5 Ways to Avoid College Debt

Key Points – 5 Ways to Avoid College Debt

- Avoid Going to Private Schools or Out-of-State Public Schools (at Least from a Debt Perspective)

- Avoid Student Loans Altogether

- Avoid Not Working

- Avoid Waiting to Save

- Avoid Paying Taxes

- 7 minute read

5 Ways to Avoid College Debt

Over the weekend, I’m sure I wasn’t alone by spending most of my free time relaxing and watching Netflix. While scrolling through all the options, I came across a relatively new series called “Money Explained,” and episode three titled “Student Loans” caught my attention. This episode had some great facts about college debt, but unfortunately most of them were depressing and alarming.

The Game of Life

I thought the way the episode started with a reference to the board game, The Game of Life, was brilliant. This board game, now part of a permanent collection at the Smithsonian, was designed to simulate a person going through life, from college to retirement, with jobs, marriage, and possible children along the way.

The game starts with the decision of beginning adult life by going straight into the workforce or attending college. With the decision to attend college, student loan debt soon followed due to borrowing $40,000. Our culture has taught us that our first step as adults is to go directly into student loan debt. We believe this to be a prudent, simple strategy. The student studies hard to obtain a higher education that will provide a well-paying job, and then they repay the loan.

While this sounds perfect and may be a blessing for some people, it could be a tragic mistake with lasting effects for others. Students’ financial decisions impact the immediate direction of their lives. We need students and parents to be aware of ways to avoid college debt.

Sad Facts of Student Loan Debt

- We have reached a record-breaking $1.73 trillion in U.S. student loan debt in 2021. That is up from $1.57 trillion in 2020. This number has tripled over the past 15 years and projects to be more than $3 trillion over the next 15 years.

- 45 million Americans have student loan debt.

- Student loan debt is higher than debt from credit card and vehicle loans.

- 11.8% of student loans were 90 days or more delinquent or are in default. That’s more than one out of every ten borrowers that can’t make their next payment.

- Not so fun fact: The default rate is the highest for those with the least amount of student loan debt. Those with small student loans have a tendency of dropping out of school and struggling to find a job that pays a decent wage. Those with significant debt tend to have advanced degrees and likely are on schedule with their student loan payments.

Is Your Education Paying Off?

The average salary of a college graduate is reported to be around $76,000. That sounds great, but this is an average over someone’s lifetime. You wouldn’t make $76,000 until Year 14 of a 40-plus year career. Year 1 out of college may be a very different reality. According to ZipRecruiter, U.S. college graduates have starting annual salaries as high as $66,000 and as low as $22,000. The majority earn salaries between $36,000 (25th percentile) to $47,000 (75th percentile) with top earners (90th percentile) making $55,000.

