform lifetime table from the IRS that forces money out of the IRA whether a person needs to spend it or not. Oftentimes, the RMD is bigger than the amount of money that an individual needs to spend in a given year. That can cause more Social Security to become taxable, trigger additional Medicare premiums, or cause people to hit the 3.8% Affordable Care Act tax. There are all kinds of things that large RMDs can do in the future.

So, it’s not necessarily only about what a person is going to spend. It’s a projection of how much money is going to be in someone’s 401(k) or IRA or whether it’s traditional or Roth when the RMDs start. You don’t want to run yourself into a potential tax nightmare.

“I always show my clients that when I’m looking at tax projections. I show them what their assets look like over time. When you get a client that’s in that situation, it’s always interesting to look at their mix of after-tax, tax-deferred, and Roth later on in life. Sometimes, people will start to see this weird little bubble where the after-tax bucket starts growing. That’s a problem because their RMDs is more than what they want to spend in retirement. They’re actually saving money and being forced to take the money out and pay taxes on it.” – Will Doty

Considering RMDs Before and After Retirement with Sam and Samantha Sample

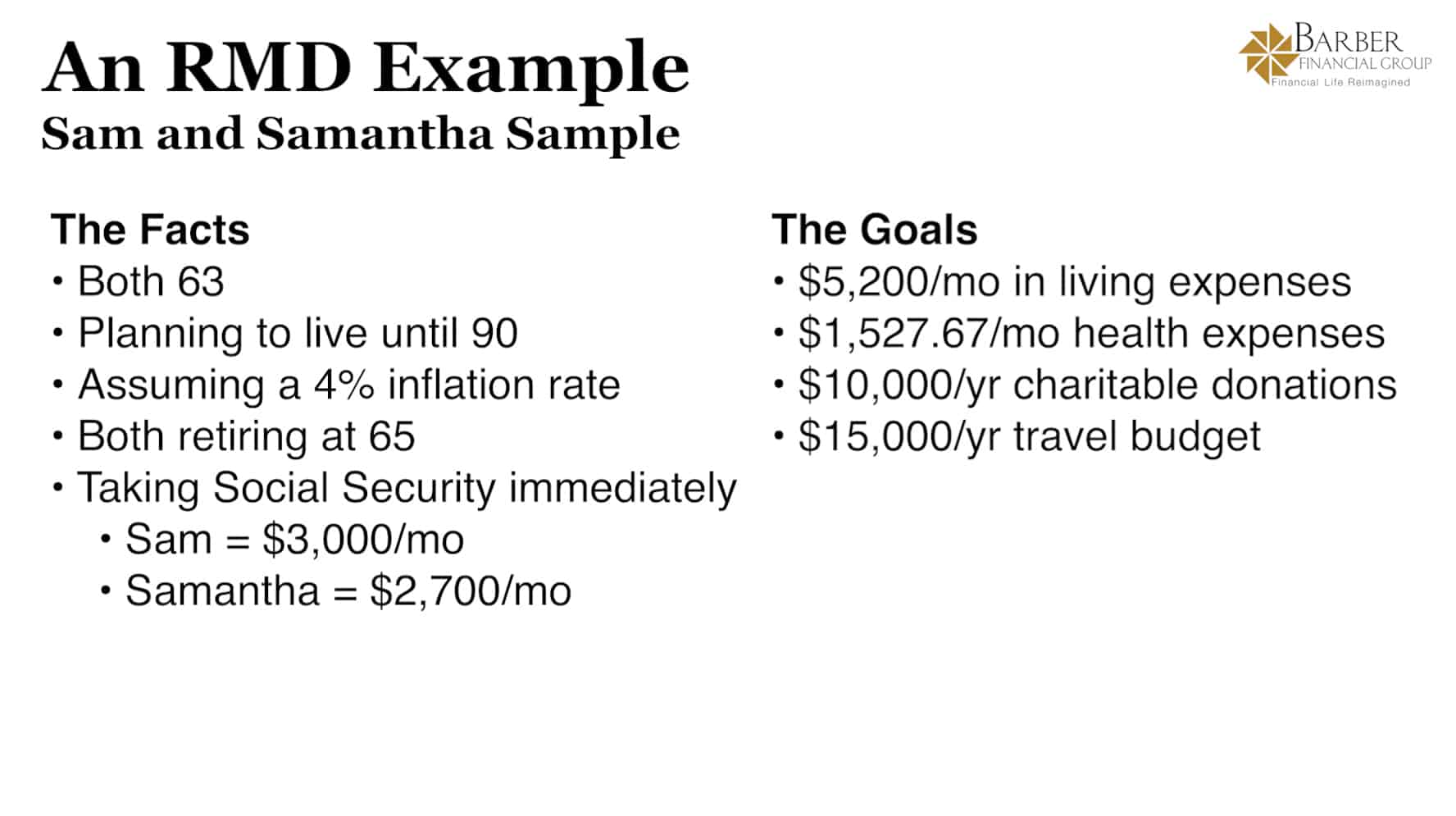

When we’re building and updating someone’s plan using our Guided Retirement System, we show people how much they have in each bucket—taxable, tax-deferred, and tax-free. We have some examples to review from a sample couple named Sam and Samantha Sample. In one example. In the examples, we’ll look at what happens when they save most of their money into a traditional 401(k) or IRA vs. a Roth 401(k) or IRA. As we’re running through those examples, keep in mind the tax implications over someone’s lifetime. Figure 1, below, has some pertinent background info about the Samples.

FIGURE 1 – Goals and Facts

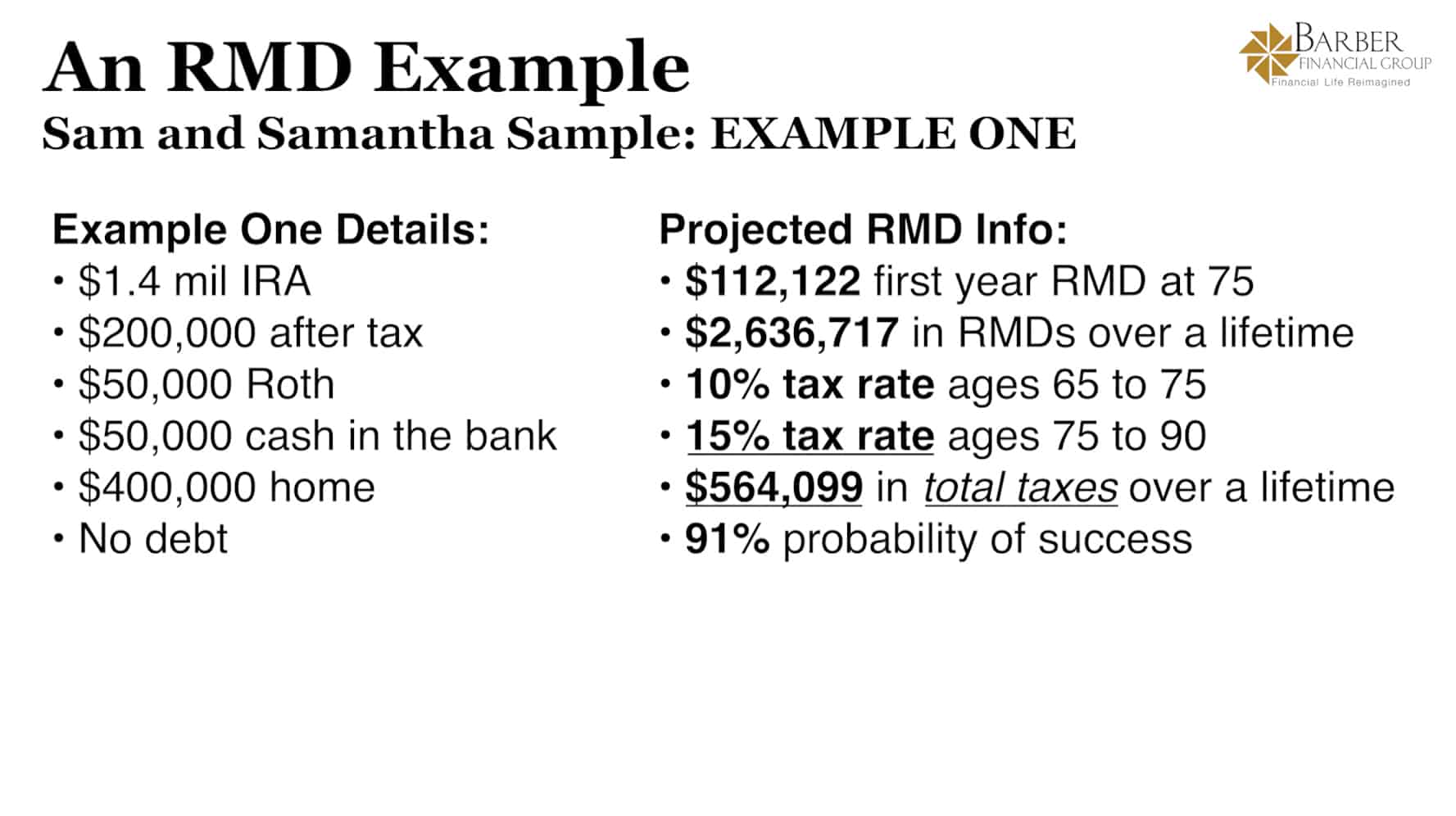

Example One

This first example is one that’s quite common. A majority of their assets are tax-deferred and then have a little bit in the after-tax and the Roth buckets. They have about $1.6 million in liquid assets and about $1.4 million of that was tax-deferred in an IRA. That would be coming from their 401(k) or whatever their employer plan would be. They also have $50,000 in cash in the bank and a $50,000 Roth IRA.

FIGURE 2 – Example 1

Another RMD Age Change from SECURE 2.0

When we do these long-term projections, there’s another new nuance about RMDs that needs to be considered. Due to the passing of SECURE 2.0, the RMD age will increase to 75 on January 1, 2033. The Samples will be turning 73 in 2033, so they still won’t need to take RMDs at that point. They’ll be taking their first RMD at 75. The projection of that RMD is $112,000.

“That’s substantial. Their total lifetime RMDs are $2.636 million. That causes their total tax to be $565,000 over their lifetime. That’s a lot. We always look at a plan when we start running these numbers. It shows a 91% probability of success in this scenario. That means that 91% of the time, they can spend what they want, keep up with 4% inflation, and not need to adjust their spending. So, 9% of the time, they may need to adjust their spending.” – Dean Barber

Anywhere between 75-90% range is considered to be an ideal probability of success, so 91% is still a good place to be. Still, they didn’t know early on in life that they had the power to change the bucket that they’re putting their life savings into, which will greatly impact their tax rate and RMDs will be in retirement.