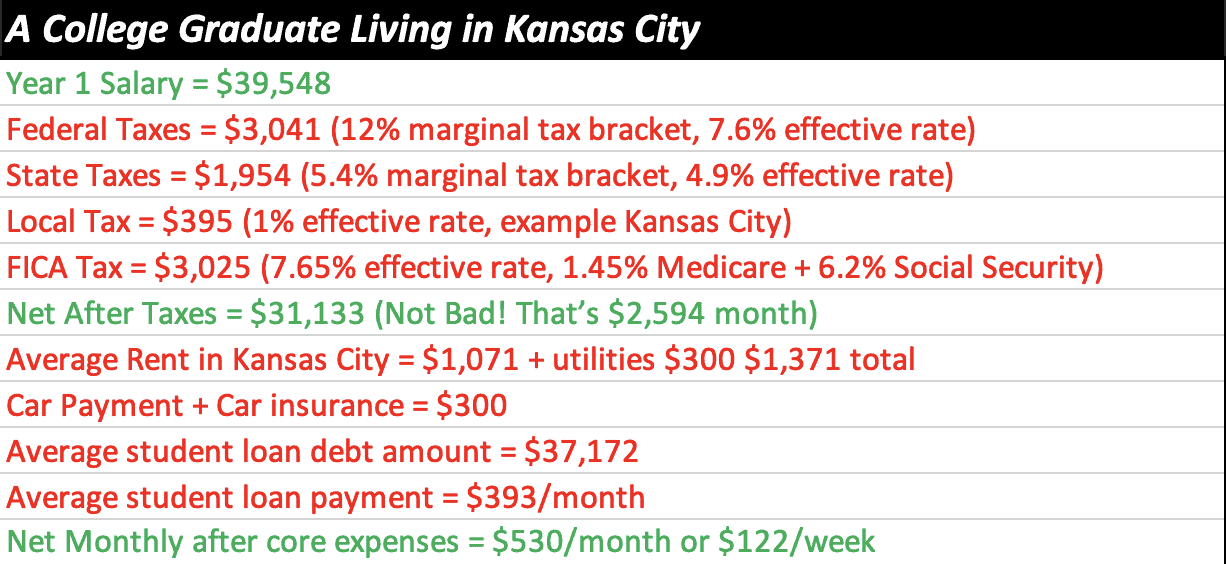

Keep in mind that these are nationwide averages. You need to know the reality of income expectations where you plan to live and the cost of living. ZipRecruiter also shares that a first-year college graduate in the Kansas City area makes an average of $39,548 per year. That’s $3,819 (9%) less than the national average annual salary of $43,367. Missouri ranks 32nd out of all 50 states for highest college graduate salaries.

TABLE 1 | Sources: RENTCafé and Nitro College

The Real Troubles of Being in the Red

Now, let’s run the same analysis, but for someone only making $22,000 per year. They would net $18,145 a year or $1,512 a month after taxes. After paying $393 per month in student loans, they are at $1,119 per month. If they find a place to rent, pay utilities, can afford a car to make it to work, they will be in the red -$552 per month.

A person who makes $36,000 (25th percentile) annually would be positive $311 per month. They would have $72 a week for food, gas, and entertainment, and praying they have no other financial surprises. Could you imagine what an extra $100 per week would mean for this individual if they had no student loans?

No College Equals No Debt? … Not So Fast

Suppose someone instead takes the opposing position in “The Game of Life” and goes directly into the workforce. Guess what? They completely avoid college debt. That was easy! Well, not so fast.

Unfortunately, average salaries for non-college students have decreased over the past 50 years. There is still a struggle to support cost of living even without student loan payments. This leads to many young adults living in their parents’ basement until their skills are developed and salary increases.

On average, student loans are paid in about a decade, so these young adults should be out of the house no later than age 30 to 32! Students and parents need guidance to avoid these costly mistakes.

What Parents Need to Do to Avoid College Debt

0. Avoid Having Kids

Just kidding!

What Students Need to Do to Avoid College Debt

1. Avoid Going to Private Schools or Out-of-State Public Schools (at Least from a Debt Perspective)

TABLE 2 | Source: Peterson’s Undergraduate and Graduate Institution Database

There are exceptional private schools and out-of-state universities with benefits to enrolling that may outweigh the price, but we are looking for ways to avoid college debt. Also, quick note, some public out-of-state universities will charge in-state tuition for students that qualify.

The average cost for private and public out-of-state schools are excessive compared to public in-state schools. We can see in Table 2 that the significant savings by avoiding the financial hurdle of private and public out-of-state schools. What else should you consider by lowering your public in-state expenses? Community college can save thousands in tuition. You can live at home, be enrolled in typically smaller class sizes, improve your GPA, complete general education courses, transfer credits, and graduate at a four-year in-state public school.

Average tuition/books expenses for community college students is $4,930 per year ($9,860 for two years). After completing two years of community college, you can transfer to a four-year In-state public school and pay a two-year average total cost of $53,640. Once you add the $9,860 from community college, you are at a four-year total of $63,500. That will save you $43,780.

TABLE 3 | Source: Peterson’s Undergraduate and Graduate Institution Database

Next, let’s look only at tuition and books for public in-state schools. What if parents are looking only to cover those core costs for college and/or the student lives at home?

The average expense is $11,737 per year. That equates to $46,948 for four years. That can be cut to just $23,474 for two years for those who go to community college first, so they have a four-year total of $33,334. The $46,000 or $33,000 hurdle spread over four years is starting to show some light now, totaling $8,300 to $11,500 per year.

2. Avoid Student Loans Altogether

That may seem impossible, especially with the case above showing that you are still looking at $60,000 to $110,000 to pay for room/board/books/tuition for a public in-state school. One of the best ways to reduce this amount is through scholarships.

Scholarships are great since you do not have repay this dollar amount. Athletic scholarships serve a larger number of student athletes. A great way to be proactive is to look for technology solutions and services like recruitlook.com to connect players to coaches. The earlier you start, the better.

You do not have to be a star athlete like Patrick Mahomes, or even an athlete. Just pull out your phone and you will discover hundreds of scholarship opportunities. Those include academic, community service, extracurricular, need-based, employer, and military scholarships. Fastweb is one of many great resources for this.