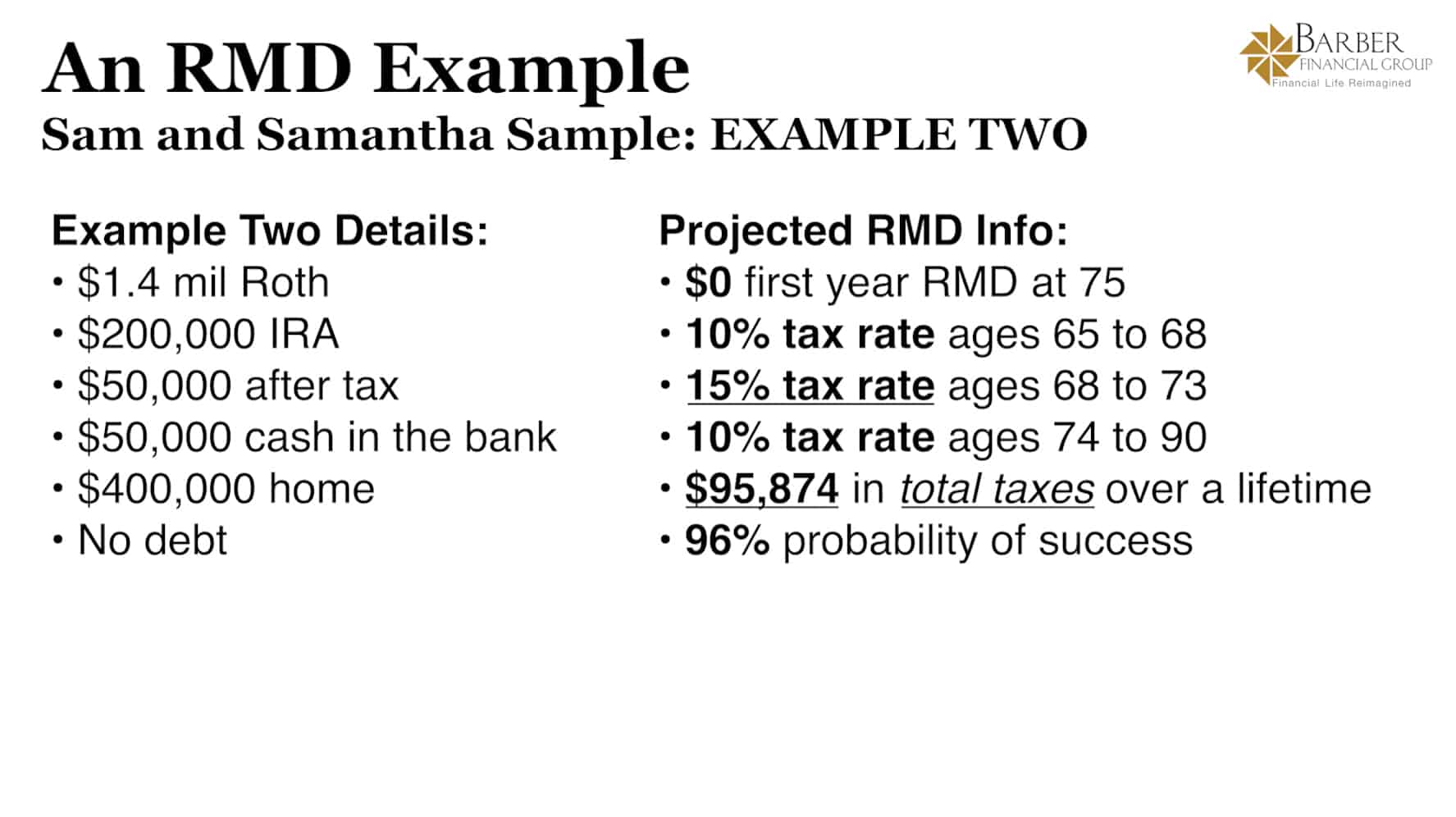

Example Two

So, now let’s look at how things would be for the Samples if they $1.4 million of their $1.6 million in Roth instead of traditional. There is no for Roth IRAs, so they’re not forced to take anything out of their Roth IRA and anything they do take out is tax-free. The savings in taxes during retirement is substantial in this scenario. They’re only paying $96,000 in taxes over their retirement as opposed to $565,000.

FIGURE 3 – Example Two

In this scenario, they have about $200,000 in tax-deferred and the rest is Roth. When we do these projections, they end up spending through the IRA before getting to RMD age. So, their projection for RMDs at 75 is $0.

“That’s pretty cool. They’re retiring earlier, spending the taxable portion first, and letting the tax-free portion continue to grow.” – Dean Barber

There is one thing that can be confusing in this scenario, and we want you to be clear on it. It is technically more difficult to achieve a $1.4 million Roth 401(k) or IRA than it is to achieve $1.4 million into traditional. That’s because in order to get money into the Roth, you had to pay tax on it before it went in as opposed to getting a tax deduction.

If someone is focused on saving to the Roth rather than traditional, it might mean that their standard of living during their working years could be slightly lower. That’s because their tax bill during their working years will be higher.

Analyzing the Tradeoffs of Roth vs. Traditional

It could seem like saving to the Roth is the no-brainer decision when you look at those numbers. But it’s not as simple as the examples from the Samples. It depends on your unique situation.

“You can’t just say a blanket statement that you should put everything into the Roth. It may be that you need to save more to get to where you want to be. An in order to save that amount, you need the tax deduction to live the way you want to live today. There are always tradeoffs. But the main point is that when you’ve accumulated most of your money into the Roth, your taxes in retirement are totally different. You have a lot more freedom.” – Dean Barber

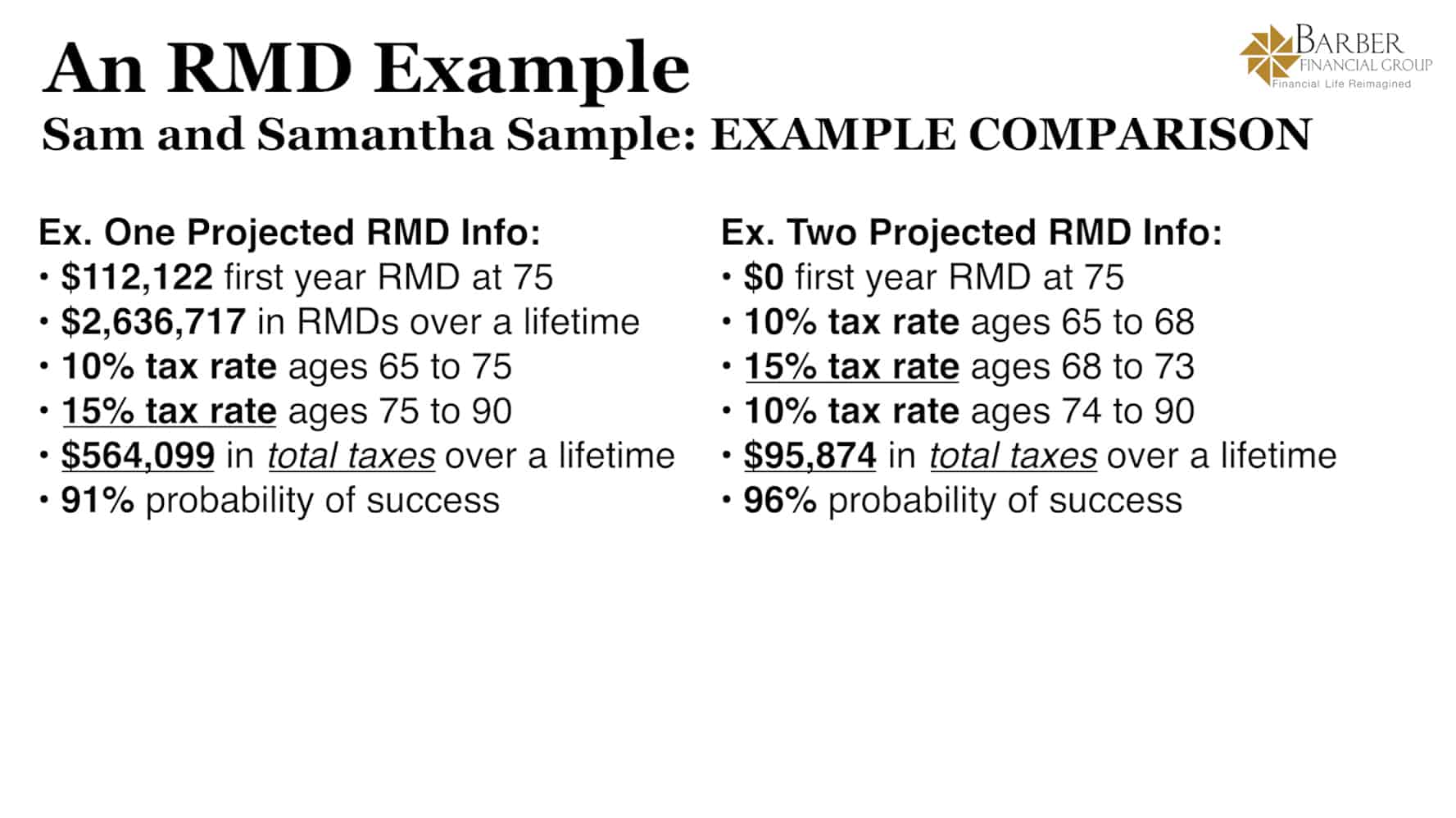

For Roth IRAs outside of the employer account, you have income limits. Some people might not be able to build outside of their employer plan. And, while most employers now offer a Roth 401(k), that is something that you want to confirm. And here’s another fun fact about SECURE 2.0 related to the Roth. The employer can now make a matching contribution to the Roth 401(k). The match always went to the tax-deferred portion of the traditional 401(k) prior to that. Here are the examples of the Samples side by side to get a better idea of what needs to be considered.