That leads me to grants. That’s financial aid that you don’t have to repay! Grants are supported through your universities, organizations, and businesses designed to assist students with their financial needs for education.

3. Avoid Not Working

Look for work study programs that allow you to work on or off campus in jobs that will financially support your college expenses. Working in general is a great way to save money up to and through college. Create a savings strategy to support your education expenses. When you are in college, keep working, especially over the summer, when you potentially have more free time. Understand your cashflow needs by identifying any excess to support college costs.

You can also reduce cost of living by locating rental properties off campus at a lower rate than on-campus. Then, take that lower expense and divide it by four by living with three of your friends.

Another great way to save is purchasing used books or going to Amazon for discounted prices.

4. Avoid Waiting to Save

TABLE 4 | Source: Peterson’s Undergraduate and Graduate Institution Database

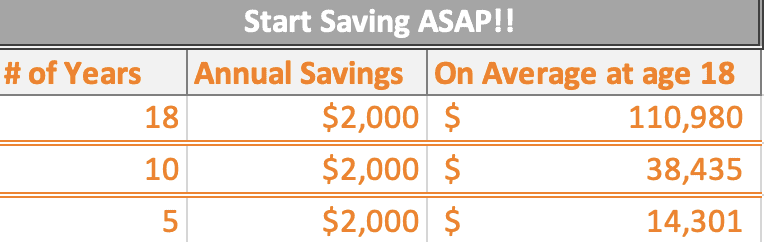

The longer you wait, the more pain and pressure you will feel saving for your children’s education, plain and simple. Parents that are looking to financially commit need to begin ASAP.

The analysis in Table 4 identifies parents that started saving at different ages. It’s amazing to see that beginning to save $2,000 a year at age 1, increasing that amount by 5% per year, and investing in a 60/40 stocks/bonds portfolio would eventually have $110,980 on average at the time the child enters college.

Look at what happens when you wait eight years. You only have $38,000 raised for your children’s college fund. Five more years doesn’t allow for enough time to accumulate any significant value. However, delayed savings is much better than no savings. While we have high hopes to support our children down the road, we are also trying to support and afford a family year by year. That’s not easy to do!

5. Avoid Paying Taxes

Although saving for college is great, removing Uncle Sam as you pay for college is even better. Two of the best ways to save for college is through a 529 Plan or an ESA (educational savings account, also known as a Coverdell account).

When you look at the parent that saved for 18 years, they would have contributed a total of $51,680 of after-tax money. If they are ready to fund college with the account that’s valued at $110,980 and they were not invested in an education account, then they would pay a capital gains tax and most likely some ordinary income tax as they withdrawal the appreciation away from this account. ESAs and 529s allow for tax-free appreciation and distribution for qualified educational expenses.

The Reality of The Game of Life

Graduates do not want to be in their parents’ basement anymore than their parents want them to. Plus, that makes for an awkward dating scene. It’s almost impossible to start a family as you attempt to move through the reality of “The Game of Life.”

Do not fall trap to the ease of access to student loans, nor give up on your education. Two of the most painful stories that were shared in this episode of “Money Explained” were how one graduate who entered the workforce with a little more than $80,000 in student loans, paid interest on this loan for 10-plus years, paying north of $100,000, and still owed more than $70,000 in student loans. That will make anyone more than just angry. The second sad story was a lady who defaulted on her student loans. She has filed for Social Security and receives a reduced amount as the government is still recovering money that she owes for these loans.

It’s far from easy, but I hope this helps illustrate the importance of building an education plan and avoiding college debt to the best of your ability. If you’d like to meet with one of our CPAs or CFP® Professionals about how to avoid college debt, please contact us.

Matt Kasper, CFP®, AIF®

Financial Advisor

Schedule Complimentary Consultation

Select the office you would like to meet with. We can meet in-person, by virtual meeting, or by phone. Then it’s just two simple steps to schedule a time for your Complimentary Consultation.

Lenexa Office Lee’s Summit Office North Kansas City Office

Investment advisory services offered through Modern Wealth Management, Inc., an SEC Registered Investment Adviser.

The views expressed represent the opinion of Modern Wealth Management an SEC Registered Investment Advisor. Information provided is for illustrative purposes only and does not constitute investment, tax, or legal advice. Modern Wealth Management does not accept any liability for the use of the information discussed. Consult with a qualified financial, legal, or tax professional prior to taking any action.