FIGURE 4 – Example Comparison

Planning Ahead for RMDs

As you’re saving for retirement, you really need to consider what those RMDs are going to be. That’s one of the important aspects of a forward-looking financial plan. Even if you’re 50 and want to retire at 65, we’re going to project what you have at 65 and where your income is going to come from in the first few years of retirement. Then, we’ll show what those RMDs are going to look like in the future so we can see that tax impact. That was what we were trying to get at with the Sam and Samantha Sample examples. The issue is that a lot of people aren’t aware of RMDs when they’re saving.

“It’s kind of like people don’t know how Social Security is taxed when they file their first tax return that includes Social Security. We need to look at that as well because those larger RMDs during retirement is just the tax that they’re paying. That could’ve triggered additional Medicare premiums if your taxable income goes above a certain amount.” – Dean Barber

Looking at the Bigger Picture of Family Financial Planning

If your RMD gets too large, you could get stuck forever in a higher IRMAA bracket. That’s also something we want to look at when we’re looking at the bigger picture later on in life. It’s not just about the taxes. We want to understand Medicare and all the other implications.

It’s the same thing when you pass away. How is this going to affect your kids and grandkids and the RMDs that they must take? Dean and Bud Kasper, CFP® discussed the SECURE Act and inherited IRAs late last year on America’s Wealth Management Show. The SECURE Act made the inheriting of IRAs and Roth IRAs so much more complicated. It’s very easy for someone to make a mistake and then be stuck with excess penalties if they don’t do the RMDs on inherited IRAs correctly.

You also need to keep in mind about how the surviving spouse is impacted. What happens when the first spouse passes away? Unfortunately, the tax rates change drastically for the surviving spouse because the brackets change. That’s something that everyone isn’t looking at if you’re working, married, and have kids.

“Will is younger than I am, but I’m looking at that today since I’m in my mid 50s. People don’t start thinking about it enough until they’re maybe in their 60s. I encourage people that as they cross that age of 50 to sit down with a CFP® Professional and doing things like projecting RMDs. Retirement is still going to be aways out for you. But getting a clear picture early on is critical, especially with figuring out RMDs in the future. It can give you clarity on how much and where you should be saving.” – Dean Barber

What Else Is There to Consider About RMDs Before and After Retirement?

We’ve hit most of the main points about considering RMDs before and after retirement. It’s about looking at your tax situation today and long-term. Are you staying level or are you going up in terms of tax rates? As Dean mentioned, meeting with one of our CFP® Professionals can help with planning for RMDs and much more when it comes to your financial planning needs. We give you the option of scheduling a 20-minute “ask anything” session or complimentary consultation with one of our CERTIFIED FINANCIAL PLANNER™ professionals. That meeting can be in person, by phone, or virtually.

After you meet with one of our CFP® Professionals, our team will dive in and figure out how to go about building your plan. But once that plan is built, it becomes a living, breathing plan that’s adjusted on a year-over-year basis. It acts as a guide to get you to where you want to be in the future.

The Clarity and Confidence That Comes from a Financial Plan

At the end of the day, your financial plan gives you the clarity and confidence that you want. You can’t understand what your financial picture looks like without a financial plan.

“As an example, there was a really nice couple that I just met with the other night. This woman was just turning 50 this year and has been saying all this time that her and her spouse had been doing what they can, but that they didn’t know what the future looks like since they didn’t have a plan. She desperately wanted a plan so she could understand it.” – Will Doty

In addition to that 20-minute “ask anything” session or complimentary consultation with one of our CFP® Professionals, we’re also giving you the chance to access our financial planning tool at no cost or obligation. It’s the same industry-leading tool that our CFP® Professionals and you can access it from the comfort of your own home by clicking the “Start Planning” button below.

Considering RMDs Before and After Retirement | Watch Guide

Introduction: 00:00

Big Changes in RMDs for 2023: 01:16

Roth or Traditional?: 01:50

The Impact of Large RMDs: 02:48

An RMD Example with Sam and Samantha Sample: 04:57

Analyzing the Tradeoffs of Roth vs. Traditional: 10:00

Planning Ahead for RMDs: 12:15

RMDs & Family Financial Planning: 14:19

Conclusion: 16:30

Investment advisory services offered through Modern Wealth Management, LLC, an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Adviser. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